- within Finance and Banking topic(s)

- in United States

- within Finance and Banking topic(s)

- within Immigration topic(s)

Private credit is now becoming a well-established asset class in the Middle East. As activity grows, sponsors and investors are focusing as much on regulatory cost and efficiency as on structuring mechanics. The choice of jurisdiction directly affects speed to market, ongoing overheads and investor confidence.

As regional markets mature and diversify, alternative lending strategies are gaining traction among sponsors, institutional investors and family offices alike. This growth is driven not only by the search for yield and flexible capital solutions but also by the evolving regulatory landscape that shapes how these transactions are structured and executed. Understanding the regulatory nuances is essential for market participants seeking to deploy capital efficiently while maintaining compliance and investor confidence.

This is the third article in our series on private credit in the Middle East. The first examined orphan issuer vehicles in private credit transactions, while the second looked at the rise of private credit platforms in the Middle East: structuring scalable lending through Cayman Islands SPCs.

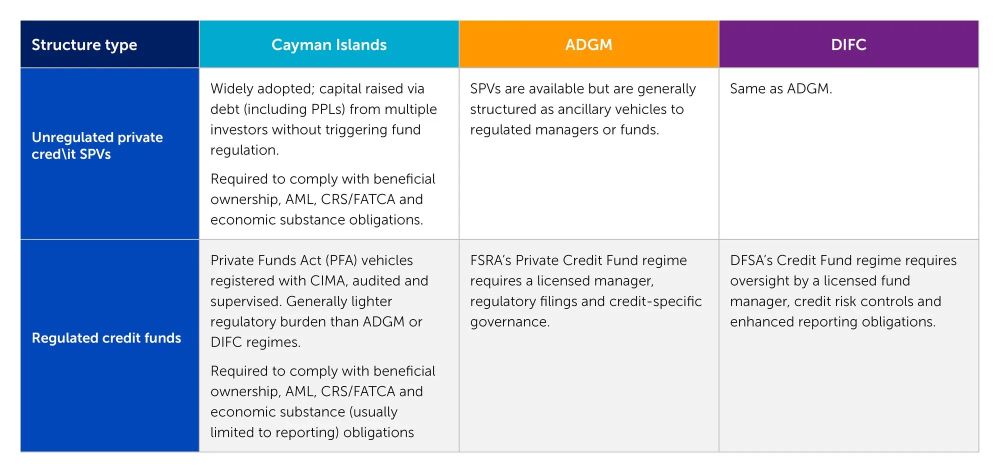

Here, we consider the regulatory framework - how Cayman Islands special purpose vehicles (SPVs) are treated, what regulation looks like, when is it required and how the Cayman Islands generally compares with the Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC) regimes.

Cayman SPVs: efficient, credible and investor-friendly

Cayman Islands SPVs have become a preferred structuring tool in Middle East private credit transactions, striking a balance between regulatory efficiency and institutional credibility.

- Private Funds Act (PFA). The PFA applies only

where equity interests are pooled. Most private credit SPVs raise

capital through debt instruments (such as notes or loans) and

therefore fall outside its scope. Where equity is pooled, the

vehicle would most likely need to register with the Cayman Islands

Monetary Authority (CIMA) and comply with certain regulatory

requirements under the PFA.

- Profit-participation loans (PPLs). Sponsors

increasingly use PPLs and similar instruments to aggregate capital

from multiple investors. These remain outside fund regulation

provided they retain clear debt characteristics and avoid

equity-like features.

- Securities Investment Business Act (SIBA).

Cayman Islands SPVs engaged in loan origination or note issuance do

not require a licence or registration under SIBA unless they are

conducting securities investment business in or from the Cayman

Islands (eg, discretionary portfolio management, advising etc),

which is not usually the case for typical private credit

transactions.

- Beneficial ownership reporting. Cayman Islands

SPVs must maintain a private beneficial ownership register via a

corporate services provider.

- AML and CRS/FATCA compliance. Anti-money

laundering (AML) / know-your-client (KYC) and CRS/FATCA obligations

are likely to apply.

- Economic substance (ES). All private credit Cayman Islands SPVs must file an annual ES notification. An ES return must also be submitted where an SPV conducts such activities or any other relevant activity under the ES regime. Private credit SPVs earning income from "financing or leasing activities" may be subject to enhanced substance requirements, but can be structured in a way to avail of an exemption from ES requirements.

In practice: Cayman Islands SPVs offer a streamlined and cost-effective way to raise capital (typically through debt) while remaining outside the scope of private fund registration and requirements. At the same time, they operate within a transparent framework that satisfies regulatory and investor expectations.

When regulation is required – Cayman Islands

Some sponsors prefer a regulated wrapper, either to meet investor expectations or for marketing purposes. The Cayman Islands provides this through:

- Private Funds Act funds. If the vehicle issues

equity interests and meets the private fund statutory definition,

it must (among other things) register with CIMA, appoint an

auditor, file audited accounts, meet governance and internal

control requirements and maintain valuation and conflict-management

policies.

- SIB Act licensing. Where securities investment business (eg, managing, arranging or advising in respect of securities) is carried on in or from the Cayman Islands, licensing or registration is required unless an exemption applies.

This flexibility means the Cayman Islands can offer both

unregulated SPVs and regulated funds depending on the sponsor's

objectives.

ADGM and DIFC credit fund regimes

Both the ADGM and DIFC have introduced dedicated regulatory frameworks for credit funds, going beyond the lighter-touch approach of Cayman Islands SPVs.

- ADGM. The Financial Services Regulatory

Authority (FSRA) launched its private credit fund regime in 2023.

It allows loan origination within a fund structure, provided the

fund is managed by an FSRA-licensed manager and adheres to

governance and reporting requirements.

- DIFC. The Dubai Financial Services Authority (DFSA) introduced its credit fund regime in 2022. It mandates that at least 90 percent of a fund's assets be deployed in credit, with oversight by a DFSA-authorised manager and additional credit-specific risk management controls.

While these regimes offer a regulated and supervised label, they come with more licensing, capital requirements, and reporting obligations compared to Cayman Island SPVs.

Key risks and structuring considerations

- Instrument design. Ensure profit-participation

loans (PPLs) and notes retain clear debt characteristics and avoid

equity-like features that could trigger fund regulation.

- SIBA scope. Confirm that any management,

arranging or advisory activity is not conducted in or from the

Cayman Islands unless appropriately licensed or registered under

SIBA.

- Economic substance. Assess early whether the

entity is in scope and plan for board-level oversight and

decision-making and filing requirements.

- Beneficial ownership. Maintain accurate and

up-to-date registers with your corporate services provider.

- Cross-border enforceability. Be aware that

collateral laws vary by jurisdiction and may affect enforcement

strategies.

- Investor preferences. Where a regulated structure is preferred, Cayman Islands private funds offer a credible and compliant solution.

Conclusion

Cayman Islands SPVs continue to be the most efficient and widely accepted structuring option for private credit transactions in the Middle East. They enable sponsors to raise capital from multiple investors using debt instruments (without falling within the scope of fund regulation) while still meeting global standards for transparency, anti-money laundering and economic substance.

For sponsors seeking a regulated structure, the Cayman Islands Private Funds Act offers a globally recognised framework with a lighter regulatory footprint than the credit fund regimes in ADGM and DIFC.

The choice is not binary: the Cayman Islands provides both a scalable, unregulated platform and a credible, regulated fund domicile - allowing sponsors to tailor their approach to investor preferences and transaction objectives.

Integrated legal and corporate support for private credit platforms

Walkers has deep experience advising private credit sponsors on the use of Cayman Islands SPVs and, where required, segregated portfolio companies as part of scalable platform structures. Our legal team regularly advises on the Cayman Island law aspects of:

- Regulatory structuring, and compliance, including CIMA

registration, SIBA and PFA compliance, beneficial ownership, AML,

CRS/FATCA and economic substance compliance.

- Security packages and intercreditor arrangements.

- Investor disclosure and offering documentation.

In addition to legal advice, Walkers offers a fully integrated corporate services platform that supports efficient execution through dedicated formation, fiduciary and administrative teams. Our services include:

- Fiduciary support, including share trustee services and

provision of independent directors.

- Company secretarial services and board governance support.

This end-to-end offering enables Walkers to act as a single point of contact for private credit clients -delivering seamless support from formation through execution, with on-the-ground expertise in the Middle East.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.