- with Inhouse Counsel

- in North America

- in North America

- in North America

- with readers working within the Banking & Credit, Business & Consumer Services and Insurance industries

In what is always of interest for dealmakers, the American Bar Association (ABA) has released its 2024 U.S. Public Target M&A Deal Points Study (the US Study).

The US Study comes less than a year after the release of the ABA's 2023 Canadian Public Target Deal Points Study (the Canadian Study) in the Spring of last year. In addition, the temporal periods of the two studies partially overlap, with the US Study analyzing transactions closed between January 1, 2021 and June 30, 2023, and the Canadian Study analyzing transactions announced in 2020 and 2021 (and closed before March 31, 2022).

Given the relatively close release dates and the partial temporal overlap, the two studies can also be used to (1) draw notable comparisons between contemporary U.S. and Canadian public M&A, and (2) identify significant trends from previous iterations.

For Fasken's Guide to Public M&A in Canada and our related M&A insights, visit our M&A Knowledge Centre.

Key Comparisons and Caveats

It has been noted that the M&A market trends illustrated by the ABA's U.S. deal point studies often forecast where Canadian M&A practice is likely to go in the future. Of course, this is not always accurate, which highlights the need to approach comparisons on a case by case basis, recognizing (among other things) the potential for divergences in applicable law.

An important difference between the U.S. and Canadian studies is the significant difference in minimum deal size. The US Study used US$200 million for the minimum deal size and the Canadian Study used CA$25 million. The study sample is also much larger for the US Study (312 deals) than for the Canadian Study (92 deals).

Another notable difference between the two studies is the industry sectors that are the focus of their deal samples. The US Study's top 4 distinct industry sectors (representing 59% of the sample deals) are technology (19%), banking and finance (17%), pharma and biotech (13%) and medical devices and healthcare (10%). Whereas the Canadian Study's top 4 industry sectors (representing 69% of the sample deals) are mining and natural resources (39%), cannabis (14%), industrial goods and services (10%) and oil and gas (9%).

Lastly, it must be appreciated that "what's market" remains general guidance. Many deal points are best resolved through an acknowledgment of the underlying reasonableness of the parties' respective positions in the particular circumstances. In other cases, asymmetry in negotiating leverage may be more likely to drive the ultimate outcome.

Closing Conditions

A review of closing conditions in the U.S. and Canadian studies shows a notable difference. In particular, the findings in the most recent iteration of each study show different approaches to when the target's representations must be accurate, i.e., at signing and closing, or only at closing. In the US Study, 28.8% of deals are limited to closing only, while in the Canadian Study this figure is higher at 41% of deals. That said, Canada appears to be trending towards the U.S., as this figure was much higher (64%) in the 2017 Canadian study.

Another notable difference is in the accuracy of the target's capitalization representation at closing. In the US Study, 88.9% of deals required the representation to be accurate "in all respects other than de minimus inaccuracies". In Canada the prevalence of this is markedly lower, at approximately 62%.1 However, there is a clear trend in Canada, going back to the 2013 Canadian study, of increasing use of the di minimus standard. It therefore appears that Canada is on the path to convergence with U.S. practice.2

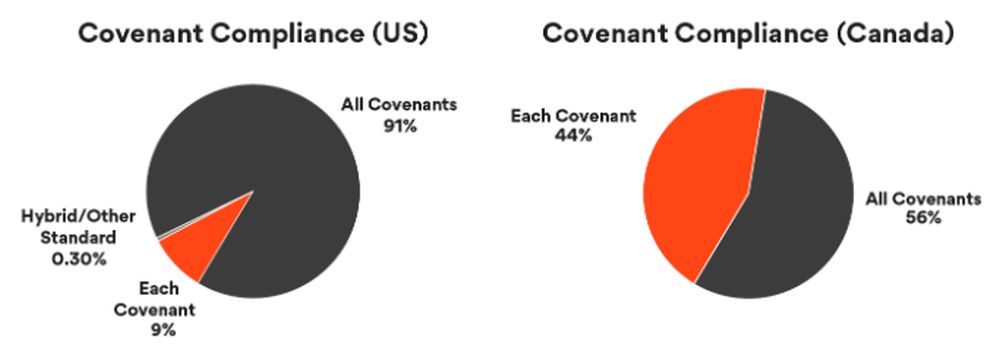

Regarding covenant compliance by the target, the U.S. Study sample leans heavily toward the more "seller-friendly" formulation of compliance with "all" covenants (91%) as compared to the more "buyer-friendly" formulation of compliance with "each" covenant (8.7%). By contrast, the ratio is much closer in Canada, "all" covenants appearing in 56% of deals and "each" covenant in 44% of deals. Moreover, Canada appears to be trending away from the U.S., with the "each covenant" formulation steadily growing in popularity since the 2013 Canadian study, where its frequency was only 11%. Amongst other things, this could indicate that Canadian practitioners increasingly view there not to be a meaningful difference between the two formulations from a contract interpretation standpoint.

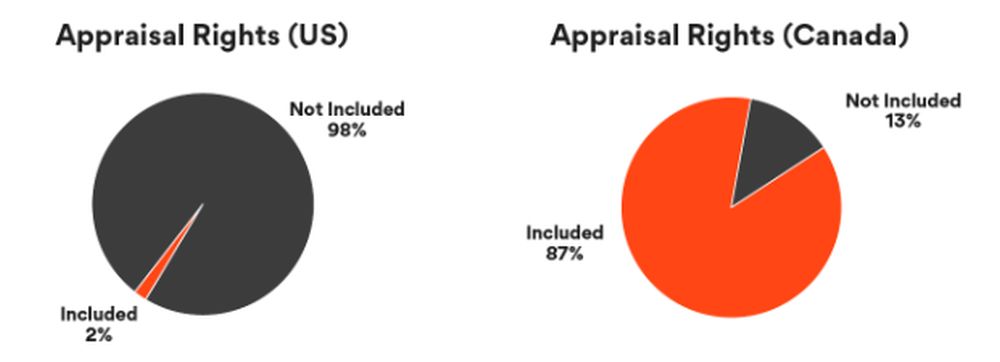

As we've previously written in The M&A Lawyer,3 another point of difference between U.S. and Canadian practice is regarding appraisal rights. For various reasons, appraisal rights are not an important aspect of U.S. public M&A, appearing in only 1.9% of deals. In stark contrast, appraisal rights are a dominant feature of Canadian public M&A, appearing in 87% of all cash deals, 100% of all stock deals, and 100% of part cash/part stock deals.4

U.S. and Canadian public M&A practice regarding closing conditions also differ notably regarding the absence of litigation. In the US Study, such conditions were included in only 10% of deals. This figure was much higher in the Canadian Study at 74%. This stark divergence is presumably explained by the greater regularity of stockholder litigation in U.S. public M&A as compared to Canadian public M&A.

Deal Protection

As has been the case historically, "go-shop" clauses remain more common in U.S. public M&A than in Canada, appearing in 8.5% of deals compared to only 3% of deals north of the border.

A fiduciary exception to a target's recommendation covenant for "intervening events" is well established in U.S. public M&A, appearing in 87.5% of deals. An "intervening event" refers to changes in circumstances, facts or events occurring after execution that were either not known to the target board or were not reasonably foreseeable but do not relate to any "acquisition proposal". Such clauses remain rare in Canada appearing in only 2% of deals in each of the Canadian Study and the 2017 Canadian study. However, the clause has begun appearing in Canadian public deals from 2015 onwards, which is indicative of U.S. M&A trends having influence in the Canadian market.

Material Adverse Effect (MAE) Clauses

Although U.S. and Canadian practice regarding MAE definitions are generally closely aligned, there are some significant differences. While reference to "prospects" has gone near extinct in U.S. deals (1.6%), 11% of Canadian deals still include the term, although trending downward.5 U.S. MAE definitions are far more likely to include an adverse effect on the target's ability to consummate the transaction (64.8% of deals), compared to only 17% in Canada. U.S. MAE definitions are also likely to feature a longer list of MAE "carve-outs," with over 12 carveouts occurring in 90% or more of deals while only 8 carveouts achieve 90% or greater frequency in Canada. For a detailed discussion of the similarities and dissimilarities in U.S. and Canadian MAE caselaw, including how this can impact drafting, see Fasken's Private M&A in Canada: Transactions & Litigation.

Knowledge Qualifiers

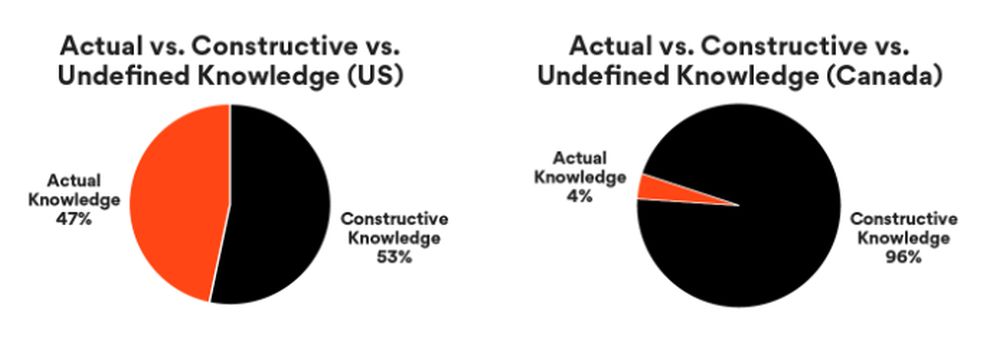

A sharp divide exists between U.S. and Canadian practice regarding knowledge qualifiers. In the U.S. there is a near even split between "actual" knowledge (46.7% of deals) and "constructive" knowledge (53.3% of deals). In Canada, "constructive" knowledge dominates, being employed in 96% of deals. Within the realm of constructive knowledge qualifiers, U.S. and Canadian practice much more closely align: in both jurisdictions "constructive" knowledge is very likely "inquiry" based (96.6% in the U.S. and 100% in Canada) rather than "role" based (3.4% in the U.S. and 0% in Canada).6

Interim Period Covenants

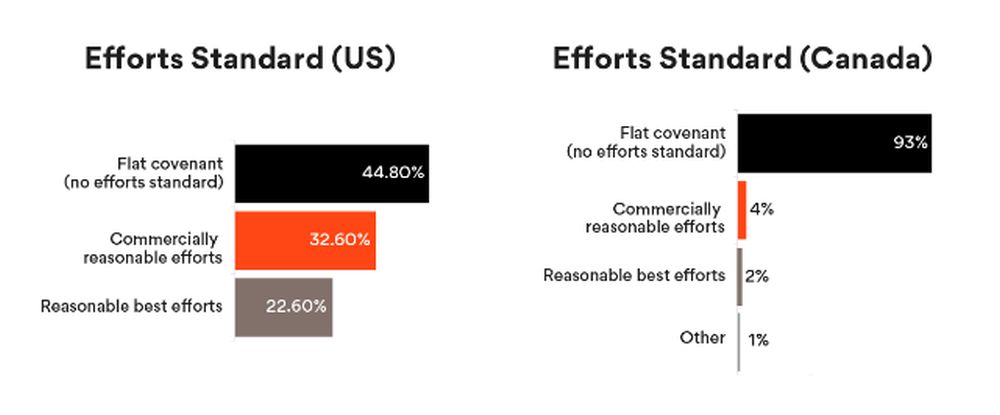

Regarding the target's covenant to operate the business in the ordinary course during the interim period, U.S. practice is varied: 44.8% of deals employ a flat covenant, 32.6% of deals employ a "commercially reasonable efforts" standard, and 22.6% of deals employ a "reasonable best efforts" standard. Canadian practice is more uniform, with 92% of deals featuring a flat covenant, and only 4% of deals using a "commercially reasonable efforts" standard and 2% using a "reasonable best efforts" standard.7

There are, however, two important nuances on the Canadian side. First, the ordinary course covenant is often followed by a separate covenant to preserve the target's assets, business relationships, etc., which is often qualified by a "commercially reasonable" or "reasonable" efforts standard. Second, the closing condition tied to the ordinary course covenant is typically subject to a materiality or MAE qualifier.

Two other differences in interim period covenants between U.S. and Canadian practice are in respect of "consistent with past practice" qualifiers and carve-outs for pandemic responses. "Consistent with past practice" qualifiers appear in 69.9% of U.S. deals but are almost omnipresent in Canada (96% of deals). By contrast, 79.3% of U.S. deals featured a carve-out for pandemic responses compared to only 53% of Canadian deals. That said, the discrepancy on this latter point (i.e., pandemic carve-outs) may be explained by the fact the US Study sample extends later in time than the Canadian Study sample.

For a comparison of how U.S. and Canadian courts have interpreted and applied "efforts" standards and "consistent with past practice" qualifiers in pre-closing M&A disputes, see Fasken's Private M&A in Canada: Transactions & Litigation.

Target/Seller Remedies

An interesting divergence between U.S. and Canadian practice relates to drafting for target (and target shareholders') remedies in a busted deal. In the U.S., 25.2% of deals included an express target right to pursue lost premium damages on behalf of stockholders, while in Canada only 2% of deals included such a clause. Writing in The M&A Lawyer in early 2023, we argued Canadian practice could learn from U.S. practice on the point.8 This area of public M&A practice is set to evolve following the ruling of the Delaware Court of Chancery in late 2023 in Crispo v Musk9, which cast doubt on the enforceability of different varieties of stockholder premium clauses (often referred to as "ConEd" clauses).

The Delaware Bar Association in March 2024 responded by proposing amendments to the Delaware General Corporation Law expressly permitting merger parties to contract for lost premium damages. Canadian courts have not directly addressed the enforceability of "ConEd" clauses. However, as we discussed in The M&A Lawyer, in Cineplex v. Cineworld the court on two occasions indicated the parties could have "entitled Cineplex, as the contracting party, to recover the loss of the consideration to shareholders if the Transaction was not completed."10

Footnotes

1. See Canadian Study Slide 32. 21% of deals apply a MAE standard to the capitalization representation similar to the target's other representations. Of the 79% of deals that apply a different standard, only 78% of deal apply an "in all respects other than de minimus inaccuracies." This means that, where as the figure is 88.9% in the US Study, in the Canadian Study it is effectively 62%.

2. Canadian dealmakers may therefore be interested in a recent Delaware ruling on capitalization representations and "phantom equity" in the private M&A context. See HControl Holdings LLC v. Antin Infrastructure Partners S.A.S., C.A. No. 2023-0283-KSJ (Del. Ch. May 29, 2023).

3. For more detailed discussion of this point, see Fasken's 2023 article in The M&A Lawyer, entitled "Appraisal Rights in Cross-Border Public M&A: Canada is Not Quite Delaware."

4. A noteworthy decision on appraisal rights under the Canada Business Corporations Act in the takeover bid context was recently released by the Quebec Court of Appeal. For Fasken's insights on the decision, see "One True Rule" Reigns Again in Public M&A: Court of Appeal Awards Dissenting Shareholders Significant Premium.

5. Down from 27% in the 2017 Canadian study and 30% in the 2013 Canadian study.

6. For a discussion of how knowledge qualifiers have been interpreted and applied in M&A disputes, see Fasken's Private M&A in Canada: Transactions & Litigation.

7. As previously mentioned, the US Study analyses transactions closed between January 1, 2021 and June 30, 2023 while the Canadian Study analyses transactions announced in 2020 and 2021 (and closed before March 31, 2022).

8. Cineplex's C$1.24 Billion Damages Award: Should Market Practice in Canadian Public M&A Learn From the U.S.? The M&A Lawyer (April 2023).

9. Crispo v Musk et al., C. A. 2022-0666-KSJM (Del. Ch. October 31, 2023).

10. Cineplex v. Cineworld, 2021 ONSC 8016 (CanLII). The court also stated: "If the parties had wanted to appoint Cineplex as the shareholders' agent to enforce their rights on Cineworld's failure to close, they could have done so."

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.