- with Finance and Tax Executives and Inhouse Counsel

- with readers working within the Media & Information, Property and Law Firm industries

Tax debts are essentially debts owed by a business to the Australian Taxation Office ("the ATO").

These can include tax & superannuation liabilities and debts, ATO interest & penalty charges, credits and refunds of indirect taxes, foreign tax credits, and/or franking credits and debits.

It may be that there is a mistake, or something is not quite right with the demand from the ATO.

If this is the case, then the onus is usually on the taxpayer to prove the inconsistency.

Disputes with the ATO over tax debts can take a considerable amount of time and be very expensive.

If you have tax debts, then it is vital that you get good legal advice from a suitably qualified disputes lawyer, especially considering the ATO is set to ramp up its debt collection activities.

What are Disputes about Tax Debts?

There are several different things that the ATO will do to force the payment of tax debts.

These things include:

- Send a letter of demand

- Issue Directors Penalty Notices

- Issue Garnishee Notices

- Commence Legal Proceedings

- Creditor's Statutory Demands

- Commence Wind Up Proceedings

- Commence Bankruptcy Proceedings

We will explain what these are, and what you can do if you receive one.

Letter of Demand from the ATO

There are several different types of letters that a business can get from the ATO in relation to tax debts. They can include:

- A demand letter from a debt collection agency that is engaged by the ATO.

- You may get a Superannuation Guarantee which is a bill to pay super.

- A demand letter asking you to lodge your taxable income payments annual report.

- A demand letter for failure to Lodge BAS on time.

- A demand letter asking you to pay your outstanding tax debt.

- A demand letter asking you to pay your overdue tax debt.

- A demand letter with a final reminder to lodge your tax return; and/or

- A final demand letter stating that the ATO will commence debt collection action.

These letters of demand are opportunities for you to start negotiation with the ATO before anything more serious happens.

If you do owe tax debts, then this may be a perfect opportunity to enter an ATO payment plan with the taxation department.

If you enter an ATO payment plan at this stage, then you will minimize any costs, fees, and penalties being added to the tax debts.

Our tax dispute lawyers have written more about ATO Payment Plans in this article below.

If you fail to resolve the dispute by way of negotiation, and an ATO payment plan, then the ATO may take action to recover this tax debt.

Directors Penalty Notices from the ATO

There are penalties for directors of non-complying companies pursuant to Division 269 of Schedule 1 of the Taxation Administration Act 1953 (Cth) ("the TAA").

The ATO may issue a director penalty notice if the taxpayer fails to meet their taxation obligation in relation to Pay As You Go ("PAYG"), Superannuation Guarantee Charge ("SGC"), and Goods & Services Tax ("GST").

Division 269-25 of the TAA states:

(1) The Commissioner must not commence proceedings to recover from you a penalty payable under this Subdivision until the end of 21 days after the Commissioner gives you a written notice under this section.

(2) The notice must:

(a) set out what the Commissioner thinks is the unpaid amount of the company's liability under its obligation; and

(b) state that you are liable to pay to the Commissioner, by way of penalty, an amount equal to that unpaid amount because of an obligation you have or had under this Division; and

(c) explain the main circumstances in which the penalty will be remitted.

(3) To avoid doubt, a single notice may relate to 2 or more penalties, but must comply with subsection (2) in relation to each of them.

(4) Despite section 29 of the Acts Interpretation Act 1901, a notice under subsection (1) is taken to be given at the time the Commissioner leaves or posts it.

There are two types of director penalty notices – a traditional notice and a lockdown notice.

Traditional Director Penalty Notice

A traditional director penalty notice is given when a company's tax liabilities are not paid but have been reported to the ATO within three (3) months of the due date.

A traditional director penalty notice is a notice giving the director of the company 21 days to do any of the following (pursuant to 269-15 of the TAA):

- the company complies with its obligation; or

- an administrator of the company is appointed under section 436A, 436B or 436C of the Corporations Act 2001; or

- a small business restructuring practitioner for the company is appointed under section 453B of that Act; or

- the company begins to be wound up (within the meaning of that Act).

This basically means, (1) pay (or enter into an agreement to pay); (2) put the company into administration or liquidation; or (3) engage a small business restructuring practitioner.

If any of these three (3) things are not done within the required time, then the director becomes personally liable for the amount of tax the ATO says is outstanding.

It is very important to contact a tax dispute lawyer or insolvency practitioner as soon as possible after receiving a director penalty notice.

There are a few defences to a director penalty notice, see below.

Lockdown Director Penalty Notice

A lockdown director penalty notice is given when a company's tax liabilities are not paid and have not been reported to the ATO within three (3) months of the due date.

The only way to avoid personal liability for a lockdown director penalty notice is to pay the company debt within the 21-day period.

The reason for this is to ensure that directors cannot avoid liability for aged taxation debts by placing the company into liquidation.

It is very important to contact a tax dispute lawyer or insolvency practitioner as soon as possible after receiving a director penalty notice.

There are a few defences to a director penalty notice, see below.

Defences to a Director Penalty Notice

There are a couple of defences to personal liability of directors served with a director penalty notice pursuant to 269-35 of the TAA, they are:

- Illness; and

- All reasonable steps

We will explain these in a little more detail below.

Illness as a Defence to a DPN

Division 269-35(1) of the TAA says:

1) You are not liable to a penalty under this Division if, because of illness or for some other good reason, it would have been unreasonable to expect you to take part, and you did not take part, in the management of the company at any time when:

(a) you were a director of the company; and

(b) the directors were under the relevant obligations under subsection 269-15(1).

Further to this, in Canty v Deputy Commissioner of Taxation [2005] NSWCA 84 Handley JA said at [48] (with Beazley JA and Santow JA agreeing):

This defence can only succeed if the illness or other good reason continued for the whole of the time the director was in office and the obligation to comply with [s269-15] continued.

Further, in Deputy Commissioner of Taxation -v- Miller [No 2] [2021] WADC 65, Russell DCJ said:

The obligation of a director under s 269-15(2) is a continuing one that applies throughout the period commencing on the breach of the obligation to pay the PAYG withholding amounts on the due day and continuing until the expiry of the DPNs. As a consequence, any defence under s 269-35(2)(a) must cover the whole of that period.

There are similar cases which concur with the cases above. This means that to rely on illness as a defence, the illness must have made it:

- Unreasonable to expect a director to take part, and the director did not take part, in the management of the company.

- Throughout the entirety of the directorship.

- From the time of the breach of the obligation to pay the eligible debt, until the expiry of the director penalty notice.

There is also a defence if the director took all reasonable steps.

All Reasonable Steps as a Defence to a DPN

Division 269-35(2) and (3) of the TAA says:

(2) You are not liable to a penalty under this Division if:

(a) you took all reasonable steps to ensure that one of the following happened:

(i) the directors caused the company to comply with its obligation;

(ii) the directors caused an administrator of the company to be appointed under section 436A, 436B or 436C of the Corporations Act 2001 ;

(iia) the directors caused a small business restructuring practitioner for the company to be appointed under section 453B of that Act;

(iii) the directors caused the company to begin to be wound up (within the meaning of that Act); or

(b) there were no reasonable steps you could have taken to ensure that any of those things happened.

(3) In determining what are reasonable steps for the purposes of subsection (2), have regard to:

(a) when, and for how long, you were a director and took part in the management of the company; and

(b) all other relevant circumstances.

This essentially means that a director may avoid liability for tax debts if:

- The company complied with its obligations to pay; or

- The company appointed an administrator; or

- The company began to be wound up in liquidation; or

- There were none of the steps available.

In Roche -v- Deputy Commissioner of Taxation [2015] WASCA 196, the Court said at [35]:

The taking by the director of 'all reasonable steps to ensure', within s 269-35(2)(a), requires that each of the alternative events be addressed, either on the basis of taking reasonable steps to ensure the event happened or declining to do anything about that particular event on the basis that there were no reasonable steps that the director could have taken to ensure that the event happened.

Whether the director took reasonable steps is an objective test.

Again, in Roche -v- Deputy Commissioner of Taxation [2015] WASCA 196, the Court said at [29]:

What is 'reasonable' for the purposes of s 269-35(2) does not depend merely upon the actual knowledge of the director but involves an objective test. The director must prove that he or she took all steps which were reasonable, having regard to the circumstances of which the director, acting reasonably, knew or ought to have known: see Deputy Commissioner of Taxation v Saunig [2002] NSWCA 390; (2002) 55 NSWLR 722; (2002) 43 ACSR 387 [25].

It is very important to contact a tax dispute lawyer or insolvency practitioner as soon as possible after receiving a director penalty notice.

Read our complete guide to director penalty notices here

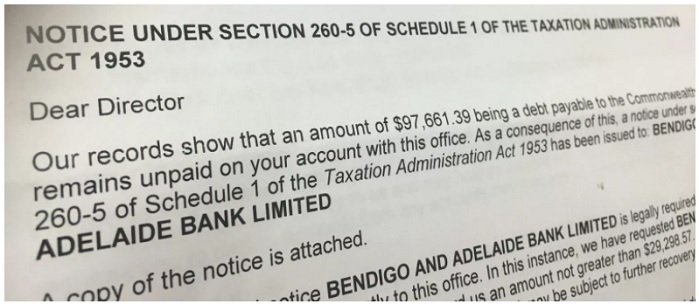

The ATO can also issue garnishee notices.

Garnishee Notices from the ATO

The ATO can issue a garnishee notice to a third-party business or person holding money for the taxpayer.

This garnishee notice requires the third-party to pay any money due to the taxpayer directly to the ATO.

ATO garnishee notices are often embarrassing, and sometimes damaging to your business as they drag third parties into your financial issues and may cause significant cashflow issues.

The ATO can send a garnishee notice to several different third parties.

For individual taxpayers, the ATO may issue a garnishee notice to:

- Your bank, building societies other financial institutions.

- People who may owe the taxpayer money from the sale of real property.

- The taxpayer's employer or head contractor.

For business taxpayers, the ATO may issue a garnishee notice to:

- Your business suppliers of merchant card facilities.

- Your business trade debtors.

- Your business bank or financial institution.

The authority for the ATO to issue garnishee notices is contained at section 260-5 of schedule 1 of the TAA. Section 260-5(1) says:

(1) This Subdivision applies if any of the following amounts (the debt) is payable to the Commonwealth by an entity (the debtor) (whether or not the debt has become due and payable):

(a) an amount of a * tax-related liability;

(b) a judgment debt for a * tax-related liability;

(c) costs for such a judgment debt;

(d) an amount that a court has ordered the debtor to pay to the Commissioner following the debtor's conviction for an offence against a * taxation law.

So, the ATO can issue a garnishee notice for a tax debt, and judgment given on a tax debt, and the costs of obtaining judgment on a tax debt.

Section 260-5(2) of the TAA says:

The Commissioner may give a written notice to an entity (the third party) under this section if the third party owes or may later owe money to the debtor.

This section authorises the ATO to send the written garnishee notice to the third party.

A copy will also be sent to the taxpayer.

Section 260-5(3) of the TAA states that the third party is taken to owe money to the debtor if the third party:

- is an entity by whom the money is due or accruing to the debtor; or

- holds the money for or on account of the debtor; or

- holds the money on account of some other entity for payment to the debtor; or

- has authority from some other entity to pay the money to the debtor.

The third party is so taken to owe the money to the debtor even if:

- the money is not due, or is not so held, or payable under the authority, unless a condition is fulfilled; and

- the condition has not been fulfilled.

The ATO garnishee notice will require the third party to pay the alleged amount of the tax debt immediately after issuance; or within a specified time after the amount of the available money concerned becomes an amount owing to the debtor.

What does the ATO Consider?

The ATO Practice Statement Law Administration 2011/18 says at 106:

The ATO will consider the following when deciding whether to issue a garnishee notice:

- the tax debtor's financial position and circumstances and the steps the tax debtor has taken to pay the debt in the shortest possible time frame;

- any other debts that the tax debtor owes;

- whether the revenue is placed at risk because of the tax debtor's actions (ie paying other creditors in preference to the ATO); and

- the likely implications on the tax debtor's ability to provide for a family or maintain the viability of a business should the notice be issued.

Are there any defences to an ATO garnishee notice?

Defences to an ATO Garnishee Notice

There are a few things that a taxpayer can do to attempt to stop the third party from making the payment requested by the ATO. These include:

- Checking that the formal requirements of the garnishee are included.

- If the garnishee notice has been issued in bad faith or for an improper purpose.

- If issued on judgment, if there is a stay of enforcement or appeal available to the taxpayer.

- If the funds are held in foreign currency, held in a joint account, or held in a self-managed superannuation fund account.

However, these are not very strong defences and are likely to be risky applications to make.

Typically, if the ATO can see that the taxpayer is prepared to settle this tax debt dispute, and agree to enter into a payment plan, and/or offer some security for the tax debt, then the ATO may withdraw the garnishee notice.

However, the ATO may also commence legal debt recovery proceedings.

Legal Proceedings to Recover Tax Debts

If a taxpayer disputes a tax assessment by objecting pursuant to Part IVC of the TAA, then the ATO can commence legal action to recover this disputed debt.

It can be difficult to successfully defend tax debt proceedings because the general rule that an assessment is conclusive evidence:

- That the taxation assessment was properly made; and

- Of the amounts of the amount of tax payable, penalties and interest owing.

This means that even if there is a genuine dispute about part of the tax liability, the taxpayer may still have to pay the entire assessed amount to the ATO until the tax debt dispute is resolved.

Even if you lodge your notice of objection, you are still required to pay the entire tax assessment amount.

Even if you get a notice that the objection was not successful, and you file an appeal in the Administrative Appeals Tribunal or the Federal Court, then you are still required to pay the entire tax assessment amount.

Because of this, it can be very difficult to defend tax debt legal proceedings.

Tax Debt Legal Defences

Tax debts are especially difficult to defend because of the 'conclusive evidence rule'.

The conclusive evidence rule basically says that if the ATO says you owe $1m in tax, then you owe $1m in tax, and it is up to you to prove you do not.

What this means is if the ATO commences tax debt recovery proceedings, then the Court is bound to accept that the amount of tax owing in the ATO's notice of assessment is correct, and the Court cannot challenge that.

In certain cases, the taxpayer may try to use 'conscious maladministration' as a defence.

The defence of conscious maladministration means that the assessment by the ATO is invalid because it is so wrong. However, this is not simply an argument that the ATO made a mistake, but in fact the ATO must have acted in bad faith.

This is a difficult argument to make.

The Legal Tax Debt Recovery Process

For taxpayers who want to have a punt at defending an ATO claim, or genuinely believe there has been conscious maladministration and bad faith by the ATO then the process is:

- Service of the claim and statement of claim.

- Filing and serving a notice of intention to defend and defence.

- Disclosure / Discovery.

- Mediation / settlement conference.

We will explain these in more detail below.

Service of the Claim and Statement of Claim

If the defendant taxpayer is a person, then the claim and statement of claim must be served on the debtor personally.

This means that the ATO are required to engage a process server to identify the taxpayer and hand the documents to the taxpayer personally.

If the taxpayer is a company, then pursuant to section 109X(3) of the Corporations Act 2001 (Qld) and section 9 of the Service and Execution of Process Act 1992 (Cth), the ATO can serve the documents by (inter alia):

- Leaving it at, or by sending it by post to, the company's registered office.

- Delivering a copy of it personally to a director of the company who resides in Australia.

Once served, a taxpayer will have 28 days to file a notice of intention to defend and defence.

If the taxpayer does not, then the ATO may obtain default judgment.

Filing and Serving a Notice of Intention to Defend and Defence

You have 28 days from the date of service to file a notice of intention to defend and a defence to the claim by the ATO.

As above, it is very difficult to successfully defend a tax debt claim.

Ideally, you will provide your lawyers with all the evidence that you will seek to rely on in good time in order for the solicitors and barristers to formulate a legal strategy and draft the defence.

The ATO then have to file and serve a reply to your defence.

Once the pleadings have closed, the parties are required to disclose documents to the other.

Disclosure / Discovery

A party to a legal tax debt proceeding has a duty to disclose to each other party each document (a) in the possession or under the control of the first party; and (b) directly relevant to an allegation in issue in the pleadings; and (c) if there are no pleadings—directly relevant to a matter in issue in the proceeding.

Every document that the party wants to rely on at trial must be disclosed to the other party.

If the taxpayer does not feel that the ATO has provided all of the documents, then the taxpayer can make an application that the ATO provide those documents.

Once disclosure has been complied with, the parties are usually required to complete mediation or attend a settlement conference in an attempt to resolve the tax dispute.

Mediation / Settlement Conference

The mediator is usually a trained mediator or barrister.

The purpose of the mediation is to negotiate a settlement which will usually be put into a binding deed of settlement.

Find a mediator at the QLS – http://services.qls.com.au/Web/FindLegalServices/ApprovedMediator

If the matter cannot be settled at mediation, then the tax debt proceeding will proceed to a trial.

Risks of Losing at Trial

The main risks of losing at trial are:

- You will likely be ordered to pay the ATO's legal costs; and

- A judgment will go on the taxpayers' credit report.

It is usual for the 'loser' in litigation to pay the legal costs of the 'winner'.

These legal costs will usually be calculated on a standard basis, and in some cases on the indemnity basis. This would be somewhere between 65% and 85% of actual costs.

If the taxpayer loses at trial, then there will be a judgment entered against the taxpayer. This judgment will be lodged on the taxpayer's credit file, and if the decision is reported then it may be searchable on Google when a search of the taxpayer is made.

Once the ATO gets a judgment, it can then start enforcement proceedings. This will usually consist of issuing a statutory demand / winding up or issuing a bankruptcy notice / creditor's petition.

We will explain these in more detail below.

Statutory Demands to Recover Tax Debts

If the taxpayer is a company, then the ATO can issue a creditor's statutory demand.

The ATO does not need a judgment to issue a creditor's statutory demand, as a statutory demand can be served with an affidavit in support or a judgment in support.

The statutory demand formal requirements include:

- It must be in writing and use the correct form – Form 509H.

- It must correctly identify the debtor and the creditor or creditors.

- It requires the debtor company to pay, secure, or compound for the debt within 21 days.

- It must correctly and sufficiently identify and particularise the debt or debts owing by the debtor company; and

- It must be signed by the ATO creditor.

Pursuant to section 109X of the Corporations Act 2001 (Qld), the ATO can serve the documents by (inter alia):

- Leaving it at, or by sending it by post to, the company's registered office.

- Delivering a copy of it personally to a director of the company who resides in Australia.

Once served, the taxpayer has 21 days to either:

- Pay the amount claimed by the ATO.

- Secure or compound for the tax debt.

- Request that the statutory demand be withdrawn; or

- Make an application to the Court setting aside the demand.

If the taxpayer does not do any of the above then it is presumed to be insolvent, and the ATO can make an application to wind up the taxpayer company in insolvency.

If the taxpayer pays, or reasonably secures or compounds (enter into an arrangement to pay) for the debt, then the statutory demand is extinguished.

If the taxpayer has grounds to set the demand aside, then before making the application, they may simply request that the demand be withdrawn, based on the strength of their argument to set the demand aside, we can offer you advice

If the ATO refuse to withdraw the statutory demand, then the taxpayer may make an application to set aside the statutory demand.

The taxpayer has four (4) main grounds for setting aside the statutory demand, they are:

- There is a genuine dispute as to the existence or amount of the debt; and/or

- They have a genuine offsetting claim; and/or

- There is a defect in the demand which is likely to cause substantial injustice; and/or

- Some other reason.

Usually, the bar for setting aside a statutory demand is quite low. However, because of the conclusive evidence rule, it is a lot more difficult when it is ATO tax debts.

All that the taxpayer needs to do is prove to that any of the above exist, and the demand will likely be set aside.

If the demand is set aside, then the Court may order that the ATO pays the ATO's costs of the application.

We have a very detailed article on setting aside a statutory demand here.

If the taxpayer fails to do any of the above, the ATO may file a winding up application.

ATO Commenced Wind Up Proceedings

The ATO initiates winding up proceedings against a taxpayer company by application to the Federal Court (or Supreme Court) pursuant to section 459P of the Corporations Act 2001 (Cth).

The form of this application is Form 2 Corporations Rules 2.2(3).

An application for an order winding up a taxpayer company should include the following:

- The application; and

- The draft winding up order; and

- The affidavit in support of the application.

Once this application has been made, and if everything being correct, the ATO will be given an originating process sealed with the Court's seal ready for service by the ATO.

There are a number of strict time limits that must be adhered to in relation to the service of the originating process, so it is again vital that you engage a suitably qualified debt recovery and insolvency lawyer.

Possible Defences to Winding Up

A taxpayer company can apply to oppose a winding-up application of the following grounds:

- Solvency – the taxpayer company will need to prove solvency. The Courts have called this process "an onerous task and likely to be an expensive process for the company"; and/or

- The statutory demand, or service of the statutory demand, was deficient; and/or

- Where creditors have a better prospect of payment without winding up – with an administrator or controller; and/or

- The Court may consider the views of other creditors and whether those creditors oppose the application when deciding whether or not to exercise its discretion to make a winding up order.

However, in a lot of cases the Court has found that it is in the public interest to wind-up an insolvent company.

If the taxpayer debtor is a person, then the ATO may also commence bankruptcy proceedings.

ATO Commenced Bankruptcy Proceedings

Bankruptcy proceedings are commenced by the ATO satisfying the below requirements:

- The taxpayer debtor must be a natural person.

- The ATO must have a judgment or order from the Court of $10,000.00 or more.

- The ATO must apply for a notice at AFSA.

- The ATO must serve the bankruptcy notice on the taxpayer debtor.

- The ATO must a creditor's petition with the Federal Court; and

- The ATO must be given a sequestration order from the Court.

We will explain the bankruptcy notice and creditor's petition in more detail below.

Bankruptcy Notice

Before applying for a bankruptcy notice the ATO must perform a bankruptcy search. A search of the Bankruptcy Registry will determine if this taxpayer debtor is already bankrupt.

If the debtor is not already bankrupt, then the ATO can apply for the bankruptcy notice.

The Australian Financial Security Authority ("AFSA") works on behalf of the Official Receiver, being the agency that issues bankruptcy notices.

Once the ATO has the bankruptcy notice, it must serve it on the taxpayer debtor.

The taxpayer will then have twenty-one (21) days to comply with the notice, or attempt to set it aside.

One of the reasons that a bankruptcy notice can be set-aside is for "other reasons" – those other reasons may include:

- An irregularity or defect in the notice.

- The amount being claimed exceeds the amount allowed to be claimed.

- There is a mistake in the names of the creditor or the debtor; and/or

- The notice has been completed incorrectly.

If the taxpayer does not comply with the bankruptcy notice or make an application to set the bankruptcy notice aside, then the taxpayer has committed an act of bankruptcy.

After the act of bankruptcy, the ATO can file a creditor's petition.

Creditor's Petition

Once the taxpayer debtor commits an act of bankruptcy and all of the requirements above are satisfied, the ATO can apply to the Federal Circuit Court, by way of a creditor's petition, for a sequestration order.

The filing of a creditor's petition is just like any other application essentially. The ATO will need to file an application (petition), an affidavit in support of the application, affidavit of service of the notice, and consent to act as trustee (from a trustee in bankruptcy).

Then before the hearing, the ATO will need to provide the Federal Circuit Court with further affidavits.

If all of the steps have been completed correctly, then the Federal Circuit Court will issue a sequestration order, forcing the taxpayer debtor into bankruptcy.

It is vitally important that the taxpayer does not let it get to this point.

Negotiate a Payment Plan

In most cases, the quickest and most cost-effective way to resolve ATO tax debts is by negotiation.

It is possible to negotiate a settlement sum and a repayment plan with the ATO.

ATO payment plans are usually only made if the taxpayer is up to date with all their current taxation obligations.

An ATO Payment Plan is a great way for businesses to pay their tax debts in instalments.

These instalment payments help business owners to:

- Avoid unnecessary insolvency action.

- Keep their business trading.

- Manage the business cash flow; and

- Repay their tax debts in manageable amounts.

You can complete the ATO's payment plan estimator to calculate repayments.

Do you Qualify for an ATO Payment Plan?

For the taxpayer to qualify for an ATO payment plan, the ATO must consider the following criteria:

- The taxpayer must prove that the payment plan is in the interests of good management and administrative common sense.

- The taxpayer's debt must not be in dispute.

- The taxpayer's payment plan must not favour any creditor and ensure the payment plan is fair to all creditors.

- The taxpayer's payment plan must offer all the net assets of the taxpayer; and

- The taxpayer's proposal must be in writing and supported by material outlining how the taxpayer will fulfil the payment plan.

Are you Eligible for an ATO Payment Plan?

A taxpayer will be eligible for an ATO payment plan if:

- The taxpayer's business cannot obtain finance or a loan.

- The taxpayer's business has a history of good payments and lodgement, including (a) no more than one ATO payment plan default in the preceding 12 months; and (b) no outstanding lodgements of business activity statements.

- The taxpayer's business has a recent business activity statement debt of less than $50,000, overdue for no longer than the preceding 12 months.

- The taxpayer's business has an annual turnover of $2 million or less.

- The taxpayer's business is able to show it is viable moving forward; and

There are certain things that a taxpayer can do to assist. These include:

- Act Quickly – Your tax debt will continue to grow (with fees and interest) if you continue to ignore it.

- Develop Good Habits – If there has been an ongoing issues around failure to pay tax debts or non-lodgement, then the ATO may not agree to a payment plan.

- Making A Good Offer – If your proposed payment plan will return a better outcome than legal proceedings, then the ATO will be more inclined to accept.

- Take the First Step – the taxpayer should be proactive about the tax debt. Make the first move and address your obligations first.

Conclusion to Resolving Tax Debts

It is almost always better to try to resolve your tax debts by negotiation or alternative dispute resolution, than legal proceedings.

There are a number of different ways to settle a tax debt dispute, including (inter alia) arbitration, early neutral evaluation, independent review, in-house facilitation, mediation, and negotiation.

The onus is always on the taxpayer to prove that the tax debt claim is not genuine, which could be very difficult.

There are also some serious issues around time delays and costs.

Tax Debt Litigation Time Delays

If a tax debt dispute goes to Court, then it may take years to reach a resolution (up to ten (10) years in some cases).

Practically, this could cause a number of problems such as documents getting destroyed or go missing.

Further, the interest rate payable on the tax debt can be substantial and compounds daily.

Costs of Tax Debt Litigation

Just like all litigation, the costs of litigation can be incredibly expensive.

A taxpayer must make a commercial decision as to the value of being involved in taxation litigation with the ATO.

In most cases, these tax debt disputes should just settle.

Tax Debt FAQ

We get asked a number of questions in relation to tax debts.

What happens if you have a tax debt?

You will need to negotiate a settlement to resolve this text debt dispute, or the ATO may issue directors penalty notices, issue garnishee notices, commence legal proceedings, issue creditor's statutory demands, commence wind up proceedings, and/or commence bankruptcy proceedings.

What causes tax debt?

Non-payment of your taxation obligations, including income tax, pay as you go, superannuation guarantee charge, and goods & services tax.

How do I clear my tax debt?

The best way to clear your tax debt is to pay it in full, obtain a loan to pay the tax debt, negotiate a settlement, and/or arrange an ATO payment plan.

Can tax debt be waived?

In certain circumstances, the ATO can waive some or all of a taxpayer's tax debt. It only relates to certain tax debts, if the taxpayer is unable to afford accommodation, clothing, education, food, and/or medical treatment

Does tax debt affect your credit score Australia?

A tax debt itself will not affect a taxpayer's credit score in Australia. The ATO will need to obtain a judgment against the taxpayer or start insolvency proceedings for it to affect a taxpayer's credit score in Australia.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.