- within Compliance topic(s)

Numerous Federal and State taxes concessions are now available for BTR developments to support and encourage the sector. This note outlines the presently available state taxes concessions and issues applicable to a BTR project. As the statutory regimes vary across jurisdictions and detailed requirements apply, it is important to carefully consider these to ensure:

- from a planning perspective, that the project models the appropriate tax treatment and meets available concession conditions where possible;

- from an operational and/or due diligence perspective, that any concessions obtained are not inadvertently lost (or otherwise ensure that the triggers for and consequences of any potential unwind of a concession are understood).

It will also be important to obtain advice at the various stages of the project, as circumstances, applicable laws and Revenue practice evolve, noting that the BTR bespoke regimes are only in their early stages currently.

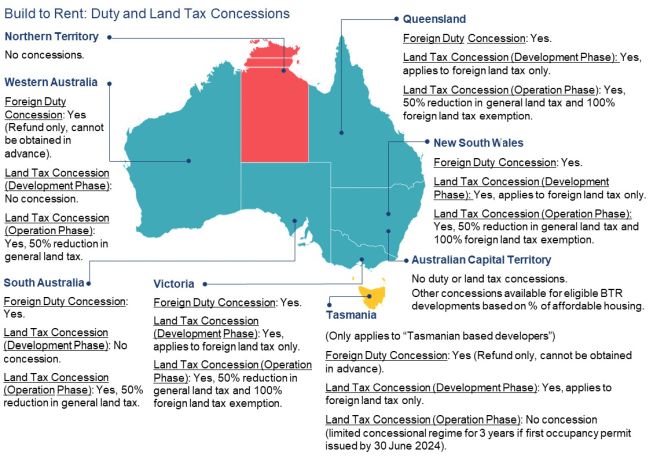

Duty and land tax concessions for BTR

A number of duty and land tax concessions are available for eligible BTR developments.

Overview of duty and land tax regimes and available concessions

Broadly speaking:

- In addition to the duty normally payable when a person acquires land, an additional duty surcharge rate (of up to 8%) applies to a foreign acquirer of residential land, unless an exemption applies. An exemption from surcharge duty may apply for residential developers generally or for land that is developed into an eligible BTR. (No foreign surcharge duty applies in ACT or NT.)

- Land tax is generally payable by an owner of land (except in NT), calculated on the taxable value of land. A concession applies to reduce the taxable value by half for eligible BTR developments (generally during the operational phase and for a specified period only, eg 20 – 30 years).

- In addition to ordinary land tax, a surcharge land tax of up to 4% applies to land owned by a foreign person (other than in WA, SA and NT). An exemption may apply during the development phase of a BTR project, and in some cases for a specified period during the operational phase.

- Where a BTR benefit has been relied upon, on-going conditions must be met to avoid a significant claw back of the benefits. For example, a subdivision within 15 years could result in a claw back in some States (such as might occur on strata conversion for sale). The position varies as to whether a minor or temporary breach, or a cured breach, will result in a claw back. Where continuous compliance is required, a breach may also mean that the project can never be eligible for the concessions again.

Eligible BTR

Some key features to qualify as an eligible BTR development include:

- a new development – being a new building or a conversion usually from a non-residential to residential use;

- a parcel held within a unified ownership structure (but can be co-owned);

- management of the BTR development must be provided by a single entity (eg management of the leases, common areas, facilities etc), including on-site management access for tenants. Affordable/social housing can be separately operated;

- a minimum number of self-contained dwellings (eg 50 or more);

- residential tenancy agreements offered to the public (ie not a subset such as student accommodation), meeting specified requirements including an offer of a fixed term lease of at least 3 years (but tenants may opt for a shorter term);

- affordable/social housing components;

- proportion of labour sourced from certain classes of workers.

The requirements are consistent with government policy to support housing affordability and new construction in Australia. As noted earlier, the requirements vary depending on the applicable jurisdiction.

Some issues to consider

Some issues to be aware of include:

- The position where land is used for BTR and another purpose, or where use is available to residents and non-residents (eg manager's residence, pool, gym, storage and car park may be treated as BTR, whereas shops, cafes and hairdressers and other commercial ventures may not);

- Where land is acquired and co-owned by a foreign person and an Australian person, complexities can arise and the rules must be carefully considered to ensure there are no unintended outcomes;

- Complications can arise for staged developments (eg where each stage does not meet the minimum dwellings requirement on its own);

- Ensuring transaction documents appropriately allocate

compliance and tax liability, for example:

- whether any land tax including the surcharge is passed on to tenants,

- who should be liable for ensuring particular BTR conditions continue to be satisfied (as between an owner vs a manager, or a seller vs a purchaser where a project is sold during say the initial 15 year period) – for example, ensuring rental agreements meet applicable requirements, ensuring conditions of affordable housing continue to be satisfied etc;

- note that although conditions are imposed to ensure ownership remains unified and to prevent subdivision, no restrictions apply to a sale of the BTR project as a whole (or of the landowner or management entities). Where a project is sold, the new owner can become statutorily liable to any clawed back of the BTR benefits obtained by the previous owner;

- Consideration should also be given to the availability of a private ruling to manage risk;

- Detailed timing requirements and anti-avoidance measures apply;

- A windfall gains tax applies in Victoria from 1 July 2023 (subject to transitional rules and excluding GAIC area), with tax rates of up to 62.5% where land is rezoned resulting in a value uplift. An exemption applies to land capable of being used for residential purposes at the time of rezoning.

Summary of applicable regimes

You can download our summary tables here which detail the available concessions and key requirements in each Australian State and Territory.1

Footnote

1. NSW

https://www.revenue.nsw.gov.au/taxes-duties-levies-royalties/transfer-duty/surcharge-purchaser-duty/exemptions-and-concessions/build-to-rent Land Tax Build to Rent Treasurer's Guidelines: Build to-rent Properties

Vic: https://www.sro.vic.gov.au/land-tax-discount-build-rent-developments http://www.gazette.vic.gov.au/gazette/Gazettes2018/GG2018S450.pdf#page=5

Qld: https://qro.qld.gov.au/resource/da000-15/ https://qro.qld.gov.au/resource/lta000-4/ https://www.legislation.qld.gov.au/view/html/inforce/current/act-2010-015#pt.6A

WA: https://www.wa.gov.au/government/multi-step-guides/duties-information-requirements/foreign-transfer-duty-duty-requirements/developer-exemptions-duty-requirements https://www.wa.gov.au/government/announcements/build-rent-land-tax-exemption#:~:text=The%20build%2Dto%2Drent%20exemption,20%20years%20for%20eligible%20developments

https://www.parliament.wa.gov.au/parliament/bills.nsf/BillProgressPopup?openForm&ParentUNID=9908145C8F28C7E3482589B10029707A (subject

to legislation)

SA: https://www.revenuesa.sa.gov.au/forms-and-publications/information-circulars-and-revenue-rulings/revenue-rulings/sda012v2 https://www.legislation.sa.gov.au/__legislation/lz/b/current/statutes%20amendment%20(budget%20measures)

%20bill%202023/b_as%20introduced%20in%20ha/statutes%20budget%20measures%20bill%202023.un.pdf (subject

to legislation)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.