On Friday, 6 September 2024, The Supreme Court of NSW ruled in favour of Uber in Uber Australia Pty Ltd v Chief Commissioner of State Revenue [2024] NSWSC 1124. Chief Justice Hammerschlag ruled that Uber's objection to six payroll tax assessments amounting to $81,515,923 from 2015 to 2020 should be upheld.

This case, assuming the Chief Commissioner does not appeal it, will have significant implications for taxpayers and Chief Commissioners in other States and Territories on how payroll tax ought to be regulated in regard to the gig economy. In respect to taxpayers who employ contractors or operate on models similar to Uber, it highlights how the manner in which contractors are paid may determine whether the employer will be liable for payroll tax in their respective state.

Background

The Plaintiff, Uber, applied to the Court to review the decision of the Defendant, the Chief Commissioner, disallowing Uber's objection of six payroll tax assessments.

Uber is a rideshare system which enables riders in contact with drivers of motor vehicles offering the service to pick them up and transport them to their destination. This service is achieved by way of Uber's software described as the Driver and Rider App.

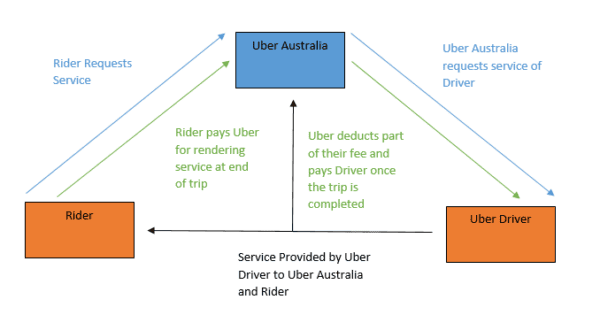

The following is broadly how Uber's service is structured:

The Chief Commissioner assessed Uber should have paid payroll tax on the basis that the amounts received by Uber from the Rider and remitted to the Uber drivers and are wages as amounts paid or payable for or in relation to the performance of work relating to a relevant contract. The Commissioner did so on the basis that Division 7 of the Payroll Tax Act treats certain payments to contractors as wages and caught under the payroll tax regime.

The issues in this case may be summarised as follows:

- Section 32 Payroll Tax Act 2007 – Whether there is a

relevant contract between Uber and its Drivers

- A sub-issue here is whether services were undertaken by the Drivers;

- If those services were for or in relation to the performance of the work;

- Whether the services were supplied to Uber under a contract;

- Whether any statutory exceptions applied; and

- Whether the amounts paid by Uber were for or in relation to the performance of the work rendered by the Drivers.

Judgement

Issue 1 – Section 32 – Was there a relevant contract?

The issue here required the identification of what services was supplied to Uber and the existence of a relationship between the services and the performance of work which results in those services being "for or in relation to" that work.

The Court acknowledged that the term, 'services' has a wide meaning as per IW v City of Perth (1997) 191 CLR at 11 defining it as an act of helpful activity. In characterising the services provided by the Drivers to Uber, the Court accepted the Chief Commissioner's contention and adopted a trichotomy analysis moving forward. The Chief Commissioner argued that the following were services supplied by the drivers to Uber:

- Transporting riders from their pickup point and transporting them to their destination;

- Giving feedback about riders at the end of the trip; and

- Referring people to Uber for the purpose of them becoming drivers.

Further, Uber was supplied with the above services in relation to the provision/performance of the work, that being the transportation of riders to their destination.

In regard to whether the services were suppled to Uber under the contracts, the Court, referring to Commissioner of Taxation v Sara Lee outlined that the contract under which something occurs is to be identified by determining whether it is properly seen as the source of the obligation to do that thing. The crux here being that if what is done is the exercise of a right, the determination is whether the contract is properly seen as the source of the right.

Although the drivers had the right to determine when to provide the services, the obligation imposed on them on when and where they could exercise their right to drive the customers was sourced in the contracts.

"The Contracts give drivers and partners the right, if and when they drive, to use the Driver App. They have the right to use the Driver App even if they choose not to drive. The right to use it, and all the entitlements and benefits stemming from its use, including the opportunity to drive, or to decline to drive, for gain, have their source in the Contracts".

Issue 2 – Are there any Statutory Exceptions

Ancillary Exclusion

It was found that the rating services provided by Uber whereby the drivers rated the riders at the end of the trip was ancillary to the use of the goods which were the property of the driver. On the other hand, the driving and by extension the referral services were one and the same with the provision of the vehicle. The Court outlined that it cannot be properly described that driving as a service is ancillary to the use of the vehicle. There is no room for separating the two, that being the provision of the vehicle and the act of driving the vehicle to the rider's destination.

The consequence of the finding that the driving and referral services were not ancillary meant that section 32(2B) applied to 'denude' Uber of the benefits of the ancillary exclusion for its rating service. This was interestingly a consequence of the Court and the parties to this case accepting a trichotomy analysis, where the services were assessed as a whole, as opposed to a holistic analysis where the three services provided to Uber by the drivers would have been assessed separately.

90 Day Exclusion

Whether this exception applies depends, in relation to each driver, whether the services provided by the drivers were supplied for less than 90 days during the financial year. The Chief Commissioner argued here that if a driver supplied services of any kind during the day, regardless of the brevity of said service, that day would be counted as a day for the calculation of whether the 90 day threshold has been met. Uber on the other hand argued that working for a specified period of the day means working for that many hours notionally equivalent to that which would have been worked by a full-time employee.

The Court rejected Uber's approach outlining that the selection of 7.6 hour days is "random and imports ambulatory operation".

To the Public Generally Exclusion

This exception applies if the services performed by the drivers are of the type ordinarily performed by the driver to the public generally.

Uber's contention was that there are drivers that held taxi licences and hire car licences during the relevant period. Uber argued that the services supplied by said drivers to Uber are of the same kind provided to the public by the taxi drivers and hire car drivers and the exception applied.

However the Court found that there was insufficient evidence to establish the frequency of the taxi or hire car driving by the drivers to enable the Court to conclude that the drivers ordinarily engaged in that activity.

Issue 3 – Are Amounts Paid or Payable to Uber taken to be Wages Paid or Payable under s35(1)

The crux of the issue here is whether the there was a connection between the payments made by Uber to the Drivers and the services/work done by the Drivers.

The Court found that it was not Uber who pays the driver to establish that connection. The rider does that. Uber was characterised as a mere payment collection agent. While Uber had to account to its drivers for what it received as an agent, by the time Uber has done that, the driver has already been paid and the rider has discharged their obligation to pay the driver for the ride. The Court highlighted the following clause in the Driver Contract which indicated this:

"You appoint Uber as your limited payment collection agent solely to accept the Fare, applicable Tolls, and , depending on the region and/or if requested by you, applicable taxes and fees from the User on your behalf via the Uber Services' payment processing functionality, and agree that the User's payment made directly by the User to you"

While there was certainly a relationship between the payment made by Uber to its drivers and the work which said driver performed, that relationship cannot be described such that the payments made by Uber as payment collection agent was in relation to the work done. The said work had already been done by the driver. In particular, the Court noted:

"There is no element of reciprocity or calibration between the driver and Uber or the rider and Uber with respect to the money paid by the rider. Those elements exist only between the driver and the rider. The payment here is made pursuant to an obligation to account, and no more

...

What the rider pays the driver is for or in relation to the work done by the driver. What Uber pays the driver is in relation to the payment Uber has received, not in relation to the work itself"

Indeed, what the rider pays the driver is for or in relation to the work done by the driver. What Uber paid is in relation to what Uber has received, not in relation to the work conducted by the driver itself.

As a result of this, the Court allowed the Uber's objection to the six payroll tax assessments by the Chief Commissioner.

Observation

This case is noteworthy given it would need to be considered alongside similar cases, such as payments made by medical practices to their doctors. This case is similar to Homefront Nursing Pty Ltd v Chief Commissioner of State Revenue [2019] NSWCATAD 145 where the Tribunal found that payments made by patients to the Practice where made as a matter of convenience in a way quite similar to using the Practice as a bank. Contrastingly, the Tribunal in Thomas and Naaz Pty Ltd v Chief Commissioner of State Revenue [2021] NSWCATAD 259 found that the availability of the Medicare benefits which was made to the GPs was a direct consequence of the provision of the services provided by the GPs to the Practice.

It would be interesting to see how future cases considering payroll tax in the context of medical practices or other entities that purport to act as mere payment collection agents in the employer/contractor context would apply this case with Homefront Nursing and Thomas and Naaz. In particular, [68] of the Tribunal's decision in Thomas and Naaz presents an interesting question in regard to [179 – [181] of the Uber case given an indirect relationship between the work done and payments is sufficient:

"There is a clear relationship between the provision of the services and the Payments. The availability of the Medicare benefits to the Doctors was a direct consequence of the provision of the services. The Payments were the amount of those benefits less a 30 per cent deduction. Whilst the relationship between the provision of the services and the Payments was not direct, there was a clear indirect relationship sufficient to satisfy the terms of the section. There is nothing in the context of the section nor its legislative history to suggest that such a relationship is insufficient."

Again, this decision may not be set in stone given that the Chief Commissioner has 28 days from the 6th September to appeal the decision.

Should you wish to discuss the above, please contact Tony Pointon and Andrew Pointon of our Taxation Team.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.