- with readers working within the Aerospace & Defence industries

- within Criminal Law, Privacy and Law Department Performance topic(s)

- with Finance and Tax Executives

Key Takeaways:

- Many states offer pass-through entity taxes to bypass the state and local tax (SALT) cap, but elections require careful modeling to avoid unexpected tax impacts — especially for nonresidents.

- SALT issues like sales tax, transfer taxes, and entity classification should be addressed early in liquidity events, reorganizations, or expansions to maximize savings.

- New guidance limits protections for online sellers, requiring nexus reassessments and potential compliance adjustments before year-end.

—

With thousands of taxing jurisdictions from school boards to states and many different types of taxes, state and local taxation is complex. Each tax type comes with its own set of rules — by jurisdiction — all of which require a different level of attention.

This state and local tax (SALT) guide can help your company with 2024 year-end tax planning considerations and guidance to hit the ground running in 2025.

State Pass-Through Entity Tax Elections

Roughly 36 states now allow pass-through entities (PTEs) to elect to be taxed at the entity level to help their residents avoid the $10,000 limit on federal itemized deductions for state and local taxes (the "SALT cap"). Those PTE tax (PTET) elections are much more complex than simply checking a box to make an election on a tax return. Although state PTET elections are meant to benefit the individual members, not all elections are alike, and they are not always advisable.

Before making an election, a PTE should model the net federal and state tax benefits and consequences for every state where it operates — as well as for each resident and nonresident member — to avoid unintended tax results. Before the end of the year, taxpayers should thoroughly consider whether to make a state PTET election — modeling the net tax benefits or costs, and evaluating timing elections, procedures, and other election requirements. If those steps are completed ahead of time, the table has been set to make the election in the days ahead.

When considering a state PTET election, a key question is whether members who are nonresidents of the state for which the election is made can claim a tax credit for their share of the taxes paid by the PTE on their resident state income tax returns. If a state does not offer a tax credit for elective taxes paid by the PTE, a PTET election could result in an additional state tax burden that exceeds some members' federal itemized deduction benefit.

Therefore, as part of the pre-year-end evaluation and modeling exercise, PTEs should consider whether the election would result in members being precluded from claiming other state tax credits — which ordinarily would reduce their state income tax liability dollar for dollar — to receive federal tax deductions that are less valuable.

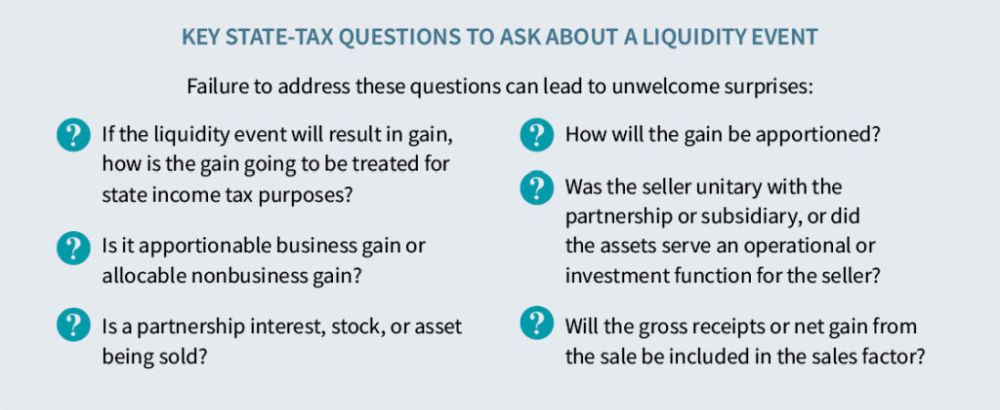

Liquidity Events

Liquidity events take the form of IPOs; financings; sales of stock, assets, or businesses; and third-party investments. Those events involve different forms of transactions, often driven by business or federal tax considerations. Unfortunately, and far too often, the SALT impact is ignored until the eleventh hour — or later.

A liquidity event is not an occasion for surprises. When contemplating any form of transaction, state and local taxes can't be overlooked. Doing so can result in a shock for the client and, at the least, embarrassment for the practitioner. SALT professionals can identify planning opportunities and point out potential pitfalls, and it is never too early to involve them. If you don't consult them until after the transaction occurs or the state tax returns are being prepared, you've left it too late.

From state tax due diligence to understanding the total state tax treatment of a transaction to properly reporting and documenting state tax impacts, addressing SALT at the outset of a deal is critical. If involved before the year-end liquidity event, SALT professionals can suggest tweaks to the transaction that may be federal tax neutral but could identify significant state tax savings or costs now rather than later. After the liquidity event, because the state tax savings or costs already have been identified, they can be properly documented and reported post-transaction. Further, because SALT experience was involved at the front end, state tax post-transaction integration, planning, and remediation can be pursued more seamlessly.

Income/Franchise Taxes

If anything has been learned from the last seven years of federal tax legislation, it's that state income tax conformity cannot be taken for granted. While states often conform to many federal tax provisions, are you certain an S corporation is treated as such by all the states where it operates? Is that federal disregarded entity disregarded for state income tax purposes as well? Not asking the question can lead to the wrong result.

Several states don't conform to federal entity tax classification regulations. Some, including New York, require a separate state-only S corporation election. New Jersey now allows an election out of S corporation treatment. Making those elections — or not — can lead to different state income tax answers, but you should make that decision before the transaction, not when the tax return is being prepared.

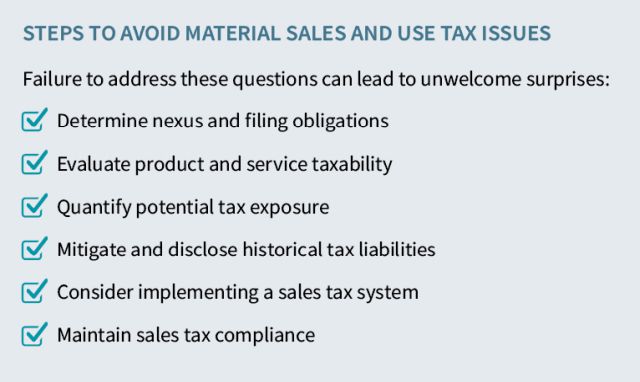

Sales/Use Taxes

Most U.S. states require a business to collect and remit sales and use taxes even if it has only economic, not physical, presence. Remote sellers, software licensors, and other businesses that provide services or deliver their products to customers from remote locations must comply with state and local taxes.

Left unchecked, those state and local tax obligations — and the corresponding potential liability for tax, interest, and penalties — will grow. Moreover, neglecting your sales and use tax obligations could result in a lost opportunity to pass the tax burden to customers as intended by state tax laws.

A company could very well experience material sales and use tax obligations resulting from a sale even though the transaction or reorganization is tax free for federal income tax purposes.

Real Estate Transfer Taxes

Most states impose real estate transfer taxes or conveyance taxes on the sale or transfer of real property, or controlling interest transfer taxes on the sale of an interest in an entity holding real property. Few taxpayers are familiar with real estate transfer taxes, and the complex rules and compliance burdens associated with those state taxes could prove costly if they are not considered up front.

Property Taxes

For many businesses, property tax is the largest state and local tax obligation and a significant recurring operating expense that accounts for a substantial portion of local government tax revenue. Unlike other taxes, property tax assessments are "ad valorem" — meaning they are based on the estimated value of the property. Thus, they could be confusing for taxpayers and subject to differing opinions by appraisers, making them vulnerable to appeal. Assessed property values also tend to lag true market value in a recession.

Property tax reductions can provide valuable above-the-line cash savings, especially during economic downturns when assessed values may be more likely to decrease. The current economic environment amplifies the need for taxpayers to avoid excessive property tax liabilities by making sure their properties are not overvalued.

Annual compliance and real estate appeal deadlines can provide opportunities to challenge property values. Challenging a jurisdiction's real property assessment within the appeal window could reduce related tax liabilities. Taking appropriate positions related to any detriments to value on personal property tax returns could reduce those tax liabilities. Planning for and attending to property taxes can help a business minimize its total tax liability.

P.L. 86-272

The Multistate Tax Commission (MTC) adopted a revised statement of its interpretation of P.L. 86-272 which, for practical purposes, largely nullifies the law's protections for businesses that engage in activities over the internet. To date, California and New Jersey have formally adopted the MTC's revised interpretation of internet-based activities, while Minnesota and New York have proposed the interpretation as new rules. Other states are applying the MTC's interpretation on audit without any notice of formal rulemaking.

P.L. 86-272 is a federal law that prevents a state from imposing a net income tax on any person's net income derived within the state from interstate commerce if the only business activity performed in the state is the solicitation of orders of tangible personal property.

To qualify, the orders must be sent outside the state for approval or rejection and, if approved, must be filled by shipment or delivery from a point outside the state.

Online sellers of tangible personal property that have previously claimed protection from state net income taxes under P.L. 86-272 should review their positions. Online sellers that use static websites that don't allow them to communicate or interact with their customers — a rare practice — seem to be the only type of seller that the MTC, California, New Jersey, and other states still consider protected by P.L 86-272.

The effect of the MTC's new interpretation on a taxpayer's state net income tax exposure should be evaluated before the end of the year. Structural changes, ruling requests, or plans to challenge states' evolving limitation of P.L. 86-272 protections applicable to online sales can be put into place.

However, nexus or loss of P.L. 86-272 protection can be a double-edged sword. For example, in California, if a company is subject to tax in another state using California's new standard, it is not required to throw those sales back into its California numerator for apportionment purposes.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.