COVID-19 isn't entirely behind us, but everyday life has largely resumed a semblance of normalcy and most Americans are back to living as they did before the pandemic. That is not to say we will be resuming all our pre-pandemic lifestyles and habits. COVID-19 forced many changes upon us, some of which we are eager to ditch (e.g., virtual Happy Hours) and others that will stick to some degree (e.g., teleworking). For large retailers, understanding what pandemic-induced changes in shopping habits will stick with their customers is critical to planning the path forward.

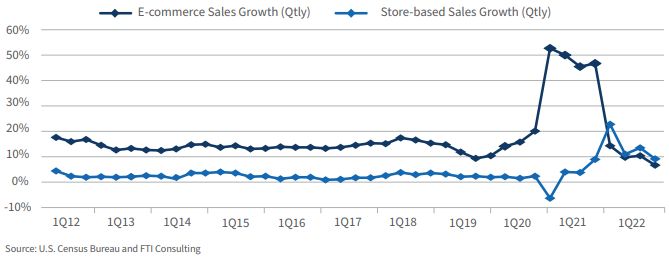

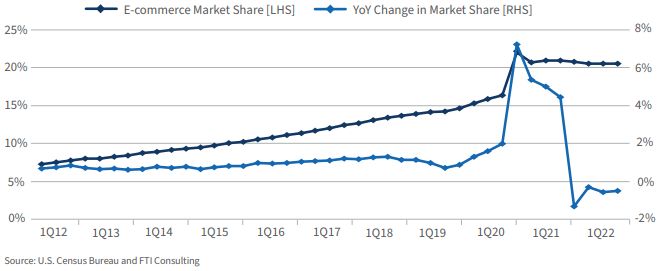

U.S. E-commerce1 retail sales enjoyed four quarters of hypergrowth from 2Q20 through 1Q21, during which time quarterly online sales growth (YoY) ranged from 45% to 53% compared to a consistent low- to mid-teen growth rate in the years preceding the pandemic — or the equivalent of nearly three years of sales gains in those four quarters (Exhibit 1), while online market share approached 21% (Exhibit 2). Online retail sales grew by nearly 43% in 2020 and another 18% in 2021 (much of it in 1Q21), even more than previous estimates, as the U.S. Census Bureau recently revised its online retail sales data for 2020 and 2021 materially higher than it originally reported. As much as e-commerce prospered during the pandemic, it was even better than first thought, with online retail sales over this two-year period revised upward by $140 billion from what was initially reported,2 or about 9% higher, further amplifying its standout performance. Consequently, U.S. e-commerce retail sales (LTM) are poised to hit the $1 trillion mark in 3Q22, representing a doubling of sales in just four years.

The COVID-19 pandemic was a huge boon for online shopping, but the question all along has been whether these market share gains would be retained once shoppers were free to roam stores safely again. So far it seems so, with online market share gains mostly holding through 1Q22 even as the channel's sales growth has slowed, with just a bit of backslide in market share over the last few quarters (Exhibit 2). Online shoppers surged in number and purchasing volumes during the COVID-19 episode, whether by choice or necessity, and most were satisfied enough with the experience that they haven't reverted to their pre-pandemic shopping ways now that it's safe to shop in stores again.

Exhibit 1 — Retail Sales Growth (YoY): E-commerce vs. Store-based

Exhibit 2 – E-Commerce Market Share of U.S. Retail Sales (excluding Auto & Gas)

2021 Was a Jubilee Year for Most Retailers Regardless of Channel

As insensitive as it may sound, the COVID-19 pandemic was the best thing to happen in decades for large omnichannel and online retailers, as it transformed the retail landscape in favor of the largest and most tech-evolved incumbents. This windfall for large retailers had several contributing causes, namely:

- stay-near-home living conditions that effectively forced most Americans to shop online more frequently and reduced competition from smaller store-based retailers;

- a surfeit of free time and personal savings for millions who were able to work from home for months;

- a redirection of consumer spending towards goods and away from services for housebound shoppers and;

- nearly one trillion dollars of financial stimulus payments paid indiscriminately to about three quarters of American households by Uncle Sam, much of it when the economy was already well on its way to recovery.

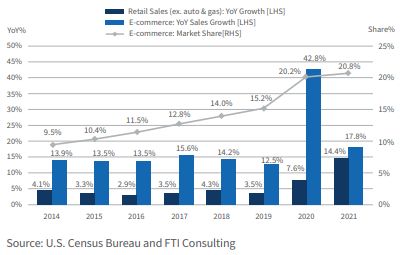

The result was an overstimulated economy, a huge spending spree by shoppers since late 2020, more entrenched supply-chain bottlenecks and accelerating inflation. Total nominal (i.e., not inflation adjusted) retail sales (excluding auto and gas) increased by 7.6% in 2020 (even with most non-essential retail stores shut down from late March through May) and by an astounding 14.4% in 2021, easily the best two-year period on record for the retail sector (Exhibit 3). (Nominal retail sales growth has averaged about 4.5% annually this century.) Despite consumers' voiced concerns about inflation becoming problematic, most shopped with abandon last year and into early 2022. The primary takeaway in retailing last year was that shoppers spent like crazy, unlike any spending splurge we can recall, and that benefitted most large retailers irrespective of shopping channel. Don't expect it to happen again any time soon.

Today, consumers' concerns over a lingering virus and its variants have taken a back seat to heightened anxieties about high inflation, the exhaustion of pandemic-related financial relief, rising interest rates and the Fed's determination to slow down the economy, which will impact jobs and personal finances to varying degree. Total retail sales growth will slow markedly over the balance of 2022, mostly because abnormally high sales growth of the last two years isn't sustainable, with much of it attributable to hoarding and then splurging, paid for with a pandemic-driven financial windfall that has been dissipated for many Americans. Furthermore, most adults today have no personal experience or recollection of living in a high-inflation environment and, beyond the financial damage it inflicts, it has become the primary source of stress for consumers, who don't know how long it will persist or whether the remedy will be worse than the disease.

Not only will retail sales growth weaken over the remainder of this year, but inflation will take a bigger bite of sales for most retailers, many of whom are reluctant to fully pass on cost increases to shoppers. As bad as price shocks have been for consumers, many retailers have been absorbing some product and fulfillment cost increases for fear of alienating shoppers. It's not clear how much longer retailers can afford to do this if cost increases continue at a high rate, and several large retailers, including Walmart,3 Target4 and Kohls5, have already warned about contracting gross margins and operating margins over the balance of 2022 despite expectations of positive sales growth.

Exhibit 3 — Retail Sales Growth: CAGR of 2-Year Stack

E-commerce Sales Decelerating from Pandemic Hypergrowth

Following huge pandemic-induced gains in sales and market share in 2020, many thought that e-commerce retailing would experience a pause or contraction in 2021 as Americans began to leave the house, resume their external lives and shop less often from their living rooms. It didn't quite play out that way until later in the year. While the COVID vaccine rollout made it safe for most Americans to be out and about again by mid-2021, COVID-19 variants, particularly the Delta variant, created rolling waves of new cases and lingering anxiety across the country that delayed the return of normal living. We tend to forget that COVID-19 was responsible for far more deaths nationally in 2021 than in 2020 despite nationwide vaccine availability.

Consequently, many Americans did not fully resume their pre-COVID lifestyles in 2021, even among the vaccinated. This slower-than-expected return to normal life continued to disproportionately benefit online retailing, especially in the early months of 2021 when vaccine uptake was just underway. E-commerce retailing again registered huge gains in sales and market share in 1Q21, but that was the channel's last boost from the pandemic. Thereafter, consumers returned to stores in considerably greater numbers, and online sales growth slowed measurably over the balance of the year. Store-based sales growth has exceeded online sales growth for the last four quarters (Exhibit 2), something that hasn't happened since online shopping became a thing.

Going forward we expect annual online sales growth to moderate near a low-double-digit rate in the next couple of years and decelerate further over the balance of the decade as the e-commerce channel approaches maturity. Nonetheless, online sales growth should exceed overall retail sales growth by a factor of two through 2030, thereby adding to its market share at a slowing rate. Online sales in several product categories, such as apparel, sporting goods, and toy & hobby, are past peak growth rates, and the channel's growth from here on will depend mostly on lower penetration categories, such as grocery and home improvement, where online market share potential is smaller. Online grocery suddenly became a $100 billion category during the pandemic, but it may not provide such high sales growth for the channel in a post-pandemic economy.

Exhibit 4 — U.S. E-commerce Retail Sales

On an LTM basis, e-commerce market share of total retail sales (excluding auto & gas) jumped to 20.2% in 2020 (Exhibit 4), a pickup of 500 basis points in one year, and subsequently gained another 60 bps in 2021, finishing the year with close to 21% of market share. However, on a quarterly basis that better reflects recent change, e-commerce market share has slipped slightly for three consecutive quarters, reflecting decelerating e-commerce growth and improving store-based sales as shoppers increasingly return to stores. For those who were concerned about the possibility of a material reversal of market share gains in a post-COVID environment, this is a very impressive hold for e-commerce, though some more slippage could continue in the quarters ahead. While it's still early to reach any definitive conclusion, it appears that e-commerce will retain much or most of the hard-fought share gains it won during the pandemic. Some givebacks should be expected, particularly in categories like grocery, where online grocery sales have decreased slightly so far in 2022 but remain far above pre-pandemic levels, which is what really matters.

Has Amazon Peaked?

As the leading online retailer in North America, Amazon certainly has benefitted from soaring online sales since the pandemic hit, but its performance, as measured by retail sales growth and market share, took a slight hit in 2020-21. This shouldn't be entirely surprising, as its largest competitors have greatly improved their omnichannel businesses since COVID after years of lagging performance.

With nearly $400 billion of incremental retail sales flowing to the online channel over the last two years (compared to our pre-COVID forecast), shoppers have spread around their business to a host of large sellers, particularly in the grocery and other consumables categories, so Amazon couldn't have been expected to maintain the estimated 41% online market share we believe it held just prior to COVID-19. There are plenty of other competitive alternatives for shoppers, namely the large general merchandisers/ big box retailers such as Walmart and Target, as well as the giant supermarket chains, most of which have stepped up and excelled in meeting shoppers' high demands during COVID. This was particularly appealing to shoppers given the broadening product categories they were purchasing online during the height of COVID and their highly varied preferences for pickup/delivery and returns. Consequently, Amazon was sure to see its share of these incremental sales fall below its pre-pandemic online market share.

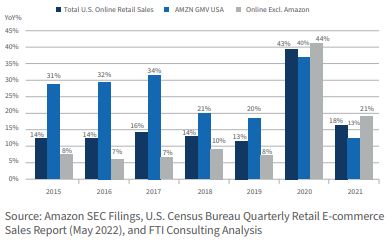

Amazon's domestic annual online retail sales growth, which had handily outpaced such growth for the rest of the channel from 2015 to 2019, suddenly trailed the rest of online in 2020-2021 (Exhibit 5) for the first time, and notably so in 2021, as large omnichannel retailers were the biggest beneficiaries of the pandemic. Amazon's online retail sales growth (YoY) has been less than 10% for the last three quarters, the first time we can recall consecutive quarters that its retail sales didn't achieve double-digit growth.

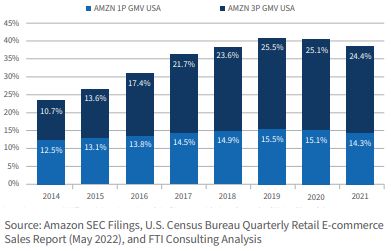

Consequently, we estimate Amazon's online market share slipped approximately 200 bps over the last two years, to 38.7% in 2021 (Exhibit 6). That's hardly alarming but going forward it's reasonable to expect this trend may persist, as omnichannel retailers continue to be more competitive with Amazon while shoppers increasingly appreciate the unique conveniences of the omnichannel experience and the price competitiveness of other large online sellers. Moreover, other online sellers (omnichannel included) collectively have more room to grow than Amazon does. Nonetheless, Amazon will remain the nation's leading online retailer, but if this trend holds and omnichannel remains ascendant, the opportunity for Amazon to take significant additional market share may be diminished.

Amazon has returned Prime Day to its traditional mid-July slot after having moved it around to June 21-22 last year and October 13-14 in 2020. Prime Day 2022 comes at a particularly vulnerable moment for the retail sector, with shoppers increasingly concerned about the condition of the economy and their personal finances. Most Americans have very negative views about "the direction the country is headed" — whatever that means exactly — for a variety of reasons, and consumer sentiment is at near record lows despite a growing U.S. economy. It's not a great moment for American consumers by many measures, and if ever there was a year when Prime Day wasn't set up to be a blowout success by Amazon standards, this would seem to be it.

And just to keep us on our toes, Amazon recently announced a second Prime event, tentatively labeled "Prime Fall," scheduled for some time in the fourth quarter — the first time it has held two Prime events in a calendar year. It's hard to discern what to make of this development, whether it's an opportunistic early grab at the holiday shopping season or an improvised attempt to jumpstart sales momentum following several quarters of uncharacteristic and uninspired growth from Amazon. Investors hardly reacted to the news and are more concerned about the prospect of flagging consumer spending as the economy weakens. Surprisingly, Amazon's stock price is just fractionally above its pre-COVID valuation.

Exhibit 5 — U.S. E-commerce Retail Sales Growth

Exhibit 6 — Amazon Market Share of U.S. E-commerce Sales

FTI's Consulting U.S. Online Retail Forecast

There's persuasive evidence so far that COVID-19's impact on e-commerce shopping will be enduring, and that assumption has been incorporated into our forecast model. We continue to utilize a logistic growth model (or S-curve) to forecast online retail sales and market shares in the decade ahead. The model was developed using historical online sales and market shares since 2000 to quantify a best-fitting logistic curve equation and is revised annually as additional online sales data become available. A logistic curve is the most suitable growth model to apply to the trajectory of online sales.

We project U.S. online retail sales will hit $1.07 trillion in 2022, an increase of 11.7% over 2021 and consistent with the pre-pandemic growth trajectory for the channel. Our 2022 forecast represents incremental online retail sales of $256 billion above our pre-pandemic forecast model (Exhibit 7). Several years ago, we projected that online retail sales wouldn't hit the trillion-dollar mark until 2025, but the impact of COVID-19 upended those expectations.

As for market share, our forecast model puts the online channel's share of U.S. retail sales (excluding auto & gas) at 22.1% by year-end compared to 20.8% in 2021 and 15.2% in 2019, an impressive gain of nearly 700 basis points (bps) over three years compared to annual market share gains of about 130 bps prior to COVID. However, we expect online market share gains going forward will slightly trail our pre-COVID estimates, as the pandemic pulled forward e-commerce adopters who would have migrated to the channel in subsequent years. In other words, some portion of sizeable market share gains in 2020-2021 was taken from future years, thereby reducing what those future gains would have been. Of the incremental 360 bps of market share that the online channel took in 2020 (that is, above what it would have gained had COVID not happened), approximately 230 bps will be retained by decade end, with the slippage attributable to slightly slower online sales growth and market share gains from 2022 to 2030 compared to our pre-COVID model.

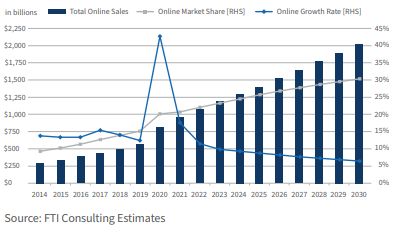

We project U.S. online retail sales will surpass $2.0 trillion by 2030 (Exhibit 8), while total online market share will approach 31% by the end of the decade compared to 21% at the end of last year. This represents a compounded annual growth rate (CAGR) for online sales of nearly 8.5% over the rest of this decade, considerably less than its historical pre-COVID growth, as the online channel begins to experience the limits of its growth potential.

Exhibit 7 — U.S. E-commerce Retail Sales (in billions)

Exhibit 8 — E-commerce Retail Sales, Growth & Market Share

Conclusion

Everyday life is quickly getting back to normal for most Americans in 2022 yet won't be the same as it was prior to the arrival of COVID-19. We shop differently now than we used to, and it has become evident since mid-2021 that the pandemic's impact on online shopping wasn't merely a one-time boost that will go away with the virus itself, as stimulus checks were. New shopping habits acquired during the pandemic are mostly sticking despite a recent revival of store-based shopping from dismal levels in 2020. In particular, the apparel categories and supermarkets saw shoppers return to stores last year, as waistlines and appetites both grew during the pandemic while wardrobes were neglected. However, consumers' reengagement with in-store shopping could prove to be short-lived once we remember how tiresome the experience had become in pre-COVID times. For now, it's still a novelty. Moreover, sky-high fuel prices mean that financially stressed consumers will be making fewer shopping trips —which will be consolidated, more targeted and less leisurely. This could also reinvigorate online shopping among cost conscious consumers try to save a few gas bucks.

As for the online channel, the party is over but there will be no hangover regardless of how and where people choose to shop in the year ahead. Its near-term fortunes largely will be dictated by how well consumer spending holds up overall. Total retail spending remained surprisingly strong through 1Q22 but has slowed in recent months, and that trend should continue as inflation persists and discretionary spending cutbacks occur. Robust spending by more affluent shoppers who aren't as sensitive to rising inflation has helped compensate for a growing cohort who are now pulling back, so the profile of a retailer's core customer base remains as determinative as ever. For hard-pressed shoppers who are sensitive to online delivery charges and other ancillary costs, any price hikes or surcharges for fulfillment will be weighed against competitors' policies as well as the gasoline costs of driving to stores instead. Price-sensitive shoppers go through these calculations regularly. For online sellers, delivery and returns costs have always been a margin killer, never more so than today, and there are some hard decisions ahead should inflation in these areas continue to increase.

Footnotes

1. E-commerce and online retailing are terms used interchangeably throughout this report and refer to the purchase of merchandise where the transaction is consummated electronically from either an online-only or an omnichannel retailer, irrespective of how a customer takes receipt of the merchandise.

2. U.S. Census Bureau and FTI Consulting

3. Melissa Repko, Lauren Thomas and Amelia Lucas. Here's what Walmart, Target, Home Depot and Lowe's Tell Us About the State of the American Consumer. CNBC, 2022.

4. Aishwarya Venugopal and Uday Sampath Kumar. Target Warns of More Margin Squeeze As Excess Inventory Weighs. Reuters, 2022.

5. Uday Sampath Kumar. Kohl's Cuts Profit Forecast, Becomes Latest Retailer to Warn of Inflation Pain. Reuters, 2022.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.