- within Finance and Banking topic(s)

- with readers working within the Banking & Credit, Property and Retail & Leisure industries

Introduction

The single most important question in every private equity conversation about an Am Law 100 law firm affiliated management services organization (MSO) is also the simplest. How does the capital come back out? Private equity operates on a fund-cycle timeline. A sponsor that acquires a stake in a law firm MSO in 2027 generally aims to return capital to its limited partners by 2033 or 2035. An Am Law 50 firm generating USD1.5B in revenue with healthy margins could produce MSO-level EBITDA that, at a reasonable multiple, implies enterprise value in the tens of billions of dollars. Even an Am Law 75–100 firm could produce MSO valuations in the high single-digit billions. The universe of PE firms capable of writing a check at that scale is small. Blackstone, Apollo, or KKR could theoretically acquire an Am Law 100 MSO at that valuation. But the exit question simply moves one level up. Who do Blackstone, Apollo, or KKR sell to? A PE-to-PE flip makes sense at USD500M. It becomes much more structurally difficult at USD5B or above. The initial public offering may represent the most efficient mechanism for recovering capital at that scale. It converts a private, illiquid stake into publicly traded equity with daily price discovery and a liquid secondary market. Without a viable path to public markets, the PE investment thesis for Am Law 100 MSOs becomes significantly more difficult to sustain. Capital goes in, but there are limited options for it to come out at an appropriate return. This exit constraint is the primary driver of the law firm IPO discussion.

The American legal industry sits at an inflection point. Over the past twelve months, private equity investment in law firm MSOs, and the rise of law firms built on alternative business structures (ABS) in the jurisdictions that permit them, has accelerated dramatically. Properly structured, the MSO has become something the profession has never had before. It is a repeatable, financeable platform. The signal is difficult to ignore. Morgan & Morgan, the largest U.S. personal injury firm, has hired JPMorgan to explore a minority stake sale that could pave the way for a public listing, a deal that could raise more than USD1B and bring in a partner seasoned in executing initial public offerings. Morgan & Morgan’s plaintiff-side model is not directly analogous to the Am Law 100, but the message is clear. The investment banking community now treats a law firm MSO IPO as a bankable proposition. Outside capital is already flowing into American law firms. The open questions are whether the public markets are a viable destination and what structural and regulatory architecture it would take to get there.

This article examines how an initial public offering could actually work for a diversified, full-service Am Law 100 firm by:

- addressing the tax structure and revenue-recognition issues that will concern underwriters

- mapping the regulatory terrain across the jurisdictions that matter most

- drawing cautionary lessons from the jurisdictions where law firm IPOs have already been tested

- laying out a practical roadmap from partnership vote to opening bell.

The economic case for public capital

Law firms possess characteristics that institutional investors may find deeply attractive. Revenues are recurrent and predictable. Profit margins are high and capital expenditure requirements are relatively low. The competitive market remains fragmented enough to support consolidation as evidenced by revenue concentration within the Am Law 5 and increased recent merger activity within the Am Law 200. These are the same characteristics that drew private equity into accounting firms and investment banks in earlier decades. All of those industries eventually accessed public capital markets.

The professional services sector has followed a clear historical arc. Investment banks went public in the 1ft80s and 1ftft0s. Accenture, born from Arthur Andersen’s consulting arm, completed its IPO in 2001. CPA firms began accepting private equity investment in 2021. The sector recorded more than 80 deals in 2025 alone, including Blackstone’s acquisition of Citrin Cooperman at approximately USD2B in valuation. Law firms have been the last major professional services category to remain closed to outside capital but that closure has ended.

The current MSO model has demonstrated that outside capital can participate in the economics of a law firm without violating fee-sharing prohibitions or professional independence requirements. Under this model, investors acquire the firm’s back-office operations with the legal practice entity retaining legal fee revenue but paying an MSO a fair market value flat fee or cost-plus services fee. The MSO model does, however, have structural limitations. Investors are confined to the services fee stream and cannot participate directly in legal fee revenue. This constrains returns relative to what a full equity stake or public listing would provide in an ABS model firm, for example.

An IPO could break through that ceiling. It would offer law firm partners full liquidity and public market valuations. It would create equity currency for acquisitions and lateral hiring, and it would enable the kind of stock-based compensation that listed UK law firms have already used to meaningful competitive effect.

But an IPO also solves a more fundamental problem that managing partners and executive committees have raised in virtually every exploratory conversation we have had about PE investment. Who do we exit to? This concern has stalled more exploratory conversations than any regulatory or structural issue. As described in the opening of this article, the scale of an Am Law 100 MSO makes the exit question existential rather than academic. The IPO may be the mechanism that makes PE investment in Am Law 100 law firms most compelling at scale

The IPO thesis depends on public markets assigning a platform multiple, in the range of 15–20× EBITDA comparable to technology-enabled professional services companies, rather than a service-contract multiple of 6–8×. The distinction is critical. If the market prices an MSO as a simple outsourcing vendor, the IPO does not solve the exit problem. If it prices the MSO as a scalable platform with recurring revenue, embedded switching costs, and technology-driven margin expansion, the economics work. Establishing that the MSO qualifies for platform-level multiples will be a central task of the pre-IPO positioning and underwriting process, and firms considering this path would benefit from engaging investment banking advisors with professional services IPO experience early in Phase Two to validate this assumption. The IPO is not the final step in the roadmap we lay out below. It could be the step that gives every prior step its fullest economic rationale.

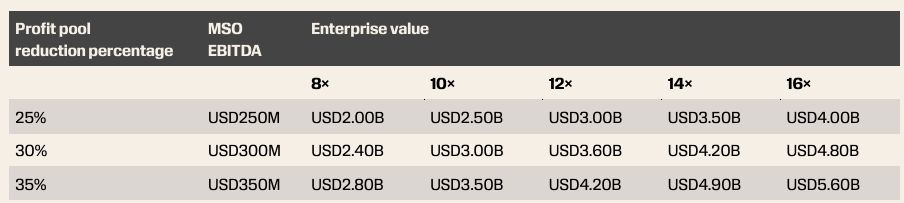

Exhibit 1: Illustrative MSO valuation sensitivity

The table below illustrates how MSO enterprise value scales with both the compensation scrape and the valuation multiple1. It assumes a representative Am Law firm with USD2B in revenue and a USD1B partner profit pool, reflecting a distributable-profit margin and scrape rates consistent with comparable platforms. MSO EBITDA is derived through the payment of one or more fair market value fees, which are funded through a reduction in the partner profit pool that would otherwise be payable in distributions to partners. Enterprise value is MSO EBITDA multiplied by the indicated multiple. The distinction between a service-contract multiple (6× to 8×) and a platform multiple (12× to 18×) is the entire economic premise of the IPO thesis.

At a 35% reduction to the profits available for distribution to the partners, repricing the same USD350M of MSO EBITDA from an 8× service-contract multiple to a 15× platform multiple could lift enterprise value from roughly USD2.8B to roughly USD5.25B. The roughly USD2.5B of incremental value would be created not by additional earnings but by the market’s willingness to treat the MSO as a scalable platform rather than a captive vendor. Establishing that characterization would be the central task of pre-IPO positioning.

The regulatory landscape: Rule 5.4 and the jurisdictions that matter

The threshold ethics concern for any law firm IPO in the United States is ABA Model Rule 5.4. The rule prohibits the sharing of legal fees with nonlawyers and, by extension, nonlawyer ownership of law firms. Most U.S. jurisdictions follow this prohibition. But the landscape is shifting unevenly, and any credible IPO pathway would need to account for the specific regulatory posture of the jurisdictions where large law firms operate. Appendix A provides a state-by-state overview of the current regulatory status across the jurisdictions that matter most for Am Law 100 firms.

The practical implication is that a law firm IPO could not currently be structured as a direct public offering of equity in the legal practice entity in most major U.S. jurisdictions. The viable path would likely run through an MSO-based structure, with investors owning the management company rather than the law firm itself. An Arizona ABS license offers a theoretical alternative, but ABS firms cannot establish branch offices in jurisdictions that prohibit nonlawyer ownership. For a firm with offices in ten states, that appears to be a non-starter as the primary structure.

The Up-C structure: a tax-efficient architecture for partnership IPOs

If a law firm were to pursue a public listing, the Up-C (umbrella partnership–C corporation) structure could be the natural transactional architecture. The Up-C has become the standard vehicle for taking partnership-based businesses public. Its core advantage is preserving the tax benefits of pass-through status for pre-IPO partners.

In an Up-C IPO, the existing operating partnership remains intact as a pass-through entity. A newly formed C corporation goes public and uses IPO proceeds to buy a majority interest in the partnership that owns the MSO, becoming its managing member. Pre-IPO partners retain their partnership units, which remain taxed as pass-through income. This avoids double taxation that would result from a direct corporate conversion. Over time, partners can exchange their partnership units for publicly traded shares of the C corporation. Each exchange triggers a step-up in tax basis for the C corporation’s proportionate share of partnership assets.

This step-up generates future tax deductions for the C corporation. The value of those deductions is typically shared with the exchanging partners through a Tax Receivable Agreement (TRA), which pays pre-IPO owners 85% of the cash tax savings the corporation realizes. Blackstone, KKR, Carlyle, and Accenture have all used the structure. Each faced analogous structural challenges in transitioning from partnership economics to public ownership.

For a law firm, the Up-C could preserve partner-level pass-through taxation and provide a public currency for acquisitions and compensation without forcing a wholesale restructuring of partnership economics on day one. The structural complexity appears manageable for sophisticated capital markets counsel. The harder question is how the public holding company’s governance obligations would interact with Rule 5.4’s requirements regarding lawyer independence.

The Up-C also supplies timing flexibility that is especially valuable given the unpredictability of IPO windows. Because pre-IPO partners retain exchangeable units rather than receiving cash at listing, partner liquidity can be sequenced over a multi-year horizon through a negotiated exchange schedule, customary post-IPO lock-up periods, and registration rights that govern when and how units convert into freely tradable shares. This staged mechanism allows the firm to calibrate the pace of partner monetization to prevailing market conditions rather than forcing a single liquidity event, and it lets the PE sponsor sell down its position in an orderly fashion as windows open.

To view the article, click here.

Footnote

1. Figures are illustrative and rounded. Multiple ranges are anchored to recent transactions for comparable professional-services and legal-services platforms. Current market conditions place professional-services transactions in a standard 8× to 12× range and premium platforms in a 13× to 17× range, with recent law-firm-MSO and accounting-advisory transactions clustering around 14× to 16× EBITDA. Actual outcomes depend on growth profile, recurring-revenue mix, EBITDA margin, management depth, and market conditions at listing.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]