An aging population, combined with Medicare Advantage, ACO and other value-based payment models, is slowly transforming care delivery. Innovative full-risk primary care companies have emerged during the past few years focused on improved patient outcomes, i.e., fewer hospitalizations, re-admissions and emergency department ("ED") visits while increasing engagement. Insurers, already a presence in physician management, have extended their reach into home care. Urgent care continues its growth trajectory.

Hospitals and health systems have become the largest employer of physicians, primary care and specialists. Shortages of primary care physicians have occurred and are projected to get worse during the next 5-10 years. Academic medical centers have been challenged by their research missions, faculty and community practices, and the need to deliver high-quality lower-cost care. Digital technology is enabling change.

In this article, we address each of these factors and discuss the evolution of primary care in a value-based environment.

Aging population and growth of value-based payments

The U.S. population aged 65 and older is forecast to increase from 56.1 million in 2020 to 73.1 million in 2030, reflecting a compound annual growth rate of 2.7%.1 The elderly population accounting for higher costs — those over 75 years of age — is growing at 4.0% per annum.2 A rapidly aging population, combined with payer and provider consolidation, contributes to rising costs; national healthcare expenditures are projected to reach $6.8 trillion — 19.6% of GDP — in 2030.3

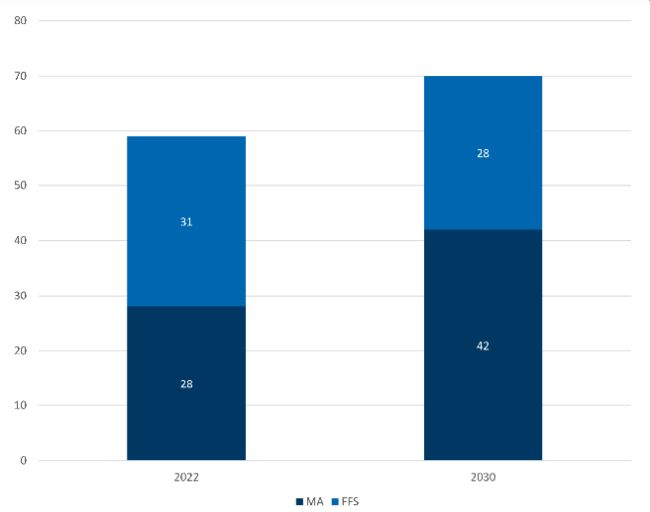

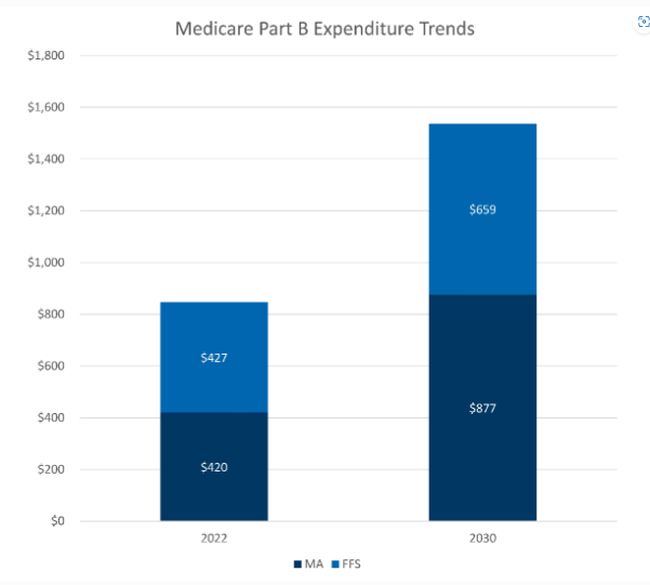

The Medicare Advantage market is projected to increase from a 48% market share in 2022 to 60% in 2030; it currently accounts for 55% of Medicare expenditures.4 The growth in Medicare Advantage enrollment (5.2% compound annual growth rate) is far surpassed by the increase in expenditures (9.8% CAGR).5 Medicare Advantage represents an entrée for providers to capitate payments.

The Case for Capitalism: Medicare Advantage Growth

Medicare Part B Enrollment Trends

Medicare Part B Expenditure Trends

Sources: FTI Consulting; Kaiser Family Foundation What to Know about Medicare Spending and Financing; Centers for Medicare and Medicaid Services National Health Expenditures - Projected

Accountable Care Organizations ("ACOs") represent another source of value-based payments. In 2022, approximately 11.0 million fee-for-service beneficiaries are enrolled in 483 ACOs.6 One-sided (33% of ACOs) and two-sided risks (67%) were taken.7 Total earned shared savings in 2020 were $2.0 billion.8

Medicare Advantage and ACOs account for most Medicare beneficiaries and represent an opportunity to enhance chronic disease management, inclusive of preventive activities.

Physician consolidation and shortages

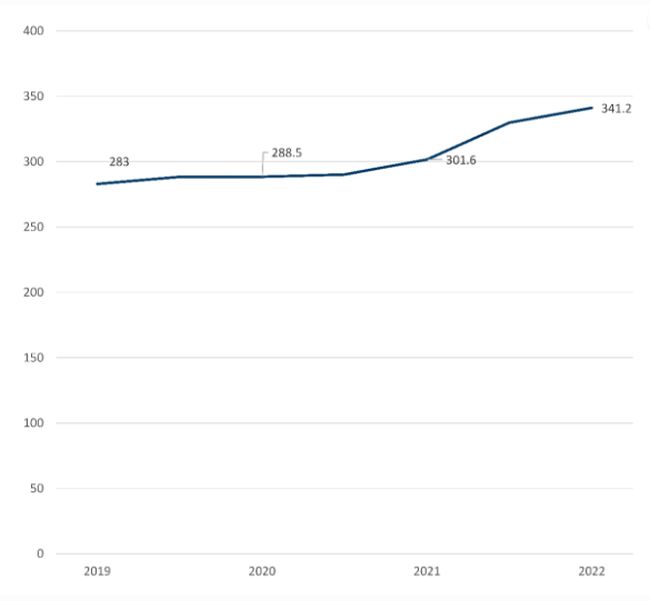

According to a study published by the Physician Advocacy Institute and Avalere Health, 341,200 physicians are employed by hospitals and health systems.9 This represents 41.7% of active physicians involved in patient care.10 An additional 122,200 (14.9%) physicians are employed by corporate entities, such as insurance companies and private equity firms; Optum Care (United) alone employs 60,000 physicians.11,12 Recent acquisitions include Kelsey-Seybold (Houston) and Atrius Health (Massachusetts).13

Physician acquisitions lead to gains in market share, the potential for bundled services, greater control of referrals and higher prices.14 They are also associated with losses (subsidies), which for primary care has a median of approximately $200,000, less than half that of medical and surgical specialties.15

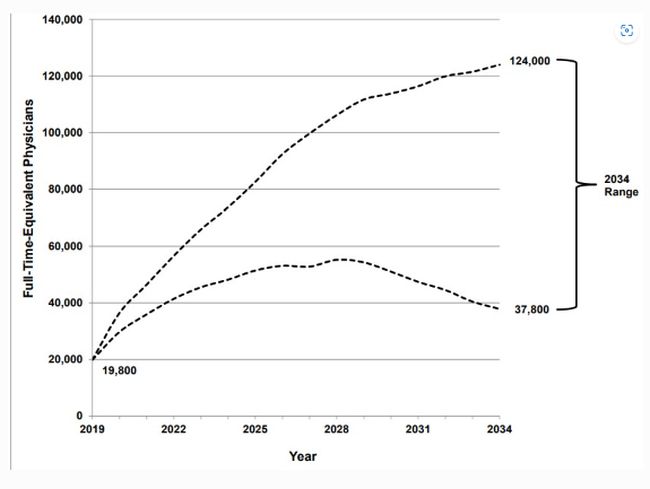

Staff shortages are currently a challenge for most health systems. A primary care shortage of 20,000-40,000 physicians is projected for 2025.16 48.8% and 49% of internal medicine and family-practice physicians, respectively, are more than 55 years old.17

Rising Hospital Employment and Shortage of Primary Care Physicians

Number of Physicians Employed by Hospitals (000)

Projected Primary Care Physician Shortage

Sources: AAMC. The Complexities of Physician Supply and Demand: Projections From 2018 to 2033 https://www.aamc.org/system/files/2020-06/stratcomm-aamc-physician-workforce-projections-june-2020.pdf

PAI-Avalere Health Report on Trends in Physician Employment and Acquisitions of Medical Practices: 2019-2021". Physician Advocacy Institute and Avalere Health (Updated April 2022), http://www.physiciansadvocacyinstitute.org/PAI-Research/Physician-Employment-and-Practice-Acquisitions-Trends-2019-21.f

Payers moving home

Each of the leading MA competitors, apart from BCBS plans, has acquired a home health company during the past 12-18 months. Humana acquired the remaining 60% interest in Kindred at Home ("KAH") in August 2021; UnitedHealth Group ("UHG") announced its acquisition of the LHC Group in March 2022; and CVS Health/Aetna announced its acquisition of Signify Health in September 2022.18,19,20 Kindred Healthcare is currently the largest home health provider, and the LHC Group Inc. is ranked third.21

UnitedHealth Group also acquired Landmark Health, a 24/7 in-home medical group for patients with multiple chronic conditions, in 2021, and naviHealth, a provider of post-acute care services, including in-market care coordinators, predictive decision support and skilled nursing facility assessment tools, in 2020.22,23

Retail providers entering primary care

In October 2021, Walgreens announced a 63% stake in VillageMD, a primary care provider with 230 practices in 15 states and revenues of nearly $1.3 billion.24 The goal is to create a co-located and integrated primary care and pharmacy model.

In November 2022, VillageMD announced the acquisition of Summit Health, the parent of CityMD, with investments from Walgreens and Cigna's Evernorth, which will also become a minority owner in VillageMD.25 Combined, they will have 680 locations in 26 markets and are expected to exceed 1,000 Village Medical at Walgreens primary care clinics within a few years.26

CVS has opened 1,126 Minute Clinics in the U.S.27 Among the healthcare services provided are treatment of minor ailments (e.g., sore throat, rash), immunizations and routine lab tests (e.g., cholesterol, diabetes).28 Behavioral health screening and chronic care management may also be provided.29

CVS is currently "rolling out a virtual [primary] care service that gives consumers access to primary care, on-demand care, chronic-condition management and mental health services."30 Referrals to in-person care are provided as appropriate.31 Team-based care combined with an interoperable EMR will facilitate care coordination and process efficiencies and outcomes. The services will be available to Aetna members and is complementary to its virtual-care strategy.32 CVS recently announced a $100 million investment in Carbon Health; primary-care clinics will be opened within drug store locations.33

Walmart, expanding its presence to 22 clinics in Florida, launched the Walmart Health Research Institute and recently signed a ten-year agreement with UnitedHealth Group.34

Amazon shut down its virtual primary care service offering, Amazon Care in August 2022; it was launched three years prior to its employees and, subsequently to corporations.35 Amazon announced the acquisition of One Medical just prior to the shutdown in July.36 Amazon's customer-centric focus, record of innovation and ability to fund additional medical centers adds value to the transaction. Patients needing prescriptions can utilize Amazon Pharmacy, formerly known as Pillpack.37 Amazon Clinic utilizes two-way text messaging to diagnose and treat common conditions.38

Outcomes of primary care innovators highlight fewer hospitalizations and ED visits

- Revenues $2.28

- 169 Centers in 21 states

- 159k capitated lives

- Emplyees 600+ primary care providers

- Panel approximates 500 patients

- 1/3 providers time used to coordinate care, close care gaps, & proactively plan

- Propritary technology: Canopy

- 2021 revenues One Medical $475M; lora Health $114M

- 188 Centers in 29 markets; 767k members

- One Medical: Commercially oriented, membership-based (concierge), technology enabled primary care platform. Focused on the consumed experience

- lora Capitated MA contracts

- 120 centers in 15 states

- Nearly exclusively Medicare Advantage

- "High touch, preventive primary care"

- Panel 345-450 patients; concierge-style practice

- SDOH-centric

- Proprietarily EMR

- Technology/virtual (on-demand enablement)

- Revenuse $2.7B; 295k members

- 170 centers in six states

- 168k Medicare, 95% of renenues capitated

- Employs 400+ providers

- Panel +/- 400 patients; multiple primary care visits per annum

- Proprirtary technology: CanoPanorama

Source: CanoHealth 3Q22 Results and 2022 Investor Day. Presentation Oak Street Investor presentation at JP Morgan conference, 2023 Chemed and One Medical websites, press releases and podcasts

Other primary-care innovators include Oak Street Health, Cano Health and Chenmed. They all focus on capitated Medicare Advantage lives, have comparatively small physician-panels, utilize care teams and developed proprietary technology platforms.

Urgent Care: Still growing (after all these years)

According to the Urgent Care Association, its membership and patient volume (inclusive of COVID) increased 60% from 2019, whereas patient volume per clinic per day increased 23.4% and emergency department visits decline by 17.2% when an urgent care center opens nearby.39 There are more than 9,600 urgent-care centers in the United States.40 Patient convenience (availability) and affordability drive utilization.

Digital transformation

Digital transformation requires a strategic, longer-term approach and integration with quality improvement initiatives. Digital transformation will accelerate the transition to a value-oriented, proactive, personalized and home-centric delivery model focused on the total cost of care. Primary care, rather than procedure-oriented specialists, requires primacy.

The onset of the COVID-19 pandemic in 2020 saw telehealth utilization increase 63-fold among Medicare fee-for-service beneficiaries, from approximately 840,000 visits in 2019 to 52.7 million in 2020.41 Telehealth is convenient, accessible, and potentially engaging in real time. A FAIR Health analysis from October 2022 found that telehealth represented 5.2% of claim lines (services or procedures listed on an insurance form).42

Remote patient monitoring has been used to track high blood pressure, diabetes, heart disease, chronic obstructive pulmonary disease and other conditions.43 Intervention success occurs most often when:

"(1) targeting populations at high risk; (2) accurately detecting a decline in health; (3) providing responsive and timely care; (4) personalizing care; (5) enhancing self-management, and (6) ensuring collaborative and coordinated care."44 Remote-patient monitoring has been shown to reduce ED visits, hospitalizations, length of stay and hospital stays.45

Conversation assistants (known as chatbots) and text messaging applications are used to provide 24/7 patient support.46 Longer-term AI tools such as OpenAI's ChatGPT and image generators like Stable Diffusion and Dall-E have captured the imagination of developers.47

Primary care evolution (not revolution)

The emerging care delivery model driven by principles of primary care will be supported by technology and incentivized by value-based payments. Patient access and engagement, also known as consumerism, will be essential to improve chronic care management and sustain market share.

Evolution of Primary Care

- Care management

- Comprehensive

- Coordinated (teambased)

- Community-based (social services)

- Continuity (across the continuum)

- Home-based preference

- SDOH-integeration

- Behevioral health integration

- Recurring PMPM revenue

- Higher quality, lower cost care

- Physician productivity and compensation

- Population health risk stratification (analytics)

- IT-enabled use of evidence-based practices

- Quality performance monitoring

- Operational efficiencies

- Digital "front door"

- Community-based clinics/resources

- Urgent care

- 24/7 urgen care line

- Telehealth

In 1998, Edward Wagner, MD, MPH introduced the Chronic Care Model based on six principles: self- management support, delivery-system design, decision support, clinical information systems, organization of healthcare, and community.48 Wagner recognized the centrality of primary care physicians to manage and coordinate the care of aging patients with multiple chronic conditions across the continuum of care. Nurse practitioners and physician assistants are increasingly being used to support primary care physicians.49

The Patient Centered Medical Home ("PCMH") is a model of care incorporating principles from the Institute of Medicine, the Future of Family Medicine and the Wagner Chronic Care.50 Core (aspirational) features of the PCMH include a personal physician, physician-directed medical practice, whole-person orientation, coordinated and/or integrated care, quality and safety, enhanced access and payment reform.51 Many of these features have been adopted by innovative providers in a capitated arrangement.

Social determinants of health ("SDOH") are "conditions in which people are born, grow, work, live, and age, and the wider set of forces and systems shaping the conditions of daily living" that affect a wide range of health and quality-of- life-risks and outcomes.52 Special Supplemental Benefits for the Chronically Ill ("SSBCI") for Medicare Advantage may include meals, food and produce; transportation, air quality, pest control, structural home modifications, education and other offerings.53 A disconnect exists between healthcare systems and social services.

Behavioral health integration remains underpenetrated as 25-33% of patients with chronic disease have co-morbid depression; associated costs are 30-80% higher compared to those with only chronic disease.54

Geisinger at Home, a team-based primary-care initiative for complex comorbid patients generates cost savings of $400-650 per member per month; a reduction in hospitalizations and emergency department visits accounts for much of the decline.55,56

Suggested next steps

- Align physician-compensation strategies and incentives with the transformation to value-based payments

- Adopt digital transformation to accelerate the transition to the future state primary-care model and improve data analytics/reporting capabilities

- Evaluate current staffing models to support physicians as part of a patient centered care team and advance population health initiatives

- Integrate community-based practices with the larger health system to improve access and expand footprint

- Contact Center Optimization efforts and implementation of a digital "front-door" to enhance the patient experience

Bottom line

Healthcare is evolving at an accelerated, though still incremental rate of change. Hospitals and health systems have become the largest employer of physicians. Recent acquisitions of Kelsey-Sebold and Atrius Health highlight the intentions of a major insurer to provide direct healthcare services. Retail entrants are expanding their presence via acquisitions, investment and internal development.

Approximately 40 million Medicare beneficiaries are either in a Medicare Advantage plan or an ACO. Capitated payments can also be found in Medicaid Managed Care Organizations and, to a lesser extent, in commercial plans (e.g., payment bundles). Value-based care and its recurring revenue stream is a core focus of emerging primary-care innovators.

Technology is advancing though the myriad of competitors with similar though nuanced features, and benefits complicate purchasing decisions. Telehealth, remote monitoring and contact centers have become integral to provider-applications focused on the patient experience.

The evolving primary-care market is challenging, but the time is now to develop expertise in risk management, make the requisite investments in decision support and alter the compensation structure. It's easier said than done.

Footnotes

1.Jonathan Vespa, et al. "Demographic Turning Points for the United States: Population Projections for 2020 to 2060." U.S. Census Bureau (Revised February 2020), https://www.census.gov/content/dam/Census/library/publications/2020/demo/p25-1144.pdf.

2."2017 National Population Projections Tables: Main Series. Detailed Age and Sex Composition of the Population, Table 3." U.S. Census Bureau (last visited January 18, 2023), https://www.census.gov/data/tables/2017/demo/popproj/2017-summary-tables.html.

3. "National Health Expenditures, Projected." Centers for Medicare and Medicaid Services (last visited January 18, 2023), https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsProjected

4. Meredith Freed, et al. "Medicare Advantage in 2022: Enrollment Update and Key Trends." Kaiser Family Foundation (August 25, 2022). https://www.kff.org/medicare/issue-brief/medicare-advantage-in-2022-enrollment-update-and-key-trends/.

5. FTI Consulting

6. "Shared Savings Program Fast Facts – As of January 1, 2023." Centers for Medicare and Medicaid Services, Medicare Shared Savings Program (last visited January 18, 2023), https://www.cms.gov/files/document/2022-shared-savings-program-fast-facts.pdf.

7. Ibid.

8. Ibid.

9. "PAI-Avalere Health Report on Trends in Physician Employment and Acquisitions of Medical Practices: 2019-2021". Physician Advocacy Institute and Avalere Health (Updated April 2022), http://www.physiciansadvocacyinstitute.org/PAI-Research/Physician-Employment-and-Practice-Acquisitions-Trends-2019-21.

10. "Physician Specialty Data Report: Active Physicians in the Largest Specialties by Major Professional Activity, 2021". American Association of Medical Colleges (last visited January 17, 2023), https://www.aamc.org/data-reports/workforce/interactive-data/active-physicians-largest-specialties-major-professional-activity-2021.

11. "PAI-Avalere Health Report on Trends in Physician Employment and Acquisitions of Medical Practices: 2019-2021". Physician Advocacy Institute and Avalere Health (Updated April 2022), http://www.physiciansadvocacyinstitute.org/PAI-Research/Physician-Employment-and-Practice-Acquisitions-Trends-2019-21.

12. "About Optum Care." Optum (last visited January 17, 2023), https://www.optum.com/about-us/optum-care.html.

13. Heather Landi. "Optum Continues Buying Spree and Scoops Up Houston-based Kelsey=Seybold Clinic: Report." Fierce Healthcare (April 5, 2022) https://www.fiercehealthcare.com/providers/optum-continues-buying-spree-and-scoops-houston-based-kelsey-seybold-clinic-report

14. Cory Capps, et al. "The effect of hospital acquisitions of physician practices on prices and spending." Journal of Health Economics (May 2018), https://pubmed.ncbi.nlm.nih.gov/29727744/.

15. "Physician Flash Report: October 2022." Kaufman Hall (November 3, 2022), https://www.kaufmanhall.com/insights/research-report/physician-flash-report-october-2022.

16. "The Complexities of Physician Supply and Demand: Projections From 2019 to 2034." AAMC: Physician Workforce Projections (Updated 2021), https://www.aamc.org/data-reports/workforce/data/complexities-physician-supply-and-demand-projections-2019-2034.

17. "Physician Specialty Data Report: Active Physicians by Age and Specialty, 2021." American Association of Medical Colleges (last visited January 17, 2023), https://www.aamc.org/data-reports/workforce/interactive-data/active-physicians-age-specialty-2021.

18. Paige Minemyer. "Humana Completes Acquisition of Kindred at Home." Fierce Healthcare (August 18, 2021), https://www.fiercehealthcare.com/payer/humana-completes-acquisition-kindred-at-home.

19. Paige Minemyer. "UnitedHealth to Acquire Home Health Provider LHC Group in $5B Deal." Fierce Healthcare (March 29, 2022), https://www.fiercehealthcare.com/payers/unitedhealth-acquire-home-health-provider-lhc-group-5b-deal.

20. Press Release. "CVS Health to Acquire Signify Health." CVS Health (September 5, 2022), https://www.cvshealth.com/news-and-insights/press-releases/cvs-health-to-acquire-signify-health.

21. Andrew Donlan. "[Updated] The Top 10 Largest Home Health, Hospice Providers in 2020." Home Health Care News (February 9, 2021), https://homehealthcarenews.com/2021/02/the-top-10-largest-home-health-hospice-providers-in-2020/.

22. Andrew Donlan. "UnitedHealth's Optum Reportedly Strikes Deal for Landmark Health." Home Health Care News (February 21, 2021), https://homehealthcarenews.com/2021/02/unitedhealths-optum-reportedly-strikes-deal-for-landmark-health/.

23. Heather Landi. "Optum Scoops Up Post-Acute Care Company NaviHealth." Fierce Healthcare (May 26, 2020), https://www.fiercehealthcare.com/payer/optum-scoops-up-post-acute-care-software-startup-navihealth.

24. "Walgreens Boots Alliance Makes $5.2 Billion Investment in VillageMD to Deliver Value-Based Primary Care to Communities Across America." Walgreens Newsroom (October 14, 2021), https://news.walgreens.com/press-center/walgreens-boots-alliance-makes-52-billion-investment-in-villagemd-to-deliver-value-based-primary-care-to-communities-across-america.htm.

25. Heather Landi. "Walgreens' VillageMD inks $9B deal to buy Summit Health, marking largest physician deal of the year." Fierce Healthcare (November 7, 2022), https://www.fiercehealthcare.com/providers/walgreens-villagemd-inks-9b-deal-buy-summit-health-expand-healthcare-footprint.

26. Ibid.

27. "Number of MinuteClinic locations in the United States in 2023." ScrapHero: A Data Company (February 1, 2023), https://www.scrapehero.com/location-reports/MinuteClinic-USA/.

28. "Retail Clinics." County Health Rankings & Roadmaps (last visited January 17, 2023), https://www.countyhealthrankings.org/take-action-to-improve-health/what-works-for-health/strategies/retail-clinics.

29. Ibid.

30. Heather Landi. "CVS Health rolls out virtual primary care service." Fierce Healthcare (May 30, 2022), https://www.fiercehealthcare.com/health-tech/cvs-health-rolls-out-virtual-primary-care-service.

31. Ibid.

32: Ibid.

33. Heather Landi. "JPM23: Carbon Health Nabs $100M, CVS Partnership to Pilot Primary Care in Retail Stores." Fierce Healthcare (January 9, 2023), https://www.fiercehealthcare.com/providers/jpm23-carbon-health-nabs-100m-cvs-health-partnership-pilot-primary-care-retail-stores.

34. Jeff Lagasse. "Walmart planning expansion of 16 clinics in Florida in 2023." Healthcare Finance (October 28, 2022), https://www.healthcarefinancenews.com/news/walmart-planning-expansion-16-clinics-florida-2023.

35. Annie Palmer. "Amazon is shutting down its telehealth service, Amazon Care." CNBC (August 24, 2022), https://www.cnbc.com/2022/08/24/amazon-is-shutting-down-amazon-care-telehealth-service.html.

36. Heather Landi. "Amazon scoops up primary care company One Medical in deal valued at $3.9B." Fierce Healthcare (July 21, 2022), https://www.fiercehealthcare.com/health-tech/amazon-shells-out-39b-primary-care-startup-one-medical.

37. "The Pharmacy That Really Delivers." Amazon Pharmacy (last visited January 17, 2023), https://pharmacy.amazon.com/.

38. "The Doctors Orders, Made Easier." Amazon Clinic (last visited January 17, 2023), https://clinic.amazon.com/how-it-works.

39: "Urgent Care Fast Facts." Urgent Care Association (last visited January 17, 2023), https://urgentcareassociation.org/.

40. Joanne Finnegan. "Now More Than 9,000 Urgent Care Centers in the U.S., Industry Report Says." Fierce Healthcare (February 26, 2020), https://www.fiercehealthcare.com/practices/now-more-than-9-000-urgent-care-centers-u-s-industry-report-says.

41. "New HHS Study Shows 63-Fold Increase in Medicare Telehealth Utilization During the Pandemic." CMS.gov Newsroom (December 3, 2021), https://www.cms.gov/newsroom/press-releases/new-hhs-study-shows-63-fold-increase-medicare-telehealth-utilization-during-pandemic#.

42. "Telehealth Utilization Declined Nearly Four Precent Nationally in October 2022." Cision PR Newsire; news provided by FAIR Health (January 10, 2023), https://www.prnewswire.com/news-releases/telehealth-utilization-declined-nearly-four-percent-nationally-in-october-2022-301716914.html.

43. "Telehealth and Remote Patient Monitoring." Department of Health and Human Services (last visited January 18, 2023), https://telehealth.hhs.gov/providers/preparing-patients-for-telehealth/telehealth-and-remote-patient-monitoring/.

44. Emma Thomas, et al. "Factors Influencing the Effectiveness of Remote Patient Monitoring Interventions: A Realist Review." British Medical Journal, 11(8). (August 2021), https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8388293/.

45. "Telehealth and Remote Patient Monitoring." Department of Health and Human Services (last visited January 18, 2023), https://telehealth.hhs.gov/providers/preparing-patients-for-telehealth/telehealth-and-remote-patient-monitoring/.

46. Nicole Owings-Fonner. "Fighting Loneliness and Anxiety: Can a Chatbot Provide Additional Support for Your Patients?" American Psychological Association Services, Inc. (August 2021), https://www.apaservices.org/practice/business/technology/tech-column/mental-health-chatbots.

47. Mike Allen. "Axios AM." Axios (January 19, 2023), https://www.axios.com/newsletters/axios-am?id=1&name=AM/PM&screen=channel.

48. "Changes to Improve Chronic Care." Institute for Healthcare Improvement, (last visited February 9) 2023) s http://www.ihi.org/resources/Pages/Changes/ChangestoImproveChronicCare.aspx.

49. "Practice Requirements for Nurse Practitioners." New York State Education Requirements: Office of the Professions. (last visited February 7, 2023) https://www.op.nysed.gov/professions/nurse-practitioners/professional-practice/practice-requirements

50. "The Patient Centered Medical Home: History, Seven Core Features, Evidence and Transformational Change." Robert Graham Center: Center for Policy Studies in Family Medicine and Primary Care (November 2007), https://www.aafp.org/dam/AAFP/documents/about_us/initiatives/PCMH.pdf.

51. Ibid.

52. "Social Determinants of Health at CDC: What Are Social Determinants of Health?" Centers for Disease Control and Prevention (last visited February 3, 2023) https://www.cdc.gov/socialdeterminants/index.htm.

53. Kathryn Coleman. "Implementing Supplemental Benefits for Chronically Ill Enrollees." Center for Medicare and Medicaid Services, Medicare Drug & Health Plan Contract Administration Group (April 24, 2019), https://www.cms.gov/Medicare/Health-Plans/HealthPlansGenInfo/Downloads/Supplemental_Benefits_Chronically_Ill_HPMS_042419.pdf.

54. "Chronic Conditions and Co-morbid Psychological Disorders." Milliman Research Report. Figure 2 (July 2008), http://www.cbhc.org/wp-content/uploads/2015/11/chronic-conditions-and-comorbid-RR07-01-08.pdf.

55. Susan Morse. "Geisinger at Home offers primary care to populations with chronic or complex conditions." Healthcare Finance (January 20, 2023), https://www.healthcarefinancenews.com/news/geisinger-home-offers-primary-care-populations-chronic-or-complex-conditions?mkt.

56. Janet F. Tomcavage, et al. "Geisinger's Home Care Program Is Cutting Costs and Improving Outcomes." Harvard Business Review (November 6, 2019), https://hbr.org/2019/11/geisingers-home-care-program-is-cutting-costs-and-improving-outcomes.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.