- within Antitrust/Competition Law topic(s)

- with readers working within the Insurance, Property and Construction & Engineering industries

- within Cannabis & Hemp and Insolvency/Bankruptcy/Re-Structuring topic(s)

The wait is over!

On October 10th, the Federal Trade Commission (FTC) unanimously approved the first significant revisions to the Hart-Scott-Rodino (HSR) Act premerger notification regime since its inception over 40 years ago.1 The Antitrust Division of the U.S. Department of Justice ("DOJ") also endorsed the new rules ("Final Rule").2 The Final Rule will not only substantially increase the complexity of filings and the time required to prepare them, but also the burden and costs borne by reporting parties. Unless enjoined by a federal court, these rules will likely go into effect mid-January 2025 (90 days after publication in the Federal Register). The FTC will publish compliance guidance in advance of the Final Rule's effective date.

The Final Rule, which took months to develop, is crafted to provide additional information to the FTC and DOJ (the Agencies) and fill in certain "gaps" in the information that the Agencies routinely receive in connection with significant mergers and acquisitions. The Agencies claim the new rules will enable them to better identify competitively problematic transactions. The Final Rule creates separate disclosure requirements for each of the buying and selling parties, rather than requiring the same information from both sides as has been required historically, and also omits certain requirements for transactions presenting a low risk of competitive harm.

The FTC asserts that despite the additional burden on the parties, the Final Rule will reduce information requests to third parties that the Agencies "routinely rely upon to fill in existing information gaps." The FTC also said merging parties are likely to see some reduction in the Agencies' follow-up information requests. "This additional information will enable the agencies to streamline their initial reviews and make decisions more quickly," according to the DOJ.

Notably, the Final Rule excludes several of the most onerous proposals published in the FTC's initial proposed rulemaking in June, 2023, such as requirements to report on how a deal might affect labor markets, obligations to produce a deal timeline and geolocation information, mandates to produce drafts of transaction-related documents or disclose the names of messaging systems used by the reporting parties, among others.

Below are the most significant changes included in the Final Rule:

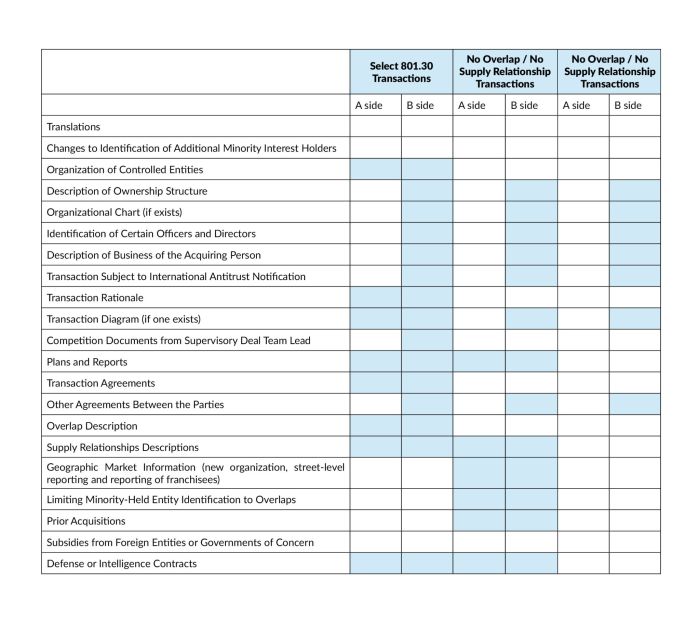

Creation of 3 Transaction Types with Different Tiers of Disclosure Requirements

The most significant structural change in the Final Rule is the creation of three categories of transactions with varying disclosure requirements and two separate HSR forms: one for buyers and one for sellers (requiring less information), to tailor the information requested to transactions with varying levels of complexity and antitrust risk and the type of filer.

- Select 801.30 transactions3 – acquisitions that seldom present competitive concerns, such as executive compensation agreement and certain other open-market transactions reportable under HSR Rule 801.30, the parties reporting such transactions are excused from many of the new disclosure requirements.

- Transactions in which the parties lack a horizontal competitive overlap or a vertical/supply relationship – similarly, such transactions are perceived to create little competitive risk and are exempt from certain of the new disclosure requirements.

- Transactions with competitive overlap or supply relationship – these transactions carry the most onerous disclosure requirements, which are substantially more significant for buyers than sellers.

Changes Impacting Timing: Early Termination and Filing on a Letter of Intent

- Early termination is back – reporting parties will be able to request early termination of the 30-day-statutory HSR Act review period, which may be granted at the Agencies' discretion, but only in limited instances, such as transactions without competitive overlap.4

- Reporting parties will no longer be allowed to file on the basis of a barebones agreement lacking sufficient details about key terms of a proposed transaction. parties will still be able to file on the basis of a fully executed letter of intent or terms sheet as long as material terms are included.

New Substantive Antitrust Disclosure Requirements

- The most critical addition of the Final Rule is the requirement for parties to describe the strategic rationales for the proposed transaction and produce documents that confirm or discuss the rationales along with a "brief" description of horizontal overlaps and vertical supply relationships.

- Parties are required to describe their principal categories of products and services, products and services still in the development stage, and supply relationships. If the parties report a competitive overlap or supply relationship, they also must describe customer categories, identify their top 10 customers and/or describe the development status of the relevant product or service.

Additional Transaction Information and Documents

- The parties are also required to submit:

- Competitive analyses and reports (corresponding to Item 4(c) and (d) documents in the current HSR form) prepared by or for the supervisor of each party's deal team, in addition to officers and directors. The supervisory deal team lead is defined as the "individual who has primary responsibility for supervising the strategic assessment of the deal, and who would not otherwise qualify as a director or officer;" and

- Regularly prepared business plans and reports provided to the company's CEO, and plans and reports provided to the board (whether prepared on a regular basis or not), prepared within one year of the filing date related to overlapping products or services.

- Parties are also required to submit all the documents included in the agreement(s) related to the proposed transaction such as exhibits, schedules, side letters, agreements not to compete or solicit, and other agreements negotiated in conjunction with the transaction.

- Buyers are required to disclose officers and directors with responsibilities for operations in overlap industries, including their positions in other entities, and certain limited partners with management rights and investment relationships between the buyer and the target.

- Buyers reporting overlap transactions or supply relationships with the target are required to report information about pending proposals and active contracts with the Department of Defense or the Intelligence Community valued at $100 million or more to help the Agencies identify transactions in which the merging parties are providing critical products or services to the U.S. government.

- Parties reporting overlap transactions or supply relationships are both required to disclose prior acquisitions over the last five years to reveal roll-up or serial acquisition strategies. Under Item 8 of the existing HSR form, only Buyers had to report such information for overlap transactions.

- Parties are required to disclose subsidies from certain foreign governments or entities that are strategic or economic threats to the United States to implement the Merger Modernization Act.5

- Parties are required to translate into English all foreign language documents submitted as part of the filing.

- The FTC also rolled out a new online portal for the submission of comments on proposed transactions that may be under review. "The Commission welcomes information on specific transactions and how they may affect competition." 6

Below is a table published by the FTC summarizing the new information requirements by filer and transaction type.7

The scope of the Final Rule will have a significant impact on deal timing. Parties to reportable transactions should consider the preparation of the HSR Act filing much earlier in the process and build in longer or more flexible filing deadlines in transaction agreements.

Dealmakers should involve antitrust counsel early in the process to review ordinary course documents related to competition and transaction-specific documents, which must be included in the HSR Act filing.

Anticipating that the Final Rule will become effective in January, dealmakers should take steps today to prepare in coordination with antitrust counsel.

For an in-depth discussion of the Final Rule, please join us for "The New HSR Rules Are Here: What Dealmakers Need to Know" webinar on Tuesday, October 22, 2024. To register, click here.

Footnotes

1. Premerger Notification: Reporting and Waiting Period Requirements: Final Rule (ftc.gov) (Final Rule); and FTC Finalizes Changes to Premerger Notification Form | Federal Trade Commission

3. The Final Rule defines Select 801.30 Transactions as “[a] transaction to which § 801.30 applies and where (1) the acquisition would not confer control, (2) there is no agreement (or contemplated agreement) between any entity within the acquiring person and any entity within the acquired person governing any aspect of the transaction, and (3) the acquiring person does not have, and will not obtain, the right to serve as, appoint, veto, or approve board members, or members of any similar body, of any entity within the acquired person or the general partner or management company of any entity within the acquired person. Executive compensation transactions also qualify as select 801.30 transactions.” 16 C.F.R. Part 803, Appendix B at 1.

4. Early termination was last suspended by the Agencies, on a “temporary basis: in February 2021. FTC, DOJ Temporarily Suspend Discretionary Practice of Early Termination | Federal Trade Commission

5. See Merger Filing Fee Modernization Act of 2022, 15 U.S.C. 18b (requiring the Commission to promulgate a rule requiring HSR filings to include information on subsidies received from certain foreign governments or entities that are identified as foreign entities of concern)

6. Portal accessible at: Comment on a Proposed Merger | Federal Trade Commission (ftc.gov)

7. See Final Rule at page 156.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.