- within Government, Public Sector, Intellectual Property and Antitrust/Competition Law topic(s)

- with readers working within the Technology industries

REPORT QUALIFICATIONS/ASSUMPTIONS & LIMITING CONDITIONS

This report sets forth the information required by the terms of NERA's engagement by Energy UK and is prepared in the form expressly required thereby. This report is intended to be read and used as a whole and not in parts. Separation or alteration of any section or page from the main body of this report is expressly forbidden and invalidates this report.

This report is not intended for general circulation or publication, nor is it to be used, reproduced, quoted or distributed for any purpose other than those that may be set forth herein without the prior written permission of NERA. Neither all nor any part of the contents of this report, any opinions expressed herein, or the firm with which this report is connected, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other public means of communications, without the prior written consent of NERA.

Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified. No warranty is given as to the accuracy of such information. Public information and industry and statistical data, including without limitation publications by Ofgem and the Office for National Statistics are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the information without further verification.

The findings contained in this report may contain predictions based on current data and historical trends. Any such predictions are subject to inherent risks and uncertainties. In particular, actual results could be impacted by future events which cannot be predicted or controlled, including, without limitation, changes in business strategies, the development of future products and services, changes in market and industry conditions, the outcome of contingencies, changes in management, changes in law or regulations. NERA accepts no responsibility for actual results or future events.

The opinions expressed in this report are valid only for the purpose stated herein and as of the date of this report. No obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof. All decisions in connection with the implementation or use of advice or recommendations contained in this report are the sole responsibility of Energy UK. This report does not represent investment advice nor does it provide an opinion regarding the fairness of any transaction to any and all parties.

This report is for the exclusive use of Energy UK. There are no third party beneficiaries with respect to this report, and NERA does not accept any liability to any third party. In particular, NERA shall not have any liability to any third party in respect of the contents of this report or any actions taken or decisions made as a consequence of the results, advice or recommendations set forth herein.

EXECUTIVE SUMMARY

Overview and Results

The Energy Company Obligation (ECO) is an obligation placed on the six largest energy suppliers to install energy efficiency measures in the homes of domestic customers. The Department of Energy and Climate Change (DECC) estimated that the ECO would cost energy suppliers £1,300 million per year (about £53 per customer per annum). Energy UK commissioned NERA to review DECC's modelling approach and to provide an alternative estimate of the programme cost.

We built a simplified model which replicates DECC's analysis and tests the impact of DECC's assumptions on its cost estimate. Our analysis suggests that correcting unreliable assumptions in DECC's modelling would raise the estimated cost of the programme to around £1,700 million per annum (ca. £69 per customer per annum).

In addition, there may be a problem with DECC's reliance on a "stated preference" study, a form of customer research which is known to suffer from a bias in the case of environmental programmes (i.e. the "warm glow" of appearing to favour good works leads people to state that they will pay more for environmental programmes than they will pay in reality). DECC has not published the study, so it is difficult to quantify precisely the impact of any bias inherent in the answers. A simple and transparent sensitivity is to assume that respondents might have ignored the "hassle costs" that an ECO project would impose on them. Adjusting DECC's model of customer preferences by a comparable amount raises the cost of the programme further still, to around £2,350 million per annum (ca. £94 per customer per annum), but the final cost could be much higher.

This analysis does not give upper and lower bounds for the costs of the ECO. Other risk factors and untested assumptions may cause the final cost of ECO to exceed our estimates.

Programme Components

The ECO consists of an obligation to surrender a given number of "ECO Points" between January 2013 and March 2015. Energy suppliers can earn ECO points from four (overlapping) schemes:

- Affordable Warmth (AW): an obligation to help customers save £4.2 billion on their "notional" energy bills using the full range of energy efficiency measures;

- Carbon Savings Obligation (CSO): an obligation to reduce lifetime carbon emissions from private households by 20.9 MtCO2 (20.9 million tonnes of carbon dioxide) using a restricted range of relatively expensive insulation measures (solid wall insulation and "hard to treat" cavity wall insulation);

- Carbon Savings Communities (CSC): an obligation to reduce emissions by 6.8 MtCO2 by insulating any housing within defined low income areas, for which suppliers may use a wide range of insulation measures; and

- Rural Safeguard (RS): an obligation on each supplier to meet at least 15% of its CSC obligation by serving rural households.

DECC assumes that energy companies pay the full cost of insulation installed under the Affordable Warmth scheme. Under the CSO, CSC and RS, domestic customers pay some of the costs of their insulation. However, they are eligible for the "Green Deal", whereby they take out a loan which they repay through a surcharge on their electricity bills. Their contribution is capped at a level intended to ensure they save money overall. Energy suppliers pay the rest.

DECC Modelling of the Costs of ECO

DECC estimated the costs of Affordable Warmth using an "Affordable Warmth Model" and the costs of the CSO, CSC and RS carbon targets using a "Green Deal Household Model" (GDH Model). The GDH Model estimates the residual costs of the CSO, CSC and RS faced by suppliers after deducting the customer contribution. DECC assumes that energy suppliers will select opportunities to invest in order of their cost effectiveness. However, the results of both models depend crucially on assumptions about the energy suppliers' costs of finding opportunities to invest, the cost of installing the insulation and consumers' reactions.

DECC has not published its analysis in full, or the models used to estimate the cost of ECO. Where DECC published its assumptions, we have compared them with information available in the public domain and obtained from the energy suppliers. Our review uncovered evidence that DECC:

- under-estimated the costs of finding customers eligible for support under the programme;

- over-estimated the frequency with which customers consider whether or not to install insulation; and

- over-estimated opportunities for bundling insulation measures together (in particular, it may be harder to find households without loft insulation).

As a result of these three biases, DECC's analysis under-estimates the cost of installing insulation, over-estimates the amount that customers will be willing to pay for it and, therefore, underestimates the total cost to energy suppliers of subsidising the programme. Other assumptions in DECC's analysis are subject to a margin of error in either direction.

DECC's estimate of the costs of the carbon targets (CSO, CSC and RS) uses a measure of customers' "willingness to pay" for insulation in their homes derived from a stated preference study. Stated preference studies are known to over-value environmentally friendly policies, as respondents tend to be favourable towards them (a phenomenon known as the "warm glow" bias). DECC's own consultants, Element Energy, explained that the output of the stated preference study had not been calibrated to historical data and that they "strongly recommend" the collection of further data on uptake of the programme in the real world. DECC has chosen instead to proceed on the basis of the results from this study.

Results After Correction of DECC's Inputs

DECC has not published either the stated preference study or the models underlying its cost estimate for the ECO programme. We therefore built our own simplified version of DECC's GDH Model and tested the impact of changing DECC's assumptions on the cost of the CSO – by far the largest component of the ECO programme, accounting for about 60% of the total cost of the programme according to DECC.

We first examined the effect of assuming that the technical potential for insulation is systematically less than DECC assumes. Given the information in DECC's publications, we captured a reduction in technical potential as a tightening of the definition of "hard to treat" cavity walls. This change substantially raised the cost of the programme. Other errors in modelling technical potential and participation by household type (such as over-estimating the willingness of large home owners to participate, and hence the average CO2 reduction per household) would have a similar effect.

We studied in detail the effect on the cost of the CSO of adopting more defensible assumptions (i.e. the historical figures) on customers' "decision making frequency, the "search" costs of identifying eligible customers and the opportunity to install a "bundle" of insulation measures at one property. The other obligations (AW, CSC and RS) appear to be less responsive overall to changes in DECC's main assumptions. In the absence of more detailed information, we assumed that the cost of these programmes was half as responsive to such changes as the cost of the CSO. We found that correcting these assumptions in DECC's modelling would cause the cost of the ECO programme to rise to £1,700 million per annum (ca. £69 per customer per annum).

We also conducted a simple sensitivity to remove a potential bias in the stated preference survey, by assuming that willingness to pay was 10% lower. This is a simplistic adjustment, but it happens to correspond closely to assuming that respondents to the survey ignored the "hassle costs" they will face during the process of installation. If DECC's estimate of customers' willingness to pay for insulation ignores the cost of the "hassle" that customers face before and during installation of insulation measures, energy suppliers will have to give customers a bigger subsidy by paying more for an ECO point. Our adjustment of willingness to pay corrects approximately for the potential bias of omitting "hassle costs". This one change raises the cost of the programme further, to £2,350 million per annum (ca. £94 per customer per annum), but the final cost could be higher still.

A reduction in technical potential (as discussed above) would raise this cost. Risks surrounding energy prices, interest rates and other untested assumptions mean that the true cost of the ECO programme could be even higher (although these risks are symmetric). A big unknown is the amount that customers will contribute towards the cost of each project. If in practice customers do not offer to finance the predicted share of project costs (directly or through the new Green Deal), the cost of the ECO programme borne by suppliers and included in customer tariffs will rise substantially.

An alternative yardstick for the cost of the ECO programme is the cost per tonne of reducing CO2 emissions. The European Union Emission Trading Scheme (EU ETS) offers the chance to purchase and sequester allowances to emit CO2, a kind of "virtual Carbon Capture and Storage" (vCCS) which also reduces emissions of CO2. The current price of these allowances is around £6.50/tCO2.1 On this basis, DECC's own estimated cost of the CSO is, at £77/tCO2, over 12 times as expensive as vCCS. Our estimate of the cost of the CSO programme would be even higher – between 15 and 25 times the cost of vCCS. Similarly, the cost of the AW, CSC and RS schemes would be around 10 times the cost of vCCS.

At a net cost to consumers of £94 per annum, therefore, we conclude that the ECO programme would be an expensive way to reduce emissions of carbon dioxide.

1. INTRODUCTION

The Energy Company Obligation (ECO) is a new obligation on the six largest energy suppliers serving domestic customers in Great Britain. Under the scheme, the energy suppliers will be required to register sufficient energy efficiency and insulation projects to meet a carbon and bill-reductions target. The Department of Energy and Climate Change's (DECC's) Final Impact Assessment includes a central estimate for the cost of the ECO to energy suppliers of £1.3bn per annum between Jan-2013 and March-2015.2 DECC ran sensitivities illustrating the possibility that components of the ECO programme could cost 1.5 times as much per ECO point as its central estimate. However, DECC failed to draw the implications for the cost of the ECO programme as a whole.3

Energy UK asked NERA to scrutinise DECC's cost assessment and provide, if appropriate, an alternative assessment. Our analysis draws on research from data in the public domain, conversations with the energy suppliers and from a confidential and commercially sensitive survey that the suppliers completed to provide detailed alternative assumptions to calculate the cost of ECO. DECC has not published the full details of its model, so it was not possible to calculate the costs of the ECO using DECC's exact framework. A full independent modelling exercise from the ground up is outside the scope of this report. We provide an independent assessment of the costs of ECO using a simplified model based on what we know about DECC's own analysis.

This report proceeds as follows:

- Section 2 provides background on the Energy Company Obligation;

- Section 3 sets out how energy companies will procure ECO points in practice;

- Section 4 scrutinises DECC's modelling assumptions and provides estimates of the costs of the components of the process of obtaining ECO points;

- Section 5 analyses the impact on the costs of the ECO of changing DECC's modelling assumptions using alternative estimates; and

- Section 6 concludes.

Our analysis suggests that correcting unreliable assumptions in DECC's modelling would raise the estimated cost of the programme to around £1,700 million per annum (ca. £70 per customer per annum).

In addition, there may be a problem with DECC's reliance on a "stated preference" study, which are known to suffer from a bias in the case of environmental programmes (i.e. the "warm glow" of appearing to favour good works). DECC has not published the study, so it is difficult to quantify precisely the impact of any bias inherent in the answers. A simple and transparent sensitivity is to assume that respondents might have ignored the "hassle costs" that an ECO project would impose on them. Adjusting DECC's model of customer preferences by a comparable amount raises the cost of the programme further still, to around £2,350 million per annum (ca. £95 per customer per annum).

Even this analysis does not give upper and lower bounds for the costs of the ECO. Other risk factors and untested assumptions may cause the final cost of ECO to exceed our estimates.

2. BACKGROUND

The Green Deal and Energy Company Obligation (ECO) are twin policies which seek to promote energy efficiency investments in Great Britain. The policies allow customers to pay for energy efficiency measures through savings in their energy bills, and to obtain subsidies to finance the installation of some these projects. The two policies are interdependent: the success of the Green Deal in financing customers' installation of energy efficient measures is a primary driver of the costs energy suppliers will face in meeting their targets under the ECO. If the Green Deal is successful in encouraging customers to finance energy efficiency investments through their bill savings, then the resulting top-up that energy suppliers must provide will be small. Conversely, if the Green Deal does not significantly increase investment in different methods of insulation, energy suppliers will face large costs to make up this shortfall. Any costs the suppliers incur will have to be recovered through an increase in energy bills.

2.1. Introduction to the Green Deal

The Green Deal provides domestic and non-domestic customers with the option of financing insulation projects through a surcharge on their own energy bills.

For each property, the process of obtaining a Green Deal starts with an assessment of the potential for improving its insulation, and the customer's estimated energy savings from installing superior insulation. In the domestic sector, energy savings will be estimated based in part on an "occupancy assessment" that informs customers whether their use is likely to be above or below the typical household.4 Following an assessment, customers may ask multiple insulation providers to offer them a "Green Deal Plan". This plan sets out a quotation for installation, as well as the terms of the repayment, which takes the form of a charge added to the customer's monthly energy bill. Charges levied under the Green Deal Plan must obey the "Golden Rule", which requires that:5

- The life of the repayment must be less than the expected life of the new installation;

- The charge in the first year must be less than the expected reduction in the bill due to the increase in energy efficiency; and

- The charge may rise no more than 2% per annum in nominal terms thereafter. Green Deal financing is available for a broad range of measures, including all forms of loft insulation, cavity wall insulation (CWI), and solid wall insulation (SWI), without restriction.

2.2. Introduction to the ECO

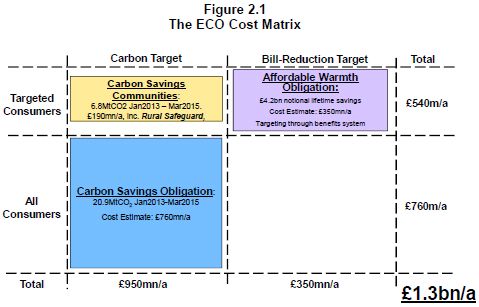

The Energy Company Obligation (ECO) is an obligation placed on energy suppliers requiring them to fund additional insulation projects, which either cannot or will not be funded by domestic customers through the Green Deal alone. DECC proposes to divide the obligation between energy suppliers "on the basis of their share of the gas and electricity supplied", with half the obligation allocated on the basis of electricity sales and half on the basis of gas sales.6 The ECO consists of four strands, which we set out below.

- Affordable Warmth: an obligation to help households from low income groups, living in privately rented accommodation and identified through the benefits system. Energy suppliers face an obligation to save £4.2 billion on their customers' "notional" energy bills by March 2015 and can satisfy the obligation using the full range of energy efficiency measures.7

- Carbon Savings Obligation (CSO): The obligation is to reduce lifetime carbon emissions from private households by 20.9 MtCO2 (megatonnes of carbon dioxide) between January 2013 and March 2015.8 Only certain measures are eligible for recognition under the CSO including SWI and "hard-to-treat CWI", as well as any thermal insulation measures packaged with SWI or hard-to-treat CWI.9

- Carbon Savings Communities (CSC): Energy suppliers can only satisfy the CSC by delivering insulation within defined low income areas (but not only to low income households within those areas). CSC allows energy suppliers to use the full range of insulation measures including all loft insulation and CWI. The CSC represents 20% of the total Carbon Savings Target (= CSO + CSC) and requires suppliers to reduce emissions by 6.8 MtCO2 between January 2013 and March 2015;10 and

- Rural Safeguard (RS): The Rural Safeguard is a "sub-obligation" nested within the CSC. The Rural Safeguard requires suppliers to meet at least 15% of their CSC obligation by serving rural households that are either (1) in receipt of benefits making them eligible for the Affordable Warmth subsidy or (2) in low income areas or in areas adjacent to low income areas.11

Figure 2.1 provides an overview of these obligations and also the estimated costs of each programme, as stated by DECC.

A

A

2.3. DECC's Estimated Costs

DECC estimates that the ECO will cost around £1.3bn per annum. To calculate this figure, DECC first assembles a list of the technical characteristics of the insulation market in Great Britain, including:

- the number of different types of insulation projects in Great Britain;

- generic costs of these projects; and

- the expected carbon savings/energy savings from these projects.

DECC then uses two models to estimate the costs of delivery: (1) the Affordable Warmth Model for AW and (2) the Green Deal Household Model for the CSO and CSC (which includes the RS).

In addition to the costs of delivering each measure, DECC estimates the administration costs for the programme as a whole. Below, we explain how DECC estimated the costs of each programme.

2.3.1. Affordable Warmth Model

The Affordable Warmth Model simulates the delivery of the wide variety of energy efficiency measures eligible under the AW scheme (including improved heating). The model assesses the technical potential for installing a range of major insulation and efficiency measures. It then estimates how much each measure would cost and ranks projects in order of cost effectiveness for delivering a reduction in CO2 emissions. Allowing for the insulation installed under the Green Deal and Carbon Saving Targets, AW then picks the most cost effective combination of measures which achieve the target reduction in "notional" customer bills.12 The model allows for multiple measures to be installed in a single property, even when some of those measures would not be individually cost effective, if the measures are cost effective when modelled as a package.13 According to DECC, the total cost of the AW programme will be around £350 million per annum.14 This programme has no target CO2 reduction attached to it.

2.3.2. Carbon Saving Obligation

DECC uses the Green Deal Household Model to estimate the cost of the CSO. The Green Deal Household Model models customer behaviour and willingness to invest in insulation. In order to model household behaviour, we understand that DECC has undertaken a survey of customers' willingness to pay for insulation projects. DECC has not published the survey in full, which makes it difficult to describe its method precisely. Instead DECC provides only a brief description of its methodology.

DECC explains that the survey offered customers a number of choices between insulation packages and financing options at random. From the customers' responses, DECC defines a probability that any customer with a given set of characteristics would be willing to install insulation for an expected energy bill saving and at a given investment cost. We note that DECC's brief description is insufficient to provide a detailed understanding of its method and DECC's methodology would be clearer if it published the documentation surrounding the survey.

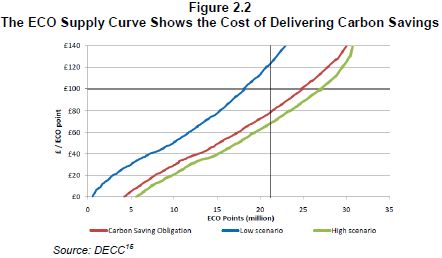

DECC combines the survey responses with information about the availability of insulation projects meeting the CSO's eligibility criteria with assumptions about energy prices, energy bills and the interest rates faced by customers under the Green Deal. This allows DECC to define an "ECO Point Supply Curve". The ECO Point Supply Curve represents the minimum subsidy that energy suppliers would have to pay in order to induce customers to install solid wall insulation and hard-to-treat cavity wall insulation for any given level of carbon emissions reduction. DECC defines three ECO point supply curves based on different assumptions about energy prices and interest rates (see Figure 2.2).

DECC is not clear about precisely how it forms its cases , which are defined as "low", "central" and "high", but also referred to as "Low, Central and High take-up".16 For example, in Annex H of the Impact Assessment, DECC labels the case with a high interest rate and a high energy price as corresponding to the high case. In practice, low interest rates and high energy prices would correspond to the "highest take-up" of the Green Deal (by making insulation measures more attractive to customers). DECC's scenarios do not therefore seem to span the entire range of possible outcomes, but to allow for some effects to offset one another.

DECC estimates that the expected cost of the CSO, in pounds per ECO point (i.e. per tonne of carbon dioxide emissions reduction or £/tCO2), is as follows:

- Over £120/tCO2 in its "low" case (saving less 5 MtCO2);

- Almost £80/tCO2 in its "central" case (saving about 5 MtCO2);

- Around £65/tCO2 in its "high" case (saving slightly more than 5 MtCO2).

These results indicate that the "low/central/high" designation relates to likely rates of take-up by customers, and not the level of all the associated variables (i.e. low energy prices may be associated with high interest rates in a "low take-up case").

The cost per ECO point is considerably higher than the cost of reducing CO2 emissions indicated by the EU Emissions Trading Scheme (ETS) over the same period. Prices in the ETS have been below £10/tCO2 for some time.

2.3.3. Carbon Saving Communities

DECC also uses the Green Deal Household Model to estimate the cost of the CSC, based on a similar but separate process of modelling customer behaviour and willingness to invest in insulation. DECC's analysis suggests that the cost of meeting the CSC obligation will be lower per ECO point than for the Carbon Savings Obligation for households in general, at around £60 per ECO point.17

2.4. DECC Estimates a Cost to Suppliers of £1.3bn

DECC admits that there is uncertainty around its central estimates and that these costs are hard to quantify:

"The ECO obligations are quantity targets, requiring a given level of savings to be achieved. Until the ECO becomes operational there is uncertainty over what the market clearing price will be. The price will be determined by a range of factors including fossil fuel prices, technology costs and consumer preferences."18

DECC models costs for its low, central and high cases.

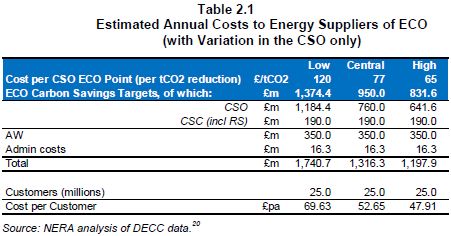

In its central case, DECC estimates that delivering the ECO measures will cost around £1.3bn pounds per annum, including the costs of the Carbon Savings Targets and Affordable Warmth. DECC also estimates that administration costs born by suppliers and green deal providers for the scheme will run to a further £16.3 million per annum and costs to the government will be £22 million.19

The total costs borne by suppliers in DECC's central case amount to around £52.50 per annum per customer (spread over approximately 25 million customers). DECC does not provide estimates for the costs of the ECO programme as a whole under its high and low case assumptions. However, costs per tCO2 under its high and low case assumptions are available for the CSO (see Figure 2.2, above), which provides the basis for some elementary sensitivity tests.

Table 2.1 shows total cost of the CSO rescaled to take account of the lower costs per tCO2 in DECC's "high" case and the higher costs per tCO2 in DECC's "low" case. This sensitivity causes total costs to vary over the range £1,200-1,700 million for the ECO as a whole, with the cost to energy suppliers ranging from about £48 per annum per customer in the "high (take-up)" case to about £70 per annum per customer in the "low (take-up)" case.

In principle, a complete assessment of total costs of the ECO in DECC's "high" and "low" cases would need revised cost estimates for the other components of the ECO. The Impact Assessment does not show the impact of changing these assumptions on the total cost of the CSC or AW programme.

DECC's "high" and "low" case assumptions would have a different impact on the costs of AW and CSC than on the costs of the CSO.

DECC assumes that energy companies will fund Affordable Warmth projects without the consumer part-financing the investment via the Green Deal.21 Therefore changing the interest rate assumption does not change the cost of the AW. However, DECC measures compliance with the AW target using generic assumptions about the energy-saving benefits of projects and multiplying them by its assumption of the variable energy price.22 Lower energy prices would mean lower reductions in the notional bill and therefore require energy suppliers to undertake more energy efficiency projects to meet the AW target, at a higher cost to energy companies and ultimately consumers.

The CSC is an obligation targeting carbon reductions (like the CSO) and would be similarly affected by DECC's "high" and "low" case assumptions. However, the CSO encompasses a broader range of technologies and a narrower customer group, which may, in principle be more or less susceptible to changes in energy prices and interest rates.

The interactions between energy prices and the AW and interest rates and energy prices and the CSC are complicated. Defining sensitivities corresponding to DECC's "high" and "low" cases for the AW and CSC would require detailed modelling. However, we can define "what-if" scenarios using the illustrative assumption that the combined cost of the AW and CSC is half as sensitive to DECC's "high" and "low" case assumptions as the CSO. Under this assumption, the total cost of ECO would range between £1,140 million and £1,880 million in DECC's "high" and "low" cases (£45.50 to £75 per customer per annum).23

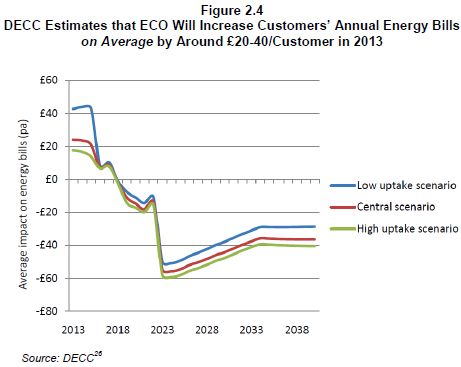

2.5. Customer Bills Rise By £20-£40 Under DECC's Assumptions

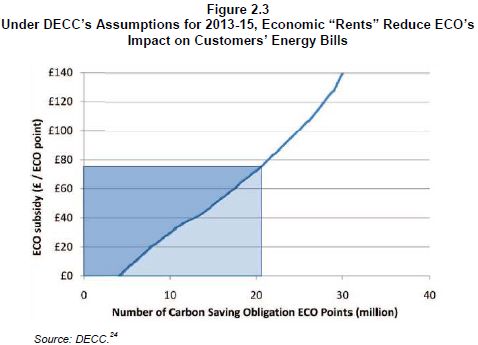

DECC's analysis assumes that energy suppliers will pass all of the costs in Table 2.1 through to customer bills. Not all of these costs of the ECO programme represent an additional cost to customers. Some of the costs of the programme are payments from energy suppliers to energy customers that reflect "economic rents", i.e. the gap between the market price for something in scarce supply and the cost of producing it. In this case, there is a scarce supply of low cost energy efficiency measures and DECC assumes that customers with low cost opportunities will capture the benefit of these rents.

Figure 2.3 illustrates the cost to suppliers of meeting the CSO. The blue line is the supply curve for ECO points earned under the Carbon Saving Obligation. It represents the minimum subsidy required to save each additional tonne of CO2 emissions under ECO, and hence the cost of obtaining an ECO point. These market-level payments of up to £77 per tCO2 would be made either as a reduction in energy bills under the Green Deal financing arrangements or through direct payments to the customer (known in economics as "side payments"). The blue shaded box represents the total cost to suppliers, who will pay the market price of £77 for each ECO point they purchase (either directly to customers by installing insulation or indirectly through installers). The darker area above the cost curve is the market-level payment from suppliers to consumers who can take advantage of relatively low cost insulation projects, and who would in principle be willing to accept a subsidy of less than £77 per tCO2 for their own insulation project to fit insulation.

DECC presents the results of its analysis assuming that energy suppliers make full use of the Green Deal and therefore reduce energy bills to cover these "side payments" (or, equivalently, that the results for average energy bills are shown net of any side payments). After taking account of these side payments and the reduction in energy bills due to energy efficiency, DECC concludes that the final impact on bills would range from just under £20 per annum per customer in 2013-2015 in DECC's "high case" to just over £40 per annum per customer in 2013-2015 in DECC's "low case" (see Figure 2.4).

This change in the average energy bill masks very different results for different types of customers.

Customers who benefit from subsidies under ECO will see their energy bills fall both due to the Green Deal or equivalent side payments and due to reduced consumption after energy efficiency improvements take effect.25

Customers who do not receive subsidies under ECO will see their bills rise by the full cost of the ECO to the energy suppliers. Under DECC's assumptions the annual energy bills of customers who do not receive any ECO subsidy will rise by £48 to £70, as set out in Figure 2.4.

2.6. Conclusion

The ECO programme is split between sub-programmes aimed at reducing "notional" energy bills by a certain amount (AW: £4.2bn from January 2013 to March 2015) and sub-programmes aimed at reducing emissions of CO2 (CSO: 20.9 MtCO2; CSC: 6.8 MtCO2; RS: contained within CSC). DECC estimates the total costs of the ECO programmes as £1.3bn per annum. This cost represents DECC's estimate of the amount energy suppliers will have to recover from customers in general.

3. THE PROCESS OF COLLECTING ECO POINTS

Energy suppliers and ultimately customers will pay for the measures installed under the Energy Company Obligation. Green Deal Providers (GDPs) and insulation installers will actually deliver the measures required under the ECO. Green Deal Providers are organisations that manage the customer relationship throughout the process of acquiring insulation under the Green Deal/ECO programmes. Insulation installers are organisations that fit insulation in customers' homes. In principle, GDPs and insulation installers could be vertically-integrated units within the six large supply businesses. Alternatively, GDPs or insulation installers could be independent businesses or part of larger networks distinct from the energy suppliers.

The process of collecting ECO points for eligible measures will involve suppliers, GDPs and insulation installers:

- acquiring a potential customer;

- providing the customer with a quotation, arranging any Green Deal finance and any relevant subsidy; and

- arranging for the installation of the measure in the customer's house or flat.

In this chapter, we set out the process that suppliers, GDPs and insulation installers will have to undertake to deliver the ECO. The roles of the supplier, GDP and installer may be slightly different across the different obligations, across suppliers or GDPs, and may evolve as the ECO is rolled out.

Throughout, we use the term "GDP" to describe an organisation that is managing the customer relationship over the course of acquiring, quoting for and installing an insulation project. In practice, the organisation may not be providing Green Deal finance (for example, DECC assumes Affordable Warmth customers do not use Green Deal finance). Nonetheless the role of a GDP as a manager of the customer relationship would still be necessary. For ease of exposition, we explain the process of acquiring ECO points in detail including the steps necessary for Green Deal Finance. Only small adjustments to the description (and the costs) are necessary for the case where customers do not make use of Green Deal Finance (and we highlight those adjustments in the text below).

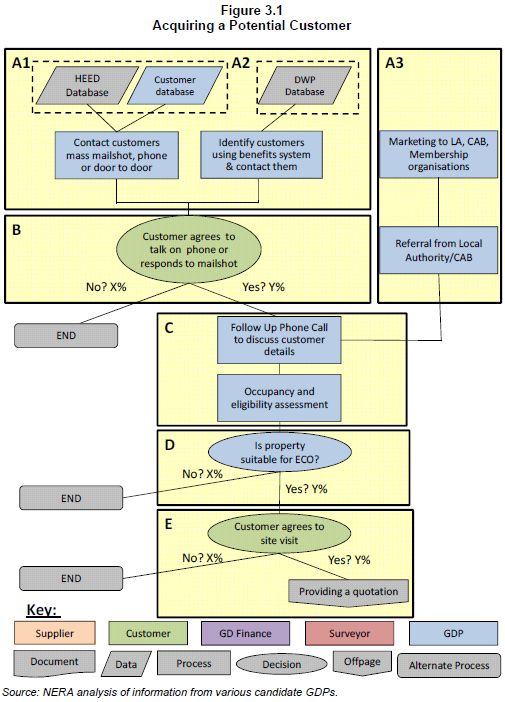

3.1. Acquiring a Potential Customer

Box A of Figure 3.1illustrates the process of making initial contact with customers. GDPs have to begin by identifying likely (or, for some programmes, eligible) customers. Data on potential customers will be available from several data sources. For the CSO, the CSC and the RS, GDPs or suppliers will be making use of the processes in Box A1. The Homes Energy Efficiency Database (HEED) is an online source for data on the housing stock, heating systems and installed installation.27 This, along with a GDP's own databases on customers, will be a method of identifying customers that can then be targeted by phone, mail, or door to door marketing. To qualify for ECO measures under the Affordable Warmth scheme, customers must be in receipt of certain means-tested benefits. To identify this group, a GDP may be able to make use of data from the Department of Work and Pensions (DWP) as illustrated in Box A2.28 An alternative route to market could involve building links with organisations or local government. For example, the GDPs or energy supply companies may market to the Citizens Advice Bureau (CAB), Local Authorities (LA) and or membership organisations such as the National Trust, as illustrated in Box A3.

For the process to proceed to the next stage, a potential customer must agree to talk on the phone or otherwise respond to the initial contact they have received. At this stage, there will be an inevitable rate of attenuation from customers who are not interested in further contact with a GDP. This process is illustrated in Box B of Figure 3.1.

Those customers who do respond by some means to the initial contact from a GDP can then be followed up by phone to discuss their personal circumstances, their need for ECO measures, and their eligibility. This process is illustrated in Box C of Figure 3.1.

At this stage, the GDP should be able to determine that a proportion of the customers that it has followed up are not eligible, typically because their property is not suitable for fitting an ECO measure. (See Box D in Figure 3.1) Moreover, even if customers are found to be eligible and living in a dwelling with the technical potential for an energy efficiency installation, there is a further stage of attenuation as customers may not agree to the site visit which is a precursor to providing a quotation. Only if to the customer agrees to such a visit will the GDP be able to progress to the next stage, as illustrated in Box E of Figure 3.1.

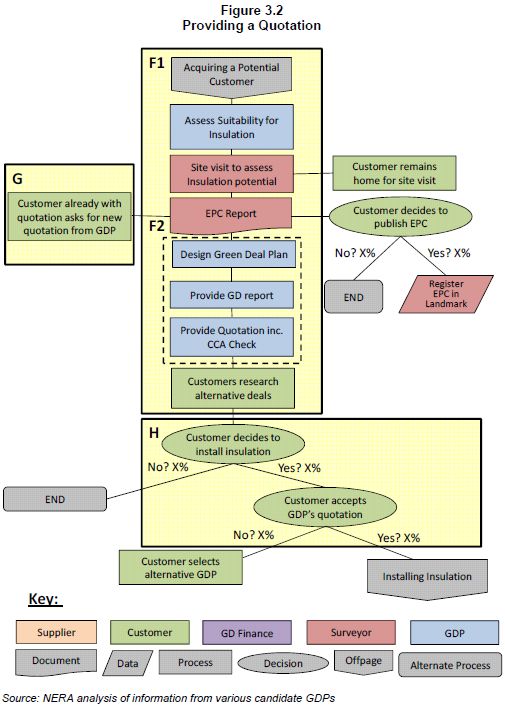

3.2. Providing a Quotation

Having acquired an eligible customer that is willing to agree to a visit to their dwelling, a GDP must then assess the suitability of the property for ECO measures. This process is illustrated in Box F of Figure 3.2. The site-visit will typically be carried out by a surveyor, or "Green Deal Advisor", which will require the customer to remain at home for the duration of the visit. The document produced by the surveyor or advisor, an Environmental Performance Certificate (EPC), may then be registered with Landmark, a company that maintains a register of EPCs on behalf of the government.29 A certain proportion of customers will not agree to have their EPC published in this manner.

The process in Box F will differ slightly depending upon whether the customer requires Green Deal Finance. If a customer is self-financing or the installer or energy supplier is financing the project without using Green Deal finance, the energy supplier may complete the steps in Box F1 and skip the steps in Box F2. If the customer wishes to use Green Deal finance, the GDP would have to undertake all of the steps in Box F1 and F2.

If the customer wishes to use Green Deal Finance, the GDP must design a Green Deal Plan as part of providing a quotation. The Green Deal Plan will ensure that the project is financeable using Green Deal Finance. This will involve identifying the subsidy (if any) required, accounting for costs of financing through the Green Deal, and ensuring that the "Golden Rule" – that bill savings in the first year must exceed repayments, and rise by no more than 2% p.a. subsequently – is followed. This will allow the GDP to provide a Green Deal report and quotation, including a credit check under the Consumer Credit Act (CCA).

As Box G of Figure 3.2 illustrates, some customers will already have received a quotation from another GDP and may seek a new quotation. These customers represent additional sources of insulation opportunities for other GDPs.

Following the provision of a quotation, customers will probably compare their quotation to other deals available. The customer may then decide to install an ECO measure, but only a certain proportion of these customers will do so by accepting the quotation provided by the GDP. The remaining customers will seek an alternative provider. Therefore, only after these further stages of deliberation and possible rejection by the customer will an eligible measure be installed, as illustrated in Box H of Figure 3.2.

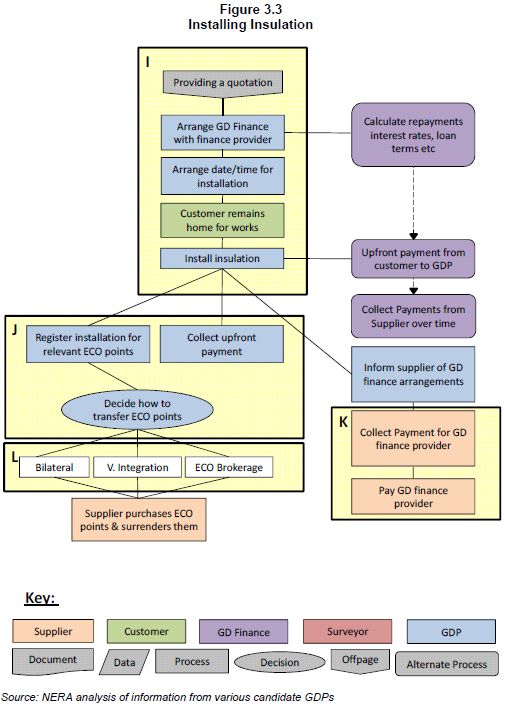

3.3. Installing Insulation

Having provided a quotation that was acceptable to the customer, a GDP will now have to arrange Green Deal finance with a suitable provider for the project. This will involve the calculation of the repayment schedule, loan duration, and interest rates applicable. The GDP will then have to arrange a date and time for the installation which, depending on the complexity of the installation to be carried out, will require considerable logistical effort by both parties. In particular, for complex measures such as wall insulation, the customer will have to remain at home for much of the duration of the works.

Installing the ECO measure may also necessitate an upfront payment from the customer to the GDP, the size of which will be determined by the quotation provided and the Green Deal finance available. Upon completing the installation, the GDP must register for the relevant ECO points. Energy suppliers require these points to fulfil their obligation, and the market for the transfer of these points encompasses three methods. Transfers can be arranged by bilateral agreement between the GDP and energy supplier, a transfer between vertically integrated entities (if the GDP is ultimately owned by an energy supplier), or by using an ECO brokerage as an intermediary. The result will be that an energy supplier purchases the ECO points and surrenders them to fulfil part of their obligation. This is illustrated in Box H of Figure 3.3.

If the customer is paying for the installation using Green Deal Finance, the energy supplier will also carry out the role of collecting Green Deal finance payments, as these are tied to the customer's electricity meter. This process is illustrated in Box I of Figure 3.3. Having been informed by the GDP of the finance arrangements the customer has entered into, the energy supplier will amend the unit rate on the meter to include the necessary repayments. The energy supplier remits the additional payments it collects from the increased unit rate on the meter to the Green Deal finance provider.

3.4. Summary

In summary, the process a supplier, GDP and/or insulation installer must undergo to successfully collect ECO points is complicated, involving search, transaction and administration costs at various stages to all parties involved.

Acquiring a customer involves the cost of searching for potential eligible households, making contact with them through physical or electronic means, and securing their agreement to talk further about the installation of eligible measures. Following up expressions of interest from potential customers, and determining whether their dwellings are indeed eligible for ECO measures, involves further overhead costs.

The surveys that must be undertaken in the house before beginning any works increase the costs of completing an installation. Customers may choose not to install an ECO measure with the GDP after obtaining an initial quotation, and GDPs may bear some or all of the costs of these unused quotations The proportion of unsuccessful assessments (which DECC estimates to be two out three) leads to increased transactions costs.30

Finally, there are costs both to the GDP and the customer of completing an installation. Customers must be willing to invest logistical effort and, where appropriate, take time off work to oversee an installation. GDPs must facilitate Green Deal finance for the project, inform the energy supplier of the appropriate repayments to collect, and finally participate in the ECO market to sell the points they have collected. There are also ongoing administration costs incurred by the Green Deal finance provider and the energy supplier in collecting repayments.

In Chapter 4 we discuss DECC's treatment of the cost items we have identified in the process of collecting ECO points.

To read this article/footnotes in full please click here.

Footnotes

1 Source: PointCarbon, http://www.pointcarbon.com/, downloaded 6 November 2012. Converted from €8.22/MtCO2 using an exchange rate of £0.80/€. Both the cost of an ECO point and the cost of vCCS represent marginal costs to society of reducing CO2 emissions. ECO points are even expensive relative to the £54/tCO2 value of non-traded CO2 emissions in 2013 stated by DECC in A brief guide to the carbon valuation methodology for UK policy appraisal, October 2011, p. 3.

2 DECC, Final Impact Assessment, 11 June 2012, page 84.

3 DECC ran a sensitivity to its modelling showing that the Carbon Savings Obligation component of the ECO would cost as much as 1.5 times its central estimate. DECC, Final Impact Assessment, 11 June 2012, page 59, Figure 22.

4 DECC, Final Impact Assessment, 11 June 2012, page 19.

5 DECC, Final Impact Assessment, 11 June 2012, page 20.

6 DECC, Final Impact Assessment, 11 June 2011, pages 7, 194.

7 DECC, Final Impact Assessment, 11 June 2012, page 4 and 21. We assume that this means energy bill savings will be estimated by a standard procedure for each type of investment in each type of property, rather than measured ex post.

8 DECC, Final Impact Assessment, 11 June 2012, page 4.

9 DECC, Final Impact Assessment, 11 June 2012, page 21.

10 DECC, Final Impact Assessment, 11 June 2012, page 22.

11 DECC, Final Impact Assessment, 11 June 2012, page 22.

12 DECC, Final Impact Assessment, 11 June 2012, page 40.

13 DECC, Final Impact Assessment, 11 June 2012, page 157.

14 DECC, Final Impact Assessment, 11 June 2012, page 84.

15 DECC, Final Impact Assessment, 11 June 2012, page 59, Figure 22.

16 DECC, Final Impact Assessment, 11 June 2012, page 155.

17 DECC, Final Impact Assessment, 11 June 2012, page 58, Figure 21.

18 DECC, Final Impact Assessment, 11 June 2012, page 84.

19 DECC, Final Impact Assessment, 11 June 2012, page 88.

20 DECC, Final Impact Assessment, 11 June 2012, page 84.

21 DECC, Final Impact Assessment, 11 June 2012, page 144.

22 In an earlier impact assessment as part of its consultation, DECC explains that Affordable Warmth target of a change in the energy bill is made by making generic technical assumptions about each energy efficiency measure: "These assumptions are used to estimate the energy reduced or increased by fuel type for each measure in kWh, using data from the Building Research Establishment and internal. Energy savings estimates from insulation measures are consistent with those in the GDHM. Changes in energy use are valued using the variable element of the relevant fuel price listed in the DECC IAG tool kit." DECC, Impact Assessment, 23 November 2011, page 191.

23 Variation in the cost of the CSO is -16% to +56%, assumed variation in the cost of the CSC and AW is -8% to +28% of the figures in Table 2.1.

24 DECC, Final Impact Assessment, 11 June 2012, page 84, Figure 33.

25 Improvements in energy efficiency may lead customers to lower their consumption of energy or to adopt higher standards of comfort, because heating is now cheaper. DECC's analysis allows for this "comfort taking" effect.

26 DECC, Final Impact Assessment, 11 June 2012, page 67, Figure 31.

28 We understand from conversations with the suppliers that discussions about whether DWP databases will be available are still ongoing.

29 See https://www.epcregister.com/home.html.

30 DECC, Final Impact Assessment, 11 June 2012, page 56.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.