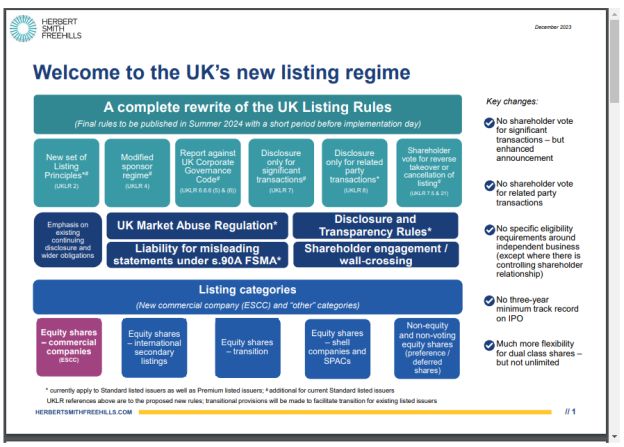

The Financial Conduct Authority (FCA) has today published in draft most of the new UK Listing Rules, to implement a radical restructuring of the UK listing regime (CP 23/31). While the genesis of the rule changes is the desire to attract more companies to list in London, they will of course have a significant impact on existing listed companies.

The FCA is implementing a new single segment, the new "equity shares (commercial companies)" category, to replace the current premium and standard segments, with just one set of continuing obligations for normal commercial companies. Proceeding with most of its trailed proposals from May this year, as part of the new UK listing regime:

- shareholder votes will no longer be required for significant/Class 1 transactions;

- shareholder votes will no longer be required for related party transactions;

- a modified sponsor regime will remain a cornerstone of investor and market protection;

- relationship agreements will remain mandatory with controlling shareholders; and

- there will be significant changes to the eligibility requirements for new prospective IPO candidates, moving to a disclosure-based rather than rules-based regime.

A short summary with further details is available below (and you can read more on the background here).

The changes will rely on greater disclosure and so will put more onus on investors to do their own due diligence.

CP 23/31 also includes the FCA's plans for investment funds, special purpose acquisition companies (SPACs) and overseas issuers with a secondary listing in London. Following this consultation paper, the FCA has said that it will publish a second paper containing draft rules for these "other shares categories", and the remaining rules that will impact all issuers (including the new listing principles), in Q1 2024.

The FCA says that it intends that all existing premium listed commercial companies will be automatically migrated to the new commercial companies category. Existing standard listed companies will be migrated to a new transition category – with the same continuing obligations as the current standard listing, and closed to new listings – where they can remain (with no present fixed end date) or make a streamlined application to join the new commercial companies category when they are ready to do so.

FTSE Russell, which maintains the FTSE indices, has said that it is reviewing the proposals and will provide an update during Q1 2024 on what they may mean for index inclusion going forwards.

The FCA has said that following this consultation (which closes on 16 February 2024 on the sponsor proposals, and 22 March 2024 for the rest) it expects to publish the final rules at the start of the second half of 2024 (with them coming into force two weeks later).

"In our view, it is positive to see the FCA sticking to its guns and pressing ahead with the full implementation of its bold package of listing reforms. The reforms will dramatically scale back those aspects of the UK's listing regime that were seen as uncompetitive as compared with other listing venues. The FCA has really done everything it realistically could to re-set the UK's listing framework, with disclosure now taking centre stage rather than shareholder votes or strict eligibility criteria."

"Investors will inevitably face more risks but encouraging vibrant public markets and improving returns for savers and pensioners is much more important than over-regulation resulting in the slow decline of the UK's equity markets. The next stage is for the Government to press ahead with its broader attempts to jump start the UK's investment culture, which is even more important than today's announcement."

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.