- in United Arab Emirates

On 4 August 2017, the text of the draft law introducing the new Luxembourg BEPS-compliant Intellectual Property (IP) regime was released. As from 1 January 2018, Luxembourg taxpayers will be able to benefit, under certain conditions, from an 80% exemption regime applicable to income related to patents and copyrighted software. In addition, IP assets which qualify for the 80% (corporate) income tax exemption will be fully exempt from net wealth tax.

The new regime will replace the former IP regime which had to be repealed as of 30 June 2016 since it was, as many other IP regimes, not in line with the so-called "modified nexus approach" defined in the OECD report on Action 5 of the BEPS Action plan and agreed upon at EU level.

Who will be able to benefit from the new regime? Which income from which IP assets will be covered and which conditions and limitations will apply? We provide answers to these questions based on the recently released draft law which may still evolve and change during the legislative process.

Who can benefit from the new IP regime?

As the former IP regime, the new regime will apply to all Luxembourg taxpayers. This means that the regime will be available to both individuals and companies. In addition, it will apply to Luxembourg permanent establishments of foreign companies located in a European Economic Area country (i.e. European Union, Iceland, Liechtenstein and Norway).

Which IP assets are covered by the new regime?

Luxembourg has defined the scope of the new IP regime in line with the conclusions reached in the BEPS Action 5 report. Accordingly, patents and other IP assets that are considered as functionally equivalent to patents if those IP assets are both legally protected and subject to similar approval and registration processes, where such processes are relevant, qualify for tax benefits under an IP regime.

In accordance with the draft law and in line with the conclusion reached in the BEPS Action 5 report, IP rights covered by the new Luxembourg regime are (i) patents defined broadly and (ii) copyrighted software.

These IP rights fall within the scope of the new regime to the extent that they are not marketing-related IP assets and were created, developed or enhanced after December 31st, 2007 (same limitation in time to the application of the regime as under the former regime) as part of research and development (R&D) activities:

- Patents defined broadly: inventions protected pursuant to domestic and international provisions in force, by a patent, a utility model, a supplementary protection certificate, a patent extension for pediatric medicines, a plant variety protection, orphan drug designations; and

- Copyrighted software: software protected by copyright according to the internal and international provisions in force.

Trademarks and domain names are expressly excluded as they fall into the category of marketing-related IP assets.

How to compute the IP income which can benefit from the new regime?

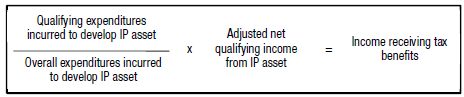

The modified nexus approach defined in the BEPS Action 5 report aims to ensure that IP regimes provide benefits to taxpayers that engage in R&D since the intention of IP regimes is to encourage R&D activity.

As a consequence, according to the nexus approach, a taxpayer is able to benefit from the IP regime to the extent that it can be demonstrated that the taxpayer incurred expenditures, such as R&D which gave rise to the IP income.

The nexus approach which determines what income may receive tax benefits is as follows:

This means that if a company has only one single IP asset and incurs all of the expenditures to develop that asset itself, the nexus approach will allow all of the income from that IP asset to qualify for tax benefits.

In order to compute the amount of income which comes within the ambit of the beneficial Luxembourg IP regime, it is necessary to determine:

- which expenditures are considered as "qualifying expenditures incurred to develop IP assets",

- which expenditures are considered as "overall expenditures incurred to develop IP assets" and

- how the net qualifying income from IP asset is computed.

Both the qualifying expenditures incurred to develop IP assets and the overall expenditures incurred to develop IP assets have to be taken into account at the time when they are incurred, no matter the treatment for accounting or tax purposes.

The draft law has defined these expenditures as follows:

Qualifying expenditures incurred to develop IP assets

Qualifying expenditures are expenditures which are necessary for undertaking R&D activities, directly linked to the creation, the development or the enhancement of a qualifying IP asset and incurred by the taxpayer for undertaking his own R&D activities.

Expenditures which are not directly linked to the qualifying IP assets are not taken into account.

It follows that the following expenditures are not considered as qualifying expenditures:

- Interest and other costs for financing the IP assets;

- Real estate costs;

- Acquisition costs; and

- Costs not directly related to a qualifying IP asset.

Expenditures for unrelated-party outsourcing performed through a related party are considered as qualifying expenditures, as long as no margin is realised by the related party on its activity linked to the qualifying IP asset.

Qualifying expenditures also include expenditures incurred by a foreign permanent establishment (PE), provided that the foreign PE:

- is located in a state which is party to the Agreement on the European Economic Area;

- is operational when the qualifying IP income is realised; and

- does not benefit from a similar IP regime in the country where it is situated.

Finally, when computing the amount of qualifying expenditures, taxpayers are allowed to apply a 30% "up-lift" to expenditures that are included in qualifying expenditures (up to the amount of the taxpayer's overall expenditures). Hence, the up-lift may increase the amount of IP income that benefits from the new IP regime.

Overall expenditures incurred to develop IP assets

The overall expenditures incurred to develop IP assets correspond to the sum of the qualifying expenditures as defined above (but without the 30% lift-up), the costs for the acquisition of the qualifying IP assets as well as the costs for related-party outsourcing.

Adjusted net qualifying income from IP assets

The net qualifying income from IP assets corresponds to the net positive difference between:

- The income realised on the qualifying IP assets (the "qualifying income"), i.e. positive income received for the right to use the qualifying IP right; income directly linked to the qualifying IP asset and incorporated in the sale price of a product or service; income realised on the disposal of such IP rights and the indemnity received in relation to the qualifying IP asset following a judicial proceeding or an arbitration procedure; and

- The overall expenditures and the expenditures incurred during the financial year which are indirectly related to a qualifying IP asset.

The draft law also provides for adjustment and offset of the net qualifying income. The purpose of such adjustment is to ensure that the net qualifying income incurred by a qualifying IP asset during a financial year only benefits from a partial IP exemption provided that the overall net qualifying income exceeds the operating expenses (i.e. direct and indirect expenses in connection with the asset). The offset is applicable when the taxpayer holds more than a qualifying IP asset. In that case, the positive adjusted net qualifying income generated by a qualifying IP asset shall be offset against the negative adjusted income of any other qualifying IP asset. The positive net qualifying income after such adjustment and offset shall benefit from the partial exemption.

How is income receiving tax benefits treated under the new regime?

Under the new regime, the income receiving tax benefits, as computed above, will benefit from an 80% corporate income tax (CIT) exemption. Since the taxable basis for municipal business tax (MBT) purposes is the same as the CIT basis, the 80% exemption will apply for both CIT and MBT purposes.

Taking into account the CIT rate decrease taking place in 2018 and the additional MBT charge, the effective corporate tax rate applicable to the income receiving tax benefits will be 26.01 * 20% = 5.20%.

How are qualifying IP assets treated for net wealth tax purposes under the new regime?

IP rights qualifying for the new IP regime will benefit from a 100% net wealth tax (NWT) exemption.

Next steps

The introduction of a new IP regime will be positive for both Luxembourg taxpayers and for Luxembourg itself as the regime should attract new R&D activity to Luxembourg and strengthen existing IP management and development activities. IP regimes in countries participating in the BEPS project will become more and more similar in the future given that they will all have to comply with the modified nexus approach. Therefore, it was important that Luxembourg make the right choices and exhaust all options provided in the BEPS report: the Luxembourg legislator decided to adopt the optional 30% up-lift on qualifying expenses, which is good news for Luxembourg taxpayers.

The draft law also states that the transfer of a qualifying IP asset as part of a tax neutral transfer of business or autonomous part of business shall be realised as if no transfer had taken place. In addition, the scope of the regime might be expanded in the future as the concept of "IP assets functionally equivalent" to patents might evolve and be defined in future OECD publications. This new IP regime shall apply as from the 2018 tax year.

Originally published 08 August 2017

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.