- within Energy and Natural Resources topic(s)

- with readers working within the Oil & Gas and Law Firm industries

- within Energy and Natural Resources, Insurance, Government and Public Sector topic(s)

- with Finance and Tax Executives and Inhouse Counsel

With the continued procrastination in passing the Petroleum Industry Bill (PIB) and the consequent delay in bringing about the much vaunted reforms of the oil and gas sector in Nigeria, other African countries such as Angola are forging ahead by creating an enabling legal and regulatory environment that will attract additional investment to their oil and gas sector. The net effect of their progress, if Nigeria's reform programme continues to stall, is that its oil & gas sector will for the foreseeable future, remain stagnant with little possibility of attracting new investments.

The Angolan government recently passed a gas specific legislation Presidential Decree No. 7/18, which sets out the rules for the exploration and production of natural gas. Hitherto the passage of the new law, the legal framework for gas development in Angola particularly associated gas, was similar to that which obtains in Nigeria. Under Nigeria's extant petroleum laws, paragraph 35 (b) (i) of the first schedule to the Petroleum Act CAP 350 Laws of the Federation of Nigeria allows for the Federal Government to take natural gas produced with crude oil by a licencee or lessee, free of cost at the flare or at an agreed cost and without payment of royalty. In Angola, associated natural gas surplus for use by oil companies in their operations, was required to be made available to the state oil company (Sonangol) for free. This provision was however deemed too broad and devoid of the necessary features to incentivize investors to develop the gas subsector, hence the introduction of the new law.

Some of the salient provisions of the new law are as follows:

- Sonangol and the oil companies can explore, appraise, develop, produce and sell natural gas both in the international and domestic markets;

- Oil companies are to continue to have the right to use free of charge natural gas associated with their own operations and in the case they do not wish to use or sell the surplus gas, same should be made available free to Sonangol at a delivery point the latter is to designate; and

- Concession decrees and underlying agreements are to set specific longer periods for natural gas exploration and production activities than the ones already set for crude oil. In particular the periods for exploration, production, declaration of commercial discovery, term to develop the general development and production plan and first production following the commercial discovery declaration, can all be extended to accommodate the features of a natural gas project.

In terms of the applicable fiscal regime to govern gas development, the following rates are applicable:

- Petroleum production tax (royalty) is 5% (20% or 10% for crude oil);

- Petroleum income tax is 25% (50% for crude oil) it can be reduced to 15% for non-associated gas projects which proven reserves are 2TCF. This may apply to different fields subject to joint development; and

- Petroleum production Tax-Exemption (70% for crude oil).

The following costs are deductible for tax purposes:

- All costs incurred with the development and production of a non-associated gas discovery within a concession to explore and provide crude oil are deductible or recoverable for crude oil petroleum income tax (and petroleum production tax where applicable) purposes; and

- All costs incurred with the development and production of associated gas (including making the gas available to Sonangol at the designated delivery point plus the pipeline construction if necessary) are deductible or reasonable for crude oil production income tax (and petroleum production tax where applicable) purposes.

Nigeria on its part, has always treated the exploration and development of natural gas the same as crude oil and therefore lacks the clear and specific legal and fiscal framework needed to attract investment for the development of its vast natural gas reserves. Excess non associated gas utilized for crude oil operations is often flared depriving the government of much needed additional revenue. Perhaps in realization of the revenue loss, the government is proposing the Nigeria Gas Flare Commercialization Programme (NGFCP) which is designed to attract investment to develop its gas market, through a competitive procurement process of allocating gas flare sites to potential investors. The NGFCP is to be hinged on the proposed New Flare Gas (Prevention of Waste and Pollution) Regulations 2018 (Regulations) to be made pursuant to existing legislations - s.9 of the Petroleum Act and S. 5 of the Associated Gas Reinjection Act.

The Regulations as part of its objectives, seeks to curb the waste of natural resources, reduce the environmental and social impact caused by gas flaring and create social and economic benefits from gas flare capture. Similar to the new Angolan law, associated gas not being utilized by the Licensee or Lessee of a Licenced or Leased Area inclusive of marginal fields is to be made available to third party licensees under the procurement process for commercialization.

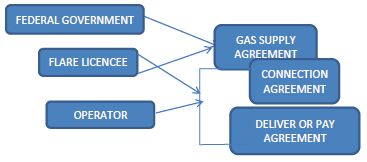

The commercial framework to underpin the programme as depicted below, forsees an agreement between the Federal Government and the Flare Permit holder (Flare Licencee) for the sale of contracted Flare Gas volumes to the Flare Licencee - Gas Supply Agreement; an agreement in respect of the connection of the respective facilities of the Operator and the Flare Licencee- Connection Agreement; and an agreement between the Operator and the Flare Licencee under which the Operator guarantees to supply an agreed volume of flared gas to a Flare Licencee - Deliver or Pay Agreement

ISSUES OF IMPORTANCE IN NEGOTIATING THESE COMMERCIAL AGREEMENTS GAS SUPPLY AGREEMENT (GSA)

A key feature of the GSA worthy of consideration during negotiation is the commitment from the Flare Licencee to Take-Or-Pay (TOP) a minimum annual quantity of flare gas. Take-or-pay provisions are fairly common in long-term gas supply and off take agreements and are designed to guarantee payment to the seller for a specified quantity of gas even where the buyer is unwilling or unable to take such quantities. It is also common for a buyer with a TOP obligation to seek a reciprocal right to Make-up gas by requesting later delivery as refund of the TOP payment later in the life of the contract.

The GSA will likely also include default provisions that gives the seller the right to suspend delivery for non-payment of an invoice. Given the novelty of the NGFCP, the Flare Licencees are will most likely be deemed not to be credit worthy and as such the Federal Government is likely to request under the GSA that they either pay in advance for the gas flare volumes, post a stand-by letter of credit or arrange some other form of credit support that will ensure the continued payment for the gas flare volumes received by the Flare Licencee.

There is the likelihood that the Flare Licencee may be supplied off-specification gas. In such circumstances, the Flare Licencee's remedy may be limited to the rejection of the off specification gas. Other remedies that may be considered in negotiation may include the offer of price discounts and allowing TOP credit for any off-specification gas taken by the Flare Licencee. Depending on the circumstances, a better approach may be to place an obligation on the Operator under the Deliver and Pay Agreement to adjust the operating efficiencies of its gas plant if the gas delivered fails to meet contract specifications for two or more consecutive months in a given contract year.

There may be instances of interruption in gas supply which is not excused either by reason of the Flare Licencee's failure to take delivery or Force Majeure. An option may be included in the agreement in favour of either the Flare Licencee or the Federal Government to make-up the shortfall in a subsequent period and with such later delivery sold at a reduced price (Shortfall gas price).

The issue of when title and risk of the flare gas is to be passed to the Flare Licencee is of key importance. The delivery point must be a precisely defined geographical location and based on the contractual arrangements envisaged under the programme, it is imperative to determine if the delivery point will be at the Operator's production facility, or the point of entry or exit of a multi-user pipeline. This will assist in determining which party is to bear the risk of transportation of the flare gas volumes. Where the transport arrangement is to be undertaken by a third party, it will be important to consider the extent to which the provisions of the GSA and the Deliver and Pay Agreement must be in alignment, particularly in relation to supply interruptions.

Often, force majeure clauses in GSAs do not address the issue as to whether the duration of the contract should be extended according to the time period that parties are prevented from performing the contract. In negotiating the GSA, this potential ambiguity should be addressed by allowing the duration of the contract performance to be extended for a period that is equivalent to the duration of Force Majeure.

Termination events will usually include extended supply interruptions, non-payment of a material amount, delivery of off-specification gas, breach of a material obligation, insolvency, extended events of force majeure, abandonment, termination of certain project documents e.g. Flare licence, Connection or Deliver or Pay Agreements. The termination events should be material and where applicable, reasonable cure periods should be negotiated.

CONNECTION AGREEMENT

Given that the flare sites may be in clusters and there may be multiple licencees using common connection facilities, regulatory and competition (antitrust) law issues will need to be considered in relation to access to these common facilities. The Regulation does not presently address the issue of third party access to processing facilities and pipelines on a non-discriminatory and cost-reflective basis.

In addition with the possibility of multiple users of common facilities, issues such as commingling of flare gas volumes will bring to the fore the principles of allocation and attribution as well as balancing which may necessitate additional contractual arrangements. Other issues of note will be infrastructure related such as pipeline crossing, abandonment and decommissioning.

DELIVER OR PAY AGREEMENT

The Deliver or Pay Agreement signifies a transportation agreement between the Operator and the Flare Licencee for the contracted flare gas volumes. It is important that the ship-or-pay obligation of the Operator is sufficiently tight in order to ensure certainty of payment from the Flare Licensee. Though the Regulation provides for a guaranteed fee by the Flare Licencee to the Operator. Key considerations in negotiating the contract should include whether the ship-or-pay obligation survives the occurrence of an event of force majeure to the Operators pipeline and facilities, and whether the Operator has a right of set-off against any amount owed to it by the Flare Licencee. Other aspects of the Operator's delivery obligations to take into consideration are the point-of-delivery as discussed above, delivery pressure and minimum quality specifications. Also as stated above, there must be consideration for third party access on a non-discriminatory basis to the Operators facilities.

CONCLUSION

Once formally introduced and the Regulation gazetted, the NGFCP and its enabling laws would have come in through the back door hopefully bringing with it, a breath of fresh air in terms of a cleaner, safer environment for the people of the Niger delta, new investments for the development of the gas sub-sector and employment opportunities.

Originally published July 2018

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]