Since the arrival of IFRS 16, the new standard on lease accounting, debates have arisen over how accounting for leases will change and how organisations will be affected. Even now, when IFRS 16 readiness comes up, it's clear that most issuers have not yet finished (or even begun) their impact assessments. With the standard becoming effective on 1 January 2019, the timeframe for assessments and system changes is getting a little bit narrow.

Scope

The new standard applies to all leases, including subleases, except:

- leases to explore our use of minerals, oil, natural gas, and similar unrenewable resources

- leases of biological assets held by a lessee

- service concession arrangements

- licences of intellectual property granted by the lessor

- rights held by a lessee under licensing agreements for items such as films, videos, plays, manuscripts, patents, and copyrights

Lessees can elect to apply the new standard to leases of intangible assets other than those listed above.

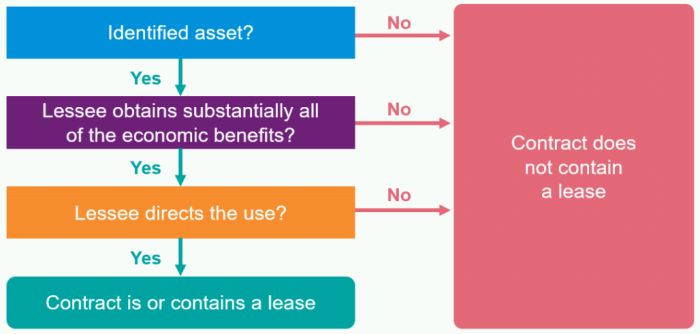

Are you sure that's a lease?

The first challenge is identifying whether a contract contains a lease, and whether contract components are separable:

Transition options

The new standard comes with a variety of transition combinations for the lessee, whilst leaving the lessor largely unaffected. The transition options include full retrospective and modified retrospective, the latter coming with further practical expedients which (contrary to the original intention) actually make this option more complex.

Identifying challenges

We believe that the biggest challenge for first-time IFRS 16 issuers might be the actual collection of the relevant data and determining how to use it. And this is without going into the details of changes in lease accounting, in what must be on balance sheet, or in the complexities surrounding the discount rate.

To prepare for all these challenges, entities need to understand the source of the necessary data and how to extract it. The following areas may require special attention:

- decentralised organisations

- contractual information outside of database system

- incentive received as part of lease renewal options

- discount rates

- separable components

- variable payments linked to index or rate where regular re-measurement is needed

- lost information

The next steps

Clients who have performed a meaningful impact assessment have had the following points in common:

- a dedicated IFRS 16 project team with defined objectives

- early identification of the lease population

- defined current IT capabilities and data gaps

- development of a detailed implementation plan

However you wish to go about it, one thing is clear: there's no more time for procrastination. Consider which practical steps your organisation needs to take in order to comply with the new requirements of this standard. If it means setting up a dedicated IFRS 16 project team, then now might be the time!

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.