- within Law Department Performance and Antitrust/Competition Law topic(s)

This briefing summarises recent legislation, cases and trends relevant to ongoing efforts to resolve the mortgage arrears crisis.

RECENT LEGISLATION

Recent legal and regulatory developments relevant to the mortgage arrears crisis have included:

- the Irish Courts being given the ability (following the enactment of the Personal Insolvency (Amendment) Act 2015) to overturn a secured creditor's decision to reject a borrower's proposal for a Personal Insolvency Arrangement (PIA) under the Personal Insolvency Act 2012 (see our recent briefing ( New Court Review Process Available for Rejected Personal Insolvency Proposals) for further details); and

- the reduction in the Irish bankruptcy term from 3 years to 1 year (see our recent briefing, ( Bankruptcy Term Reduced to 1 Year) for further details). This should reduce instances of 'bankruptcy tourism' and encourage more debt settlements outside of formal proceedings.

RECENT CASES

Recent cases in the mortgage arrears space deal with four main issues:

- Effect of non-compliance with the CCMA

-

Recent cases have followed the Supreme Court decisions in Irish Life and Permanent plc v Dunne & Irish Life and Permanent plc v Dunphy1 , holding that failure to comply with the Code of Conduct on Mortgage Arrears (CCMA) will not affect a lender's entitlement to an order for possession unless the lender has not complied with the moratorium provisions in the CCMA. In Stepstone Mortgage Funding Limited v Hughes, the Court granted an order for possession on the basis that that the lender had waited well in excess of the 12 month moratorium before taking repossession proceedings. The Court held that, while it considered CCMA compliance by the lender to be more formulaic than substantive, the moratorium provisions of the CCMA had been complied with and the order for possession should be granted.

- CCMA Clarifications

The courts have helpfully clarified two issues that have frequently caused confusion under the CCMA: - in Danske Bank v Higgins, the Court held that while the CCMA prohibits a lender from taking repossession proceedings without going through the MARP process, it does not prevent them from seeking judgment. This is consistent with our view that the CCMA is focused on repossession of a family home and does not prevent a bank from seeking other remedies not involving repossession, which could include not only seeking judgment but also taking action to enforce against other assets unrelated to the family home;

- in Fennell v Creedon, the Court held that the CCMA does not require that, following the MARP process, the only means of taking possession of a family home is through a court application for repossession. In that case, the lender had the right, following a default, to appoint a receiver. The Court held that the CCMA envisages multiple forms of repossession including the appointment of the receiver and, where the application of the CCMA does not resolve the issue between the parties, the terms of the mortgage determine the rights that then apply. If the mortgage predates 1 December 2009 and contains a right to appoint a receiver, the lender can appoint a receiver. This is a helpful clarification for lenders.

- Court Review Process for Rejected Personal Insolvency Arrangements

-

As mentioned at the start of this briefing, following the enactment of the Personal Insolvency (Amendment) Act 2015, a personal insolvency practitioner may (at a debtor's request) apply to Court for an order confirming that a PIA rejected by secured creditors comes into effect notwithstanding such rejection. Secured creditors have expressed considerable concerns over the likely operation of these provisions in practice. The first case involving an application to overturn a rejected PIA recently came before Monaghan Circuit Court – this resulted in Danske Bank's rejection of a PIA being reversed, and led to a Court-imposed write down. There are a number of other appeals in the system relating to refusals by lenders to agree to PIAs and the outcome of these further cases will be watched with interest.

- Jurisdiction of the Circuit Court in repossession

proceedings

Two conflicting High Court decisions relating to the jurisdiction of the Circuit Court in respect of repossession proceedings have led to delays in repossession proceedings where: the dwelling was built after May 2002 (when the Valuation Act 2001 came into operation); - the mortgage was entered into before 1 December 2009 (when the Land and Conveyancing Law Reform Act 2009 came into operation); and

- the repossession proceedings were initiated before 31 July 2013 (when the Land and Conveyancing Law Reform Act 2013 was came into operation).

- In Bank of Ireland Mortgage Bank v Finnegan, Murphy J held (in May 2015) that the Circuit Court did not have jurisdiction to hear such repossession proceedings. In Bank of Ireland Mortgage Bank v Hanley, Noonan J held (in November 2015) that the Circuit Court did have jurisdiction.

- Both decisions were on appeal from the Circuit Court and cannot themselves be appealed. It is possible that a High Court judge, if hearing a case with a similar fact pattern, could state a case to a higher Court to obtain clarity, and it remains to be seen whether this will take place quickly with a view to giving lenders and those in mortgage arrears certainty on this issue.

RECENT TRENDS

Both the Central Bank of Ireland and the Courts Service of Ireland have recently released the latest statistics on residential mortgage arrears and repossession for the fourth quarter of 2015. A number of key trends can be observed:

- Arrears

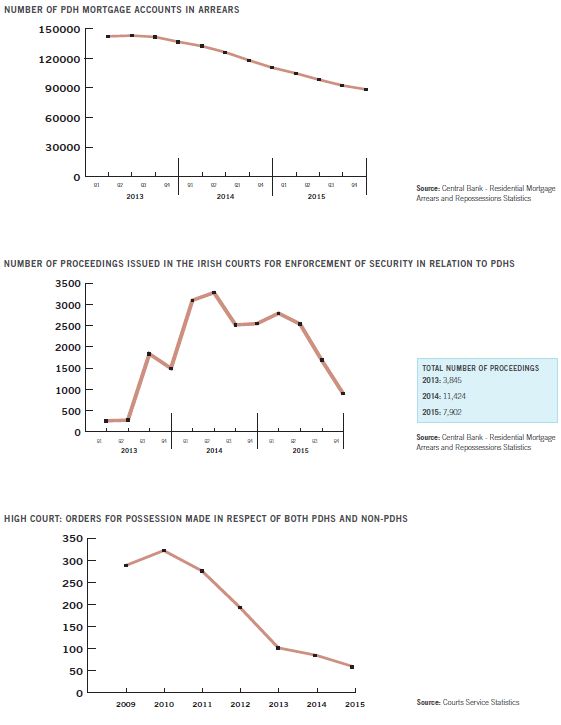

The number of residential mortgage accounts in arrears continued to decline for the tenth consecutive quarter, with 11.8% of all residential mortgage accounts in arrears by the end of December 2015. A total of 88,292 residential mortgage accounts were in arrears at the end of 2015, a decline of 4.4% relative to the previous quarter. - Proceedings issued

The last quarter of 2015 saw a 64.8% decrease in the number of proceedings issued in the Irish Courts for the enforcement of security in respect of primary dwelling houses (PDHs), as against the same period in 2014. Overall, a total of 11,424 proceedings were issued in the Irish Courts during 2014, with a total of 7,902 issued in 2015. The number of proceedings issued peaked in the second quarter of 2014, with 3,274 proceedings issued. - Possession orders made

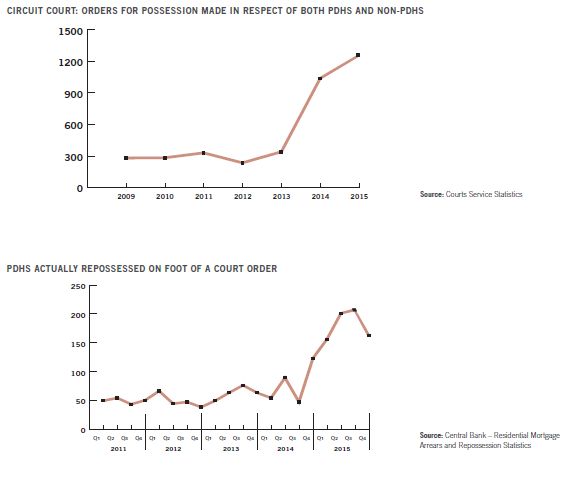

A total of 1,348 orders were made for possession of both PDHs and non-PDHs across the High Court and Circuit Court in 2015, an increase of 195 (16.9%) as against 2014. In the Circuit Court alone, 1,284 orders for possession were made in 2015, an increase of just over 20% on 2014 and in stark contrast to the total of 363 orders made in the Circuit Court in 2013. Of the total 1,284 orders made in the Circuit Court in 2015, only 210 orders were made in the last quarter and this is likely to be a result of the conflicting decisions involving Bank of Ireland Mortgage Bank (referred to earlier in this briefing). Separately, there has been a continued decrease in the orders made for possession in the High Court, with a total of 64 orders made in 2015. - PDHs actually repossessed

The total number of PDHs actually repossessed on foot of orders made in the High Court and Circuit Court in 2015 came to 726, compared against the total of 313 PDHs repossessed in 2014. There was, however, a slight decrease in the last quarter of 2015 with 162 PDHs repossessed in that period, when compared to the peaks of 201 and 207 in the second and third quarters of 2015 respectively.

In its Spring 2016 Quarterly Economic Commentary, the Economic and Social Research Institute also noted that, at the end of 2015, the number of mortgages in negative equity had fallen to below 100,000 for the first time since 2008 (to 99,950).

Footnotes

1 For further details on these cases, see our 2015 briefing (Breaking the Code: Failing to comply with the Code of Conduct on Mortgage Arrears)

This article contains a general summary of developments and is not a complete or definitive statement of the law. Specific legal advice should be obtained where appropriate.

[View Source]