On 2 June 2023, the Federal Council adopted the amendments to the Insurance Supervision Ordinance and put the revised Insurance Supervision Act and the revised Insurance Supervision Ordinance into force as of 1 January 2024. On 21 August 2023, the Swiss Financial Market Supervisory Authority FINMA published an action plan for insurance intermediaries: it calls on insurance intermediaries to inform themselves and ensure that they meet the new (increased) requirements.

Starting Point

On 18 March 2022, the Swiss parliament approved the partial revision of the Insurance Supervision Act (nISA). On 2 June 2023, the Federal Council gave its approval to the amendments to the Insurance Supervision Ordinance (nISO) and at the same time put the nISA and the nISO into force as of 1 January 2024. Among other things, the revised insurance supervision law provides for far-reaching changes for insurance intermediation. The Swiss Financial Market Supervisory Authority FINMA (FINMA) therefore published an "Action Plan for Insurance Intermediaries" on 21 August 2023, as part of the supervisory notice 04/2023. In such notice, FINMA calls on insurance intermediaries to inform themselves and take appropriate action.

What to do?

FINMA has identified the following actions that insurance intermediaries should take:

1. Check Applicability of Insurance Supervision

Insurance intermediaries must consider whether their current or planned activities will qualify as insurance intermediation as of 1 January 2024. As under the current insurance supervision law, concluding and offering insurance contracts in the interest of insurance companies or other persons is considered insurance intermediation. The concept of offering is subject to interpretation. As of 1 January 2024, it is clear that it will also be considered insurance intermediation activity if a person has an economic interest in offering or concluding of an insurance contract through a website or another electronic medium, and (i) provides information, based on individualized criteria, about one or more insurance contracts that a policyholder can choose through the website or the electronic medium, or (ii) provides a ranked list of insurance products.

Insurance intermediation does not include (i) the mere provision of data or information and (ii) the intermediation of annex insurance (annual insurance premium less than CHF 600 (excluding taxes), insurance is a subordinate service to the provision of a product or service, intermediation is a secondary activity).

If you are interested in checking whether you are subject to the Swiss insurance supervision law, you can use our form for self-assessment of insurance intermediation (FSAII) . You can download the form here.

2. Define Intermediation Type

As of 1 January 2024, insurance intermediaries may only be either tied or non-tied (so-called type constraint). At present, it is possible – and quite common – for insurance intermediaries to be non-tied in certain lines of insurance and tied in others.

Insurance intermediaries who have been active in a mixed form up to now must decide on one type of intermediation. There is likely to be a need for adjustment and/or dissolution in this regard, particularly with regard to cooperation agreements. In addition, insurance intermediaries who wish to discontinue their non-tied insurance intermediary activities as of 31 December 2023 must notify FINMA about such decision by 31 December 2023 (by 15 December 2023 via the electronic intermediary portal, thereafter in writing).

3. Register Entry

- Updating the Existing Register Entry: The non-tied insurance intermediaries must check whether their register entry is correct. Changes can be entered via FINMA's intermediary portal until 15 December 2023. From 16 December 2023 until 31 December 2023, changes must be reported to FINMA in writing.

- New Registration: If the check of the applicability of the insurance supervision shows that an insurance intermediation activity exists as a non-tied insurance intermediary as of 1 January 2024, an application for entry in the intermediary register must be submitted. Until 17 November 2023, this can be done via the existing intermediary portal (WebReg). From 18 November 2023 until 31 December 2023, the application must be submitted in writing. The insurance intermediation activity may be carried out only after the registration in the intermediary register has been made (even if the application for registration was filed before 1 January 2024). In the event of a deliberate violation of this rule, the penalty is imprisonment for up to three years or a fine, and in the event of negligence, a fine of up to CHF 250,000.

Tied insurance intermediaries may no longer be entered in FINMA's intermediary register. Consequently, FINMA will delete all tied insurance intermediaries entered in the intermediary register on 31 December 2023 as of 1 January 2024. In the future, tied insurance intermediaries can only be entered in the intermediary register if an entry in the register in Switzerland is required by the respective state for the activity abroad. Existing tied insurance intermediaries, who must necessarily have such a register entry, should promptly request FINMA to retain the register entry.

4. Subsequent Documentation

Non-tied insurance intermediaries who were entered in the intermediary register before 1 January 2024 must submit to FINMA all information and documents relating to the application for registration as a non-tied insurance intermediary by 30 June 2024. The information on this can be found in Annex 6 of the nISO (not available in English). The application must be submitted via FINMA's survey and application platform (EHP). The deadline for subsequent documentation cannot be extended (unless the Federal Council decides otherwise). FINMA expects up to 12,000 new registrations or post-documentations.

If an non-tied insurance intermediary no longer meets the requirements for the entry in the intermediary register, it will have to be deleted and the non-tied insurance intermediary may no longer engage in non-tied insurance intermediation activities. This may primarily affect foreign non-tied insurance intermediaries who must now have their registered office, place of residence or branch office in Switzerland (exceptions reserved, but there is an obligation to designate a Swiss domicile for service).

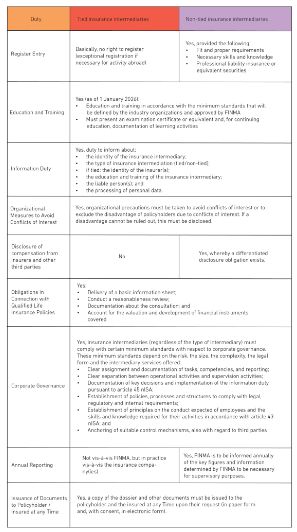

5. Compliance with the New Obligations

As of 1 January 2024, the increased requirements of the nISA and the nISO must then be complied with. The table below provides an overview:

FINMA Intermediary Symposium

The current supervision of insurance intermediaries is a so-called register supervision. FINMA therefore primarily examined registration and amendment applications. FINMA investigated complaints in individual cases only. As of 1 January 2024, the insurance intermediary supervision will be an ongoing supervision, which significantly expands FINMA's supervisory spectrum. To explain this new regime, FINMA had already outlined the broad principles relating thereto on 23 May 2023 on the occasion of the "Small Insurer Symposium 2023". FINMA is now offering insurance intermediaries and insurance company representatives three additional information events to be held in October 2023 (more information here).

Do you need a guide for a first assessment whether your activities qualify as insurance intermediation? We provide you with our form for self-assessment of insurance intermediation (FSAII) free of charge. Please note that this is an auxiliary tool and the FSAII does not constitute legal advice. Click here.

More information

Further information on the revised insurance supervision law in general and the revised insurance intermediation law in particular can be found via the following links:

- Dispatch on the amendment of the Insurance Supervisory Act (ISA) dated 21 October 2020, BBL 2020 8967

- Text of final vote for the Federal Act on the Supervision of Insurance Companies (Insurance Supervisory Act, ISA), BBl 2022 704

- Preprint of the Ordinance on the Supervision of Private Insurance Companies (Insurance Supervisory Ordinance, ISO)

- Explanatory report on the amendments to the Insurance Supervisory Ordinance dated 2 June 2023

- Result report of the consultation procedure on the amendments to the Insurance Supervisory Ordinance of 2 June 2023

- Small Insurer Symposium 2023, 23 May 2023.

- FINMA supervisory notice 04/2023 dated 21 August 2023

Originally Published 24 August 2023

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.