In response to the Foreign-sourced Income Exemption ("FSIE") guidance promulgated by the European Union ("EU") in December 2022, the Hong Kong Special Administrative Region ("HKSAR") government has proposed refinements to the existing FSIE Regime. For details of the existing FSIE Regime, please refer to our tax update published on 9 January 2023.

Under the refined FSIE Regime, the scope of property in relation to foreign-sourced disposal gains will be expanded to cover all types of property. Further, a new intra-group relief will be introduced for property transfers between associated entities, subject to specific anti-abuse rules, in addition to the existing exception requirements on disposal gains.

The Inland Revenue (Amendment) (Taxation on Foreign-sourced Disposal Gains) Bill 2023 (the "2023 Amendment Bill") was gazetted on 13 October 2023 and will be implemented effectively from 1 January 2024.

What are the key updates under the refined FSIE Regime?

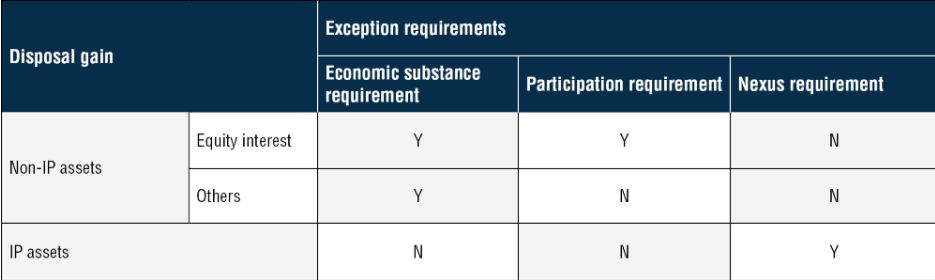

1. Extension of scope of income and applicability of exception requirements

The scope of the disposal gain will be expanded beyond its original coverage, which only included the gain from selling equity interests in an entity. It will now encompass the gain derived from selling any type of property, including movable and immovable property. As a result, the existing exception requirements, such as the economic substance requirement, participation requirement and nexus requirement, will also be broadened to apply to disposal gains on different types of properties. These gains can be further categorised as intellectual property ("IP") disposal gains and non-IP disposal gains, reflecting the distinction in exception requirements between the two types of property.

In particular, the disposal gain from property will not be brought into charge under the FSIE Regime if the exception requirements are met. The exception requirements are as follows:

For details of the exception requirements, please refer to our previous tax update dated 9 January 2023.

2. New relief introduced and exclusion list expanded

The 2023 Amendment Bill has introduced new relief for foreign sourced disposal gains derived from properties transferred between associated1 entities ("Intra-group Transfer Relief"). Additionally, the foreign sourced disposal gains on non-IP assets derived by a trader2 will be excluded from the refined FSIE Regime ("Trader Exclusion").

a. Intra-group Transfer Relief

Subject to certain anti-abuse measures, any tax which would have been charged on foreign sourced disposal gains derived from intra-group transfer between associated entities could effectively be deferred.

The effect of such deferral is that the transferor is deemed to have sold the property at consideration with no gain or loss, while the transferee is deemed to have acquired the property at the same cost and on the same date as the transferor. The transferee is also able to claim expense deductions/capital allowances/tax credits on the property acquired as if it were the transferor.

b. Trader Exclusion

Under the refined FSIE Regime, foreign sourced disposal gains from non-IP assets which are derived by a trader of assets will be excluded from the refined FSIE Regime.

3. Application of Commissioner's opinion ("Opinion") on the extended scope of income ("Transitional Measure")

To obtain tax certainty and alleviate the compliance burden, multinational enterprise ("MNE") entities can, prior to 1 January 2024, apply for the Opinion on their compliance with the economic substance requirement concerning disposal gains on the extended scope of properties to be accrued on or after 1 January 2024. If a favourable Opinion has already been obtained under the existing FSIE Regime, MNE entities can apply to expand the scope of the previously obtained Opinion to include disposal gains from the extended scope of properties.

The Transitional Measure described above will end once the 2023 Amendment Bill comes into effect, and MNE entities can then apply for advance rulings regarding their compliance with the economic substance requirement going forward.

Advance rulings under the existing FSIE Regime in Hong Kong

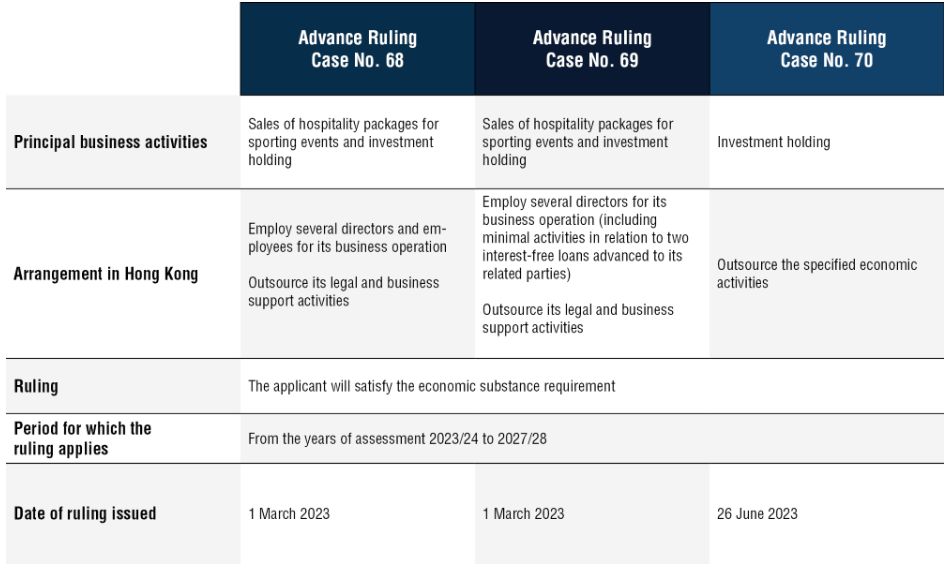

Under the existing FSIE Regime, three advance rulings, i.e., Advance Ruling Case No. 68 to 70, have recently been published by the Inland Revenue Department ("IRD") in favour of the applicants regarding the compliance with the economic substance requirement. In particular, all three cases concern private, limited companies incorporated in Hong Kong which are considered MNE entities but not pure equity holding companies. The details of the three cases are summarized as follows:

Following the above observations, the recent advance rulings published by the IRD have provided valuable insights on compliance with the economic substance requirement under the FSIE Regime. These rulings, which were published in favour of the applicants, have undoubtedly demonstrated that seeking an advance ruling from the IRD can provide entities with clarity and certainty regarding their tax positions, especially on the application of the FSIE Regime and its underlying exemption requirements. By proactively engaging with the IRD and obtaining an advance ruling under the FSIE Regime, entities can further enhance their tax planning strategies, reduce compliance burden, reduce potential disagreement with its auditors on whether a tax provision is required and mitigate the risk of unexpected tax liabilities in a fully compliant manner.

Tax certainty enhancement scheme ("TCES") for onshore disposal gain

Considering the uncertainty surrounding the application of the FSIE Regime and its exemption requirements, taxpayers may, in the future, explore an alternative approach of conducting transactions onshore in Hong Kong following the introduction of the TCES. By doing so, the resulting gains would not fall within the scope of the FSIE Regime.

In this regard, the government proposes to introduce the TCES for eligible investor entities3 deriving onshore disposal gain from the sale of equity interests in an investee entity. In particular, the Inland Revenue (Amendment) (Disposal Gain by Holder of Qualifying Equity Interest) Bill 2023 was gazetted on 20 October 2023 and is expected to be implemented effectively from 1 January 2024.

Subject to the conditions and exclusions proposed under the TCES, the onshore disposal gain can be treated as non-taxable under the TCES. This treatment saves the need for applying the existing badges of trade analysis to determine whether a gain is of a capital nature.

Basic conditions: The current proposal suggests that the investor entity should maintain a minimum of 15 percent of the total equity interest in the investee entity for a continuous period of at least 24 months prior to the disposal of the equity interests.

There are also two proposed flexible arrangements for meeting the basic conditions, which are as follows:

(i) The equity interests held by the investor entity and its closely related entities can be aggregated to meet the 15 percent ownership threshold; and

(ii) Disposal in tranches is allowed, subject to a 24-month restriction.

Exclusions: The current proposal suggests the following exclusions from applying the TCES:

(i) The investor entity is engaged in insurance business;

(ii) The investee entity is unlisted and engaged in immovable property related business (i.e., business of trading, development4 and holding5 of immovable properties in Hong Kong or overseas); or

(iii) The equity interests in the investee entity have previously been treated as trading stock of the investor entity for tax purposes based on the "badges of trade" analysis.

Takeaways from the refined FSIE Regime and TCES

Given the expanded scope of charge under the refined FSIE Regime, it is highly advisable for MNE entities to conduct a thorough review of their group holding and operational structure. This assessment will help evaluate the risk of falling under the purview of the refined FSIE Regime in Hong Kong. Furthermore, it is also recommended to seek clarity and certainty by submitting an application for the Opinion or an advance ruling with the IRD regarding the application of the (refined) FSIE Regime and its associated exemption requirements.

Alternatively, MNE entities may find it worthwhile to consider conducting transactions onshore in Hong Kong and utilizing the TCES for the sake of simplicity. The tax certainty offered by the TCES presents an appealing option in this regard.

Last but not least, it is worth noting that similar schemes have been/ are planned to be implemented in other regions as well. In our next tax update, we will compare the relevant schemes among Hong Kong, Singapore, and Malaysia. Stay tuned for more information!

Footnotes

1. Two entities are associated with each other if–

a. Either one of the companies has at least 75 percent

beneficial interest of another company; or

b. A third entity holds at least 75 percent beneficial interest of

each of the two companies.

2. Trader is defined in the 2023 Amendment Bill as an entity that sells, or offers to sell, property in the entity's ordinary course of business.

3. Eligible investor entity covers legal person and an arrangement that prepare separate financial accounts such as partnership and a trust.

4. Referring to property developers who do not use their developed immovable property for carrying on their business and deriving trading/business income (including income derived from property letting business) or have undertaken any property development activities in the past 60 months before the disposal of equity interest.

5. Referring to "property rich" companies of which more than 50 percent of the total assets are consist of immovable properties.

Originally published November 5, 2023

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.