LAW NO. 26 FOR THE YEAR 2020

On May 7th, 2020, the Government of Egypt issued Law No. 26 for the year 2020 that amended specific articles in the Income Tax Law No. 91 for the year 2005 (Articles No. 8, 13, 87). Article No.8 relates to the law regarding the income tax rates applicable to individuals, Article No.13 relates to personal allowances (personal income exemption) and Article No.87 relates to penalties on tax return differences. The application of the law will commence as of July 2020 for salaries and for commercial, industrial, and manufacturing (sole proprietorship and partnerships), professional, non-commercial or real estate taxpayers starting from the following tax period being January 2020.

Under the new law, the applicable progressive tax rates will depend on the taxpayers' annual income, to help support low income earners by reducing their tax burden.

SUMMARY OF AMENDMENTS (ARTICLES NO. 8 & 13)

- The abolishment of tax discounts for individuals

- The annual personal allowance exemption increased from EGP 7,000 to EGP 9,000

- The 1st tax bracket is subject to 0% and has increase from EGP 8,000 to EGP 15,000

- Two new tax brackets have been introduced; a bracket ranging from EGP 15,000 to EGP 30,000 and another for over EGP 400,000

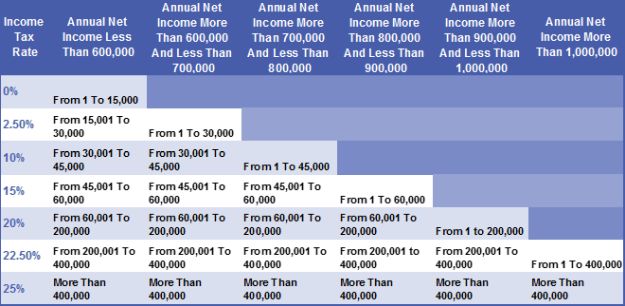

- Taxpayers with high net taxable incomes are not allowed to benefit from the lower tax brackets as per below:

-

- An annual net taxable income ranging between EGP 600,000- EGP 700,000 is not eligible for the 0% tax bracket

- An annual net taxable income ranging between EGP 700,000- EGP 800,000 is not eligible for the 0% & 0.25% tax brackets

- An annual net taxable income ranging between EGP 800,000- EGP 900,000 is not eligible for the 0%, 0.25%, & 10% tax brackets

- An annual net taxable income ranging between EGP 900,000- EGP 1,000,000 is not eligible for the 0%, 0.25%, 10%, & 15% tax brackets

- An annual net taxable above EGP 1,000,000 is not eligible for the 0%, 0.25%, 10%, 15%, & 20% tax brackets

Below is a table illustrating the above:

FINANCIAL PENALTIES

The amendment of Article 87 is related to financial penalties on tax differences identified through tax audits carried out by the Egyptian Tax Authorities.

- If the tax differences are less than 50% of what was paid per the submitted tax return, the financial penalty will be 20% of the tax differences identified.

- If the tax differences are more than 50% of what was paid per the submitted tax return, the financial penalty will be 40% of the tax differences identified; the same will be applied if no tax return was submitted.

The law also gives taxpayers the opportunity to reduce the penalty rates by 50% if an agreement is reached before referring the case to the Appeal Committee.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.