- within Corporate/Commercial Law topic(s)

- in United States

- with readers working within the Law Firm industries

- within Transport and Immigration topic(s)

Introduction

Guernsey is renowned for being one of the leading jurisdictions for fiduciary work having built a strong reputation over decades and providing private clients with the right wealth structures quickly and with a high degree of expertise and professionalism.

One of the trends in recent years has been the emergence of the private trust company (PTC). Its popularity has grown as ultra-high net worth families look to consolidate their various family interests in a bespoke private structure. The PTC offers many benefits such as the ability of the settlor or his or her trusted advisers to be closely involved with the structure, in-house specialist knowledge and expertise, continuity, flexibility and potential cost efficiencies.

Many jurisdictions have actively been trying to attract and encourage the establishment and administration of PTCs by excluding or exempting PTCs from their regulatory and licensing regimes. Regulations in the British Virgin Islands provide for an automatic exemption from licensing for PTCs provided certain conditions are met. The Cayman Islands allows for two types of PTCs (licensed and registered). Cayman-registered PTCs are subject to minimum regulation. Jersey enables PTCs to be established provided they meet tests set out in a trust company business exemptions order. In Guernsey, a PTC does not need a fiduciary license if the PTC is not remunerated for its services as a trustee. If the PTC is remunerated it may apply for a discretionary exemption by the Guernsey Financial Services Commission (the Commission) and, failing that, it would need a fiduciary licence.

Local licensed trust professionals, who are subject to oversight and inspection by the Commission, continue to play a central role in PTCs by delivering administration services and/or providing the necessary trust experience and expertise on the boards of PTCs.

As mentioned the Fiduciaries Law1 only applies to fiduciary services provided by way of business. If a PTC is paid, directly or indirectly, it will be deemed to be carrying on business and subject to the Fiduciaries Law. PTCs generally need on-going funding, particularly in complicated structures and, rather than having to fund the PTC upfront, the PTC may wish to charge administrative or management fees to the structures under its control. In that case the PTC will either need to apply for a fiduciary license or alternatively an exemption under the Fiduciaries Law.

The Commission has discretion as to whether or not to grant such an exemption. The Commission evaluates each application on its own merits but historically exemptions have generally been granted on the condition that the PTC does not offer its services to the public but that these are limited to a particular family or connected group of persons. The Commission would normally require that the board of the PTC includes at least one corporate director holding a full fiduciary license and that the licensee is responsible for the administration of the PTC. Although Guernsey therefore does not have a statutory exemption regime as is found in the BVI, Cayman as well as Jersey, the discretionary regime does allow for the Commission to grant exemption and to respond appropriately after evaluating the merits of each application.

Typical Structure

Frequently a double structure of a company and a trust are used to establish the PTC arrangement. A typical PTC is a limited company established for the sole purpose of acting as trustee of a trust or group of related trusts. In order to avoid issues arising from ownership or control of the PTC, the shares in the PTC are usually 'orphaned'. In Guernsey this can be achieved by the shares being held by the trustee of a non-charitable purpose trust2. In BVI and Cayman, VISTA and STAR trusts are frequently used. A locally regulated fiduciary will therefore still be required to act as trustee of the trust which adds an additional layer of administration and cost. Charitable trusts and companies limited by guarantee are also sometimes used to hold the shares in a PTC. An example of a typical Guernsey PTC structure can be seen in Fig 1.

The Guernsey Foundation

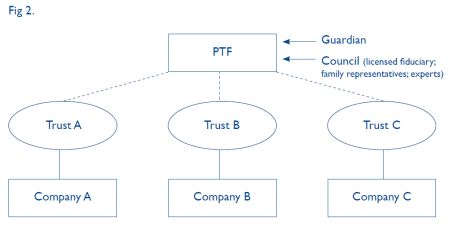

As an alternative to the typical PTC double structure described above, a Guernsey Foundation can be used to replace both the PTC and the purpose trust. A private trust foundation (PTF) can be established for the sole purpose of acting as a trustee. Receipt of remuneration for its services as trustee would be incidental to that purpose and would mean the foundation was not carrying out commercial activities which every foundation is prevented from undertaking.

As a legal person of full corporate capacity, a foundation is able to act and exercise all the powers, and would be bound to the obligations, of a trustee in the same manner as any trustee which is a company. Unlike a company, a foundation has no members or shareholders and is therefore already an orphaned structure. Accordingly there is no need to establish a trust or other holding vehicle to deal with issues arising from ownership and control (founders will still need to be mindful of control issues when deciding who is to hold the power to appoint and remove councillors under the foundation's constitution).

The result is a simplified single structure consisting of a private trust foundation (PTF).

Regulation

A PTF will not require a license if it does not receive any payment for its services as trustee. If it does receive any form of payment, whether directly or indirectly, the same considerations should apply as for any application for an exemption for a PTC. The Commission considers applications on a case-by-case basis and has discretion as to whether or not to grant a PTF an exemption from the requirement to hold a fiduciary license.

Carey Olsen advised in relation to the first PTF sanctioned by the Commission which was established in 2013.

The Commission has previously granted the PTF an exemption from the requirement to hold a fiduciary license on condition that a holder of a full fiduciary license is on the council and that any other remunerated council members who are resident in Guernsey hold personal fiduciary licenses. In addition, the Commission requires that the constitution should expressly require all councillors to ensure that the foundation complies with its fiduciary duties as trustee.

The establishment of a PTF may be a useful alternative to the customary PTC. Benefits of the PTF would include the avoidance of the complexity and cost required by the double company and trust required for the typical PTC structure. A PTF should be able to obtain an exemption from the requirement to hold a fiduciary license under the Fiduciaries Law provided it does not provide services to the public but acts as trustee of trusts established for a family, or closely defined group of beneficiaries, and there is an appropriate level of involvement by a local, fully licensed fiduciary, as well as personal licence holders.

Despite the maturity of the fiduciary sector in Guernsey, the jurisdiction has repeatedly proven that it takes a pragmatic, timely and professional approach to the ever-increasing variety of structures demanded by private clients. It is this fleet of foot and the high level of professionalism from the finance industry and associated professions, that maintains Guernsey's firm position as a leading offshore jurisdiction for private clients.

Footnote

1. The Regulation of Fiduciaries, Administration Businesses and Company Directors, etc (Bailiwick of Guernsey) Law, 2000.

2. A non-charitable purpose trust can be established under section 12 of the Trusts (Guernsey) Law, 2007 for the purpose of holding shares and does not have any beneficiaries.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]