- in Africa

- in Africa

- with readers working within the Property industries

- within Immigration, Consumer Protection, Media, Telecoms, IT and Entertainment topic(s)

In our previous article, The Protection of Sovereignty Act: A Compliance Risk for Banks and Money Remittance Agencies (June 2026), we examined the obligations imposed on supervised institutions by the Protection of Sovereignty Act, (the “Act”)(section 25). It focused on the severity of the gatekeeping function on payments to agents of foreigners, the difficulty of identifying an “agent of a foreigner” in the absence of a public register, and the potentially catastrophic penalty of up to UGX 4 billion for non-compliance.

The analysis in our previous article remains sound in so far as it describes the obligations and penalties that attach once section 25 is engaged. However, that analysis did not consider in detail the application or gateway provisions of the Act, in particular section 2(4) and section 2(5), which operate as threshold exemptions and may, in a significant proportion of ordinary banking transactions, provide much needed relief to the banks and money remittance agencies.

This article now re-examines the gateway provisions and proposes a staged compliance test that supervised institutions may employ to determine whether section 25 applies to a given transaction.

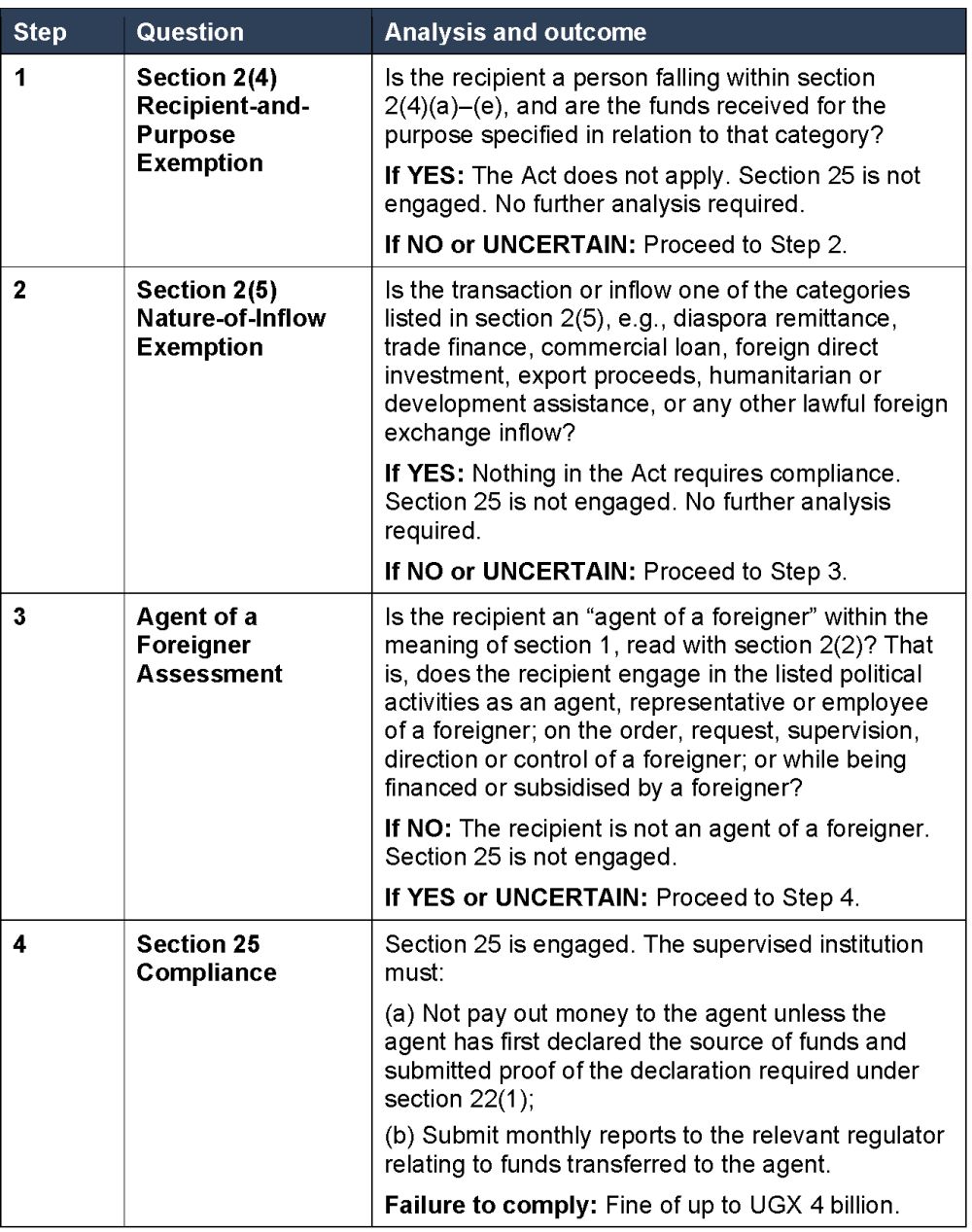

Section 2(4): The recipient-and-purpose exemption

Section 2(4) provides that, the Act shall not apply to monies or funding received from a foreigner by specified categories of recipient, provided the funds are received for specified purposes. The exempted categories include:

- any person or institution regulated by a regulatory body, for the purpose of meeting regulatory requirements or undertaking its commercial, licensed or permitted activity;

- a health or medical facility, for lawful permitted health or medical activity;

- an academic or research institution, for funding research, innovation or other lawful educational activity;

- a person, for commercial, domestic or family use; and

- a faith-based organisation, for activities connected with its mission.

This is a recipient-and-purpose exemption: it applies only where both the recipient falls within a specified category and the funds are received for the specified purpose associated with that category. An insurance company receiving foreign funds for meeting capital adequacy requirements or a bank taking deposits, would be within this exception. We trust that from a governance standpoint, a regulated entity would never receive funds outside its licensed activities.

Section 2(5): The transaction/nature-of-inflow exemption

Section 2(5) provides a further, and broader, exemption by reference to the nature of the transaction or inflow rather than the identity of the recipient. It exempts any lawful foreign exchange inflow or outflow, including lawful foreign direct investment, portfolio investment, diaspora remittances, export proceeds, trade finance, commercial loans, humanitarian assistance, grants, concessional financing, and development assistance.

The breadth of this provision is striking. It effectively exempts all lawful cross-border financial flows from the requirements of the Act. This is consistent with the Act’s policy objective of targeting political funding routed through agents of foreigners, rather than ordinary commercial, personal or development related capital flows.

When the above exemptions are read together, they establish that the Act is directed at a relatively narrow class of transactions: those involving funds received by an agent of a foreigner for the purpose of carrying out the political activities specified in section 2(2), where the funds do not fall within any of the lawful categories enumerated in sections 2(4) and 2(5).

Admittedly, the phrases used in the exemptions are vague for instance "commercial, domestic or family use" or "diaspora remittances" or “lawful foreign direct investment”. Would this not mean that any monies whatsoever received by a Ugandan individual would be exempt from application of the Act?

Four-step compliance test

Considering the application provisions, we recommend that supervised institutions adopt the following staged compliance test when processing cross-border receipts or payments. The test is designed to ensure that section 25 is applied only to those transactions that genuinely fall within the mischief of the Act, and to provide a principled basis for concluding that a given transaction does not attract the obligation.

The critical insight of this staged approach is that 16 million transactions in remittances to Uganda, per annum, may well be resolved at Step 1 or Step 2 without any need to consider whether the recipient is an agent of a foreigner or to apply section 25 at all.

Practical significance of the exemptions

The application provisions significantly narrow the universe of transactions to which section 25 applies. Consider the following practical scenarios:

Diaspora remittances: A money remittance agency processing a transfer from a Ugandan national in the diaspora to a family member in Uganda is facilitating a “diaspora remittance” within section 2(5). The Act does not require compliance, and section 25 is not engaged, irrespective of the recipient’s identity or other activities.

Trade finance: A bank confirming a letter of credit in favour of a Ugandan importer, with funds originating from a foreign buyer’s bank, is facilitating “trade finance” within section 2(5). The exemption applies regardless of the identity of the beneficiary.

Commercial loan proceeds: A bank receiving and disbursing the proceeds of a commercial loan from a foreign lender to a Ugandan borrower is processing a “commercial loan” within section 2(5).

Regulated commercial activity: Where a bank itself receives funds from a foreign correspondent bank in the course of its licensed banking activity, for example, settlement of interbank obligations or NOSTRO account funding, section 2(4)(a) provides a recipient-and-purpose exemption because the bank is a supervised institution receiving funds for the purpose of undertaking licensed activity under an Act of Parliament.

In each of these cases, the compliance test terminates at Step 1 or Step 2. The supervised institution need not proceed to the more difficult question of whether the recipient is an “agent of a foreigner.”

Why the compliance burden remains harsh

Notwithstanding the relief provided by sections 2(4) and 2(5), the compliance burden on supervised institutions remains formidable. The difficulty arises not from the architecture of the exemptions themselves, but from the practical challenge of applying them with certainty in the absence of independent verification sources.

Reliance on customer declarations

To determine whether a transaction falls within the section 2(4) or section 2(5) exemptions, a supervised institution will need to rely on information provided by the customer, that is, by the recipient of the funds. This creates a fundamental structural weakness:

- Purpose of funds: Section 2(4) requires the institution to satisfy itself that funds are received for a specified purpose (e.g., “commercial, domestic or family use”). The institution has no independent means of verifying the purpose for which a customer intends to use received funds. It must rely on the customer’s declaration.

- Nature of inflow: Section 2(5) requires the institution to classify the transaction by type (e.g., “diaspora remittance” or “trade finance”). Whilst payment instructions and supporting documentation may indicate the nature of the transaction, the institution cannot independently verify the underlying commercial or personal reality. In cases of doubt, it must again rely on the customer’s representation.

- Agent of a foreigner status: If the exemptions are inconclusive, Step 3 requires the institution to assess whether the recipient is an “agent of a foreigner.” As noted in our earlier paper, there is no public register of agents, and no prescribed mechanism by which a supervised institution may make this determination independently.

This is not to overlook the difficulty of the straight-through remittances that hit a customer’s account or mobile phone directly, with no opportunity for a bank or remittance agency to intervene.

Absence of a statutory defence

The offence under section 25(3) is one of strict liability. The Act does not provide a statutory defence of “reasonable steps” or “due diligence.” A supervised institution that pays out money to a person who is in fact an agent of a foreigner, without having first obtained the declaration and proof required by section 25(1), commits the offence regardless of whether the institution made reasonable enquiries or obtained declarations from the customer that the exemptions applied.

Customer declarations may support arguments of good faith and mitigation in sentencing, but they do not, as a matter of law, create a defence to the charge. This is a significant compliance risk.

Until implementing regulations are promulgated or the Ministry issues guidance, supervised institutions are left to design their own compliance frameworks without any assurance that their approach will be regarded as sufficient.

Recommended approach pending regulatory guidance

In the interim, we recommend that supervised institutions adopt the following practical measures:

- Implement the four-step test as a documented compliance procedure, integrated into existing transaction-processing workflows.

- Obtain written customer declarations at account-opening and at the point of transaction where the nature or purpose of funds is not evident from the payment instruction itself. Declarations should address: (a) the nature of the inflow (by reference to section 2(5) categories); and (b) whether the customer is an agent of a foreigner within the meaning of section 1.

- Leverage existing AML/KYC procedures. The information gathered under Anti-Money Laundering Act requirements, including source-of-funds enquiries, beneficial ownership records, and customer risk profiles, will in many cases be sufficient to determine whether a section 2(4) or 2(5) exemption applies.

- Develop internal risk indicators to flag transactions that cannot readily be classified within the section 2(4) or 2(5) exemptions and that may require enhanced scrutiny at Step 3.

- Maintain contemporaneous records of the basis on which the institution concluded that a transaction was exempt. Even though a record of reasonable steps does not constitute a statutory defence, it is likely to be relevant to any prosecutorial decision and to mitigation.

- Bank of Uganda proactively engage the Attorney General to seek a written legal opinion on the obligations of supervised institutions and to advocate for the quick promulgation of implementing regulations under section 29.

Conclusion

The gateway provisions in sections 2(4) and 2(5) of the Protection of Sovereignty Act provide meaningful relief for supervised institutions. Properly understood, they ensure that the Act’s obligations are directed at a narrow class of politically motivated funding, and that the vast majority of ordinary banking and remittance transactions are not caught.

However, the relief is incomplete. The exemptions are factual in character, and supervised institutions lack independent means of verification. The absence of implementing regulations, a public register of agents, and a statutory defence of reasonable steps means that the compliance burden, whilst narrower than initially apprehended, remains structurally harsh.

We continue to recommend that industry participants engage actively with the relevant regulatory bodies to secure practical guidance and that supervised institutions document their compliance processes with care in the interim.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]