Consistent with annual procedures, the Japanese government proposed Japanese tax reforms for 2016 last December. Several of the proposed reforms are focused on further advancing the overall economic reform program of the coalition government led by Prime Minister Abe (often referred to as 'Abenomics'). The entire reform package provides for reforms in the corporate tax, consumption tax and individual tax areas as well as addressing long standing issues such as online sales and the OECD anti-tax avoidance project known as BEPS. This update focuses solely on those reforms specific to corporate tax payers. The effective date of the proposed reforms discussed below was April 1, 2016 and includes:

- the reduction of national corporate tax rates

- the changes to the enterprise tax and special local corporate taxation scheme;

- the changes to the Net Operating Loss carry-forward and deduction limitation;

- the provisions related to corporate reorganizations;

- the controlled Foreign Corporation Reforms;

- the Income Attribution Rules;

- a new taxation scheme for online sales by foreign based entities;

- certain measures related to commitments under the OECD's Base Erosion and Profit Shifting (BEPS) project.

In addition to the reforms discussed in further detail below, other reforms include:

- the retention of the current 8% consumption tax rate for food and drink purchases as well as newspaper subscriptions;

- the special extensions of certain tax benefits for SME's;

- the modification of special economic zones;

- the special provisions regarding securities and the exit tax;

- Transfer pricing; and

- the provisions relating to the Japan-Taiwan double taxation agreement (DTA).

These additional provisions are not covered in this article as they are beyond the scope of this discussion but will be discussed at a later date.

National corporate tax rate reduction

In keeping with its previously stated commitments to lower the corporate tax rate in Japan (historically one of the highest in the world) a corporate tax rate reduction was introduced which will be effected over a two-year period. The new rate effective from April 1, 2016 is 23.4%, down from the previous rate of 23.9%. The rate will also be reduced even further to 23.2% from 2018 onwards. This brings the rate more in line with that of other developed countries and is a significant reduction from the longstanding rate of over 40% which was in effect until 2012, when the government decided that reform of the rate was needed in order to stimulate the Japanese economy. It is hoped that these new lower rates will not only help to attract foreign investment into the country but also provide much needed tax relief for Japanese corporates.

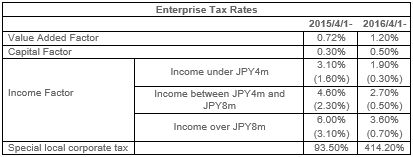

Modification of the enterprise tax and repeal of the special local corporation tax

The Enterprise Tax is a multi-layered tax on companies with a

capital base of more than JPY100 million (approximately

USD900,000). This tax is computed by taxing three different

components: a Value Added component, a Capital component, and an

Income component. Various rates of taxation are applied to each of

these components. The enterprise tax system was revised, under a

previous tax reform, by splitting the tax into two parts, the

corporate enterprise tax and a newly created 'special local

corporate tax'. This newly created tax was a measure introduced

to provide local governments with a portion of the proceeds from

the national enterprise tax.

Under the 2016 tax reforms, this special local corporate tax is to

be phased out during the 2016 tax year and will be abolished from

2017 onwards. Whilst this special tax will be abolished, the

enterprise tax will revert to its pre-modified format.

The rates in parentheses presented above are as a result of the special local corporate tax and have limited application.

Change in NOL limitations

Many countries, including Japan, have provisions for the utilization of net operating losses (NOL) in subsequent tax periods in order to offset taxable income in those periods. These NOL carry-forwards are often subject to limitations as to the percentage of income that may be offset and also to a limitation as to the number of years such losses can be carried forward. The new Japanese tax rules make an adjustment to the limitation rules on the use of NOL carry-forwards. The income offset limitation will be lowered incrementally over the next three years from the current rate of 65% to 60% from April 1, 2016, 55% from April 1, 2017, finally settling at a rate of 50% from April 1, 2018 and beyond. While this is a significant reduction in the previous NOL utilization limitation level of 80%, an offsetting extension of the NOL carry-forward period from nine to ten years will be implemented for tax years from April 1, 2018 onwards. This will effectively lead to more taxes being collected earlier and may result in a larger amount of NOLs expiring unutilized, even with the one-year additional carry-forward extension.

Corporate reorganization modifications

Japanese tax rules provide exemptions from tax for certain types

of corporate reorganization transactions. To qualify for tax-exempt

treatment, various requirements must be met as to the continuity of

management and shareholder identity, so as to prevent abuse of the

tax-free reorganization rules in transactions in which tax should

be recognized. The 2016 tax reforms relax the restrictions on the

resignation of specified directors and provide clarification around

the continuity of shareholding rules for certain types of mergers,

share splits and other share transfers.

As regards the continuity of management requirement for tax-exempt

share exchanges and transfers, the resignation of specified

directors will no longer disqualify the transaction from

tax-exemption so long as at least one director remains as a

director. Consequently, where the resignation of a director used to

be problematic in the share exchange/transfer context, now there is

more flexibility in the planning process since the resignation of

all but one director will not negatively impact the tax-exempt

nature of such transactions. Further, in transactions where a

parent company acquires subsidiary shares in a qualifying share

exchange or transfer, so long as the subsidiary has at least 50

shareholders prior to the acquisition, then such acquisition can be

valued at the most recent tax return's reported net asset value

plus an adjustment for capital acquired.

CFC (Anti-tax haven) revisions

Japan, like many other developed countries, has special rules to

prevent Japanese tax base erosion through the use of off-shore

related-party companies located in jurisdictions with lower tax

rates. The Japanese rules can be quite harsh and can result in

significant tax liabilities and are also complex and difficult to

apply in practice. The rules apply to related-party transactions

with certain types of entities and provide special exemptions from

classification in certain circumstances.

The 2016 tax reforms revise the exemption rules to include

insurance companies which are active in the Lloyd's market and

also to exempt intra-group transactions between related-party tax

haven entities as long as these entities are 100% owned, either

directly or indirectly, by the same Japanese parent company. This

effectively addresses the issue regarding Japanese taxation of

transactions that were in effect not abusive and did not result in

the reduction of the Japanese tax base.

An additional revision addresses the computation of foreign tax

credits associated with taxable income in the tax haven context and

specifically the application of the exempt foreign dividend rules.

Under these new rules the computation of foreign taxes available

for credit will be computed as follows:

Importantly, dividends which are exempt from the taxation on the CFC level are also excluded from the CFC's subsidiary income in the above calculation.

Income attribution rules

As part of the 2014 tax reforms, specific provisions were

enacted to address the issue of income attribution to permanent

establishments (PE). While these reforms were comprehensive,

special clarifications were required to support the adoption of the

new income attribution rules which came into effect from April 1,

2016. These clarifications specifically address issues raised in

the context of the computation of foreign tax credits and

utilization of NOL carry-forwards of a PE after a qualifying

merger.

The first of these clarifications focuses on the amount of foreign

income used in computing the foreign taxes available for credit

where a PE is allocated losses from a home based company. In cases

where the amount of income allocated to the PE directly from the

home based company is actually a loss (i.e., less than zero) then

the balance of the loss is used for foreign tax credit computation

purposes. However, in cases where the amount of income allocated to

the PE plus other foreign sourced income results in a loss, then

the loss is not taken account of in the foreign tax credit

computation and the income amount is instead simply zero. This

prevents the importing of foreign losses into the foreign tax

credit computation.

The second clarification applies in a narrow set of circumstances

whereby a previous Japanese PE's losses are effectively

reimported into Japan through a qualifying merger of two foreign

entities. For example, if foreign company A and foreign company B

each have PE's with NOL carry-forwards (foreign company A

having a current Japanese PE and foreign company B having a former

Japanese PE) then, by undergoing a qualifying merger, these two

companies can effectively reimport the losses of the former PE back

into Japan. These new rules eliminate the NOL's of the former

Japanese PE and limit the deductibility of NOLs to the extent of

the NOLs of the current Japanese PE only. This prevents the

importing of NOLs into the Japanese tax regime and the trafficking

in NOLs.

Taxation of online sales

Electronic (online) sales transactions have been a challenging

issue for countries throughout the world. How to determine the

source of the income and the incidence of taxation have been

particularly troublesome with the OECD even weighing in on the

subject as part of its Base Erosion and Profit Shifting (BEPS)

project. The Japanese tax system has historically considered and

defined the incidence of taxation for digital services to be either

the domicile or residence of an individual or in the case of

corporate service recipients, the location of the head office or

principal office. This has led to difficulties in taxing certain

B2B transactions where a foreign service provider provides a

digital service to a recipient PE located outside Japan but

belonging to a Japanese customer and where the service recipient is

the Japanese based PE of a foreign business customer.

The new rules amend the incidence of taxation determination and

provide that:

- where the recipient is a foreign (i.e., not Japanese) PE of a Japanese customer, the service will be considered a foreign supply of services and not taxable in Japan; and

- where the recipient is a Japanese PE of a foreign customer, the service will be considered as a domestic supply of services inside Japan and subject to Japanese taxation.

These new taxation rules will be effective from January 1, 2017.

BEPS adoption measures

Of course, no tax update is complete without considering the progress being made on the adoption of BEPS and any measures related thereto being adopted by the respective participating governments. Japan has fully committed to the BEPS project and has begun to implement the procedures and legislation required to progress the program in Japan. The Japanese transfer pricing rules are being modified to require MNEs to prepare the three types of documentation required under BEPS, namely the Country-by-Country Report, the Master File and the Local File. The first of these two will be mandatory from fiscal year 2016 onwards with the latter, the Local File, being mandatory from 2017 (tax year 2018) onwards. Whilst a discussion of the requirements of each of these reports is beyond the scope of this update, MNEs should make themselves aware of the requirements and implement documentation production and maintenance procedures accordingly.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]