- in United Arab Emirates

- within Law Practice Management topic(s)

- with readers working within the Aerospace & Defence industries

Understanding UAE corporate tax and transfer pricing framework

In recent years, the United Arab Emirates (UAE) has undergone significant developments in its fiscal landscape, most notably with the introduction of a Corporate Tax (CT) regime1. This landmark decision highlights the UAE's proactive approach to aligning with international standards while promoting sustainable economic growth and diversification.

On 3 October 2022, the UAE solidified its commitment to global tax transparency and fiscal responsibility through the issuance of Federal Decree-Law No. 47 of 20222 on the Taxation of Corporations and Businesses (UAE CT Law). This law officially established a CT and Transfer Pricing (TP) regime in the UAE. Subsequently, on 23 October 20233, the Federal Tax Authority (FTA) released the TP Guide, broadly aligning the UAE TP provisions with the Organisation for Economic Cooperation's (OECD) TP Guidelines for Multinationals and Tax Administrations.

This article focuses on defining related parties and connected persons transactions, with an emphasis on the nuances unique to the UAE.

Identifying related partiesunder UAE transfer pricing rules

As a first step, taxpayers must identify their related parties based on the definitions provided in Article 35 of the UAE CT Law, further elaborated in the UAE TP Guidelines. It's crucial to note that the definition of related parties differs between the UAE TP rules and the criteria outlined in the International Accounting Standards (IAS) 24 —Related Party Disclosures. Notably, discrepancies exist in how related parties are identified and treated across these frameworks. Therefore, businesses operating in the UAE should conduct a comprehensive review to determine their related parties according to the UAE TP rules. They should not rely solely on related party disclosures in their financial statements or the definitions used in their global TP policies.

Defining controlin UAE transfer pricing rules

Control, as defined in the UAE TP Rules, is the ability of a person to:

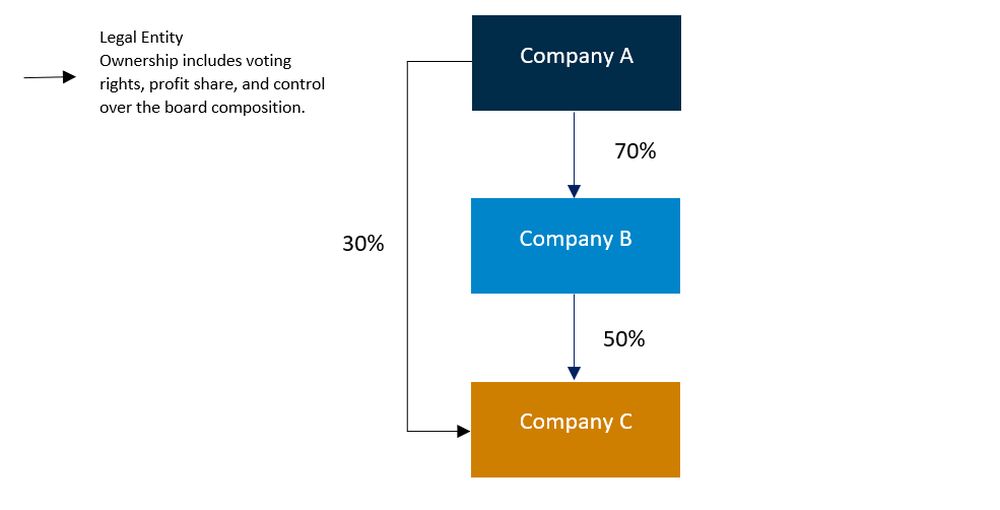

We have provided an example on what may constitute related parties under the UAE CT Law:

As per the above figure:

- Company A and Company B are related due to Company A's majority ownership in Company B.

- Company A and Company C are related due to i) Company A's indirect ownership of Company C through Company B of 35 percent (70 percent x 50 percent) plus ii) Company A's direct ownership of Company C of 30 percent, which equates to a total ownership interest of 65 percent (greater than 50 percent).

- Company B and Company C are related as both are related parties to Company A.

Key criteria for defining connected persons in UAE tax law

The UAE TP rules also apply to payments and benefits provided by taxable entities to connected persons.

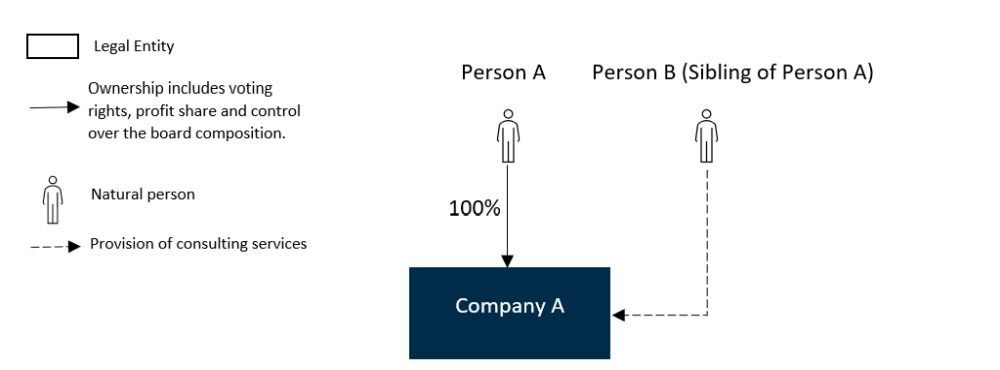

This limitation does not apply to companies listed on a Recognised Stock Exchange or Taxable Persons regulated by a competent authority in the UAE. An example of connected persons under the UAE CT Law is provided below:

As per the above figure:

- Person A is the sole shareholder of Company A, and considered a connected person to Company A.

- Person A and B are considered related parties as per the UAE CT law because they are relatives within the fourth degree of kinship.

- Person B provides consulting services to Company A.

- Person B qualifies as a connected person to Company A because they are a related party to Person A (i.e., the owner of the business/connected person of Company A).

- Payments from Company A to Person B for consulting services are classified as connected person payments and subject to UAE TP rules.

What are the tax deductibility criteria for related party and connected person payments?

To be eligible for tax deductibility, payments or benefits provided by a taxable entity to a related party or connected person must:

- Meet the arm's length standard.

- Be exclusively and wholly related to business activities.

Additionally, the expenditure must not be capital in nature. Specific deductibility rules also apply to certain categories of expenditure, such as private pension contributions.

The definition of payments or benefits is broad and may include, but is not limited to:

- Salary or bonus for employment, whether paid directly or through share plans.

- Employer contributions to a private pension fund.

- Interest on loans.

- Accommodation, education, and other benefits, either as payments or in-kind contributions.

- Other payments or allowances directly related to employment.

Failure to comply with these rules may result in the deduction being denied for UAE corporate tax purposes, increasing the taxable base of the taxable person. Furthermore, depending on the tax profile of the natural person, these payments may also be taxed in the hands of the recipient, potentially leading to double taxation. Lastly, failing to identify related party or connected person transactions may result in incomplete corporate tax returns or transfer pricing documentation.

Why should UAE businesses develop effective compensation policies?

Developing comprehensive reward and compensation policies is crucial for ensuring that payments made to connected persons adhere to the arm's length standard.

UAE businesses should:

- Establish these policies for key management personnel and directors.

- Ensure that the policies are consistently applied across the entire organisation.

- Regularly review and update the policies to align with market standards and business performance, ensuring that payments to connected persons are conducted at market value.

Key steps involved in this process include:

- Conducting periodic assessments to ensure compensation packages are in line with industry benchmarks and reflect the true value of services rendered.

- Maintaining transparency in the decision-making process.

- Documenting the rationale behind compensation decisions to strengthen compliance efforts and mitigate potential challenges from the FTA, especially regarding the denial of tax deductibility for such payments.

It's important to note that the connected person rules are specific to the UAE, therefore it's highly recommended to conduct a local review of compensation policies.

How can our TP and People Services teams help you determine arm's length payments to connected persons?

It is important to ascertain that any payments made to connected persons are on an arm's-length basis. At A&M, we work closely with our clients to ensure a robust filing position regarding payments made to connected persons, thereby minimising the risk of scrutiny by the FTA.

Our services typically include:

- Reviews of rewards and compensation policies

- Assessments of internal controls and processes to ensure compliance.

For UAE businesses that do not have a reward and compensation policy in place, we can help establish and implement a reward framework based on best practices.

This framework ensures that:

- Payments made to key management personnel and directors are aligned with established business policies and market practices.

- The payments are supported by contemporaneous TP defence documentation, as well as strong controls and processes.

Staying compliant with the UAE's corporate tax and transfer pricing rules can be complex, but it's essential to avoid penalties and secure tax benefits. By clearly defining related parties and connected persons, and setting up effective compensation policies, your business can stay on track.

Footnotes

1. Corporate Tax FAQ – Ministry of Finance – United Arab Emirates (mof.gov.ae)

2. Federal-Decree-Law-No.-47-of-2022-EN.pdf (mof.gov.ae)

3. Federal Tax Authority - Transfer Pricing Guide

Originally published by 17 October, 2024

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.