Overview

1. Income Tax

1.1. General Aspects

1.1.1. Income Tax Rate.

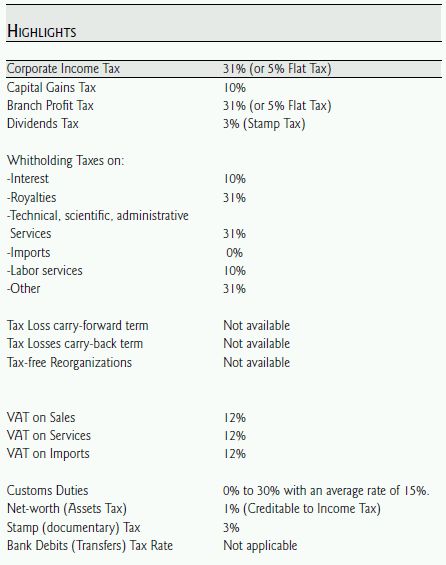

The general statutory corporate income tax rate is a flat rate of 5% on gross income minus exempt income; alternatively, there is the 31% corporate income tax rate on net income. This is equally applicable to local branches of foreign corporations.

1.1.2. Taxable Base

Refer to 1.1.1 above.

1.1.3. Deductions

There are no deductions applicable to the 5% Regime; for the 31% Regime, as a general rule, all costs and expenses related and necessary to the income producing activity, are considered deductible expenses. Excluded and/or exempted items of income are not deductible, and the lack of appropriate apportionment could lead to a proportional rejection on overall deductible costs and expenses. Some costs and expenses are limited to quantitative ceilings; e.g., royalties, unrecoverable debts, interest payments.

1.1.4. Depreciations

For the 31% Regime, tangible and intangible fixed assets´ depreciation is deductible. Depreciation term varies depending on the nature of the assets.

1.1.5. Transfer Pricing

Guatemalan legislation does not contemplate specific Transfer Pricing rules; however, this is not equivalent to say that the taxpayer is basically free to assign any value to transactions entered into with related entities. At the limit, the deliberate simulation of transactions with the purpose to evade taxes partially or totally is specifically sanctioned by criminal law.

1.1.6. Inflation Adjustments

Guatemala does not have inflation adjustments mechanisms; however, the revaluation of tangible or intangible assets is permitted.

1.2. Payment and Filing For tax payers under the 31% Regime, ordinary tax year covers the period from January 1st . to December 31st, with an annual filing deadline three months after the closing of the corresponding Tax Year. Tax payers under the 5% regime must file their returns on a monthly basis.

1.3. Interest and Penalties on Unpaid Tax or Tax Paid Belatedly

Unpaid taxes are subject to an interest charge that shall be assessed at the legal rate, roughly the average of the lending interests charged by banks, plus a fine that, subject to some qualifications, may be up to 100% of the unpaid taxes. Late payments (where no inspection has taken place yet) are subject to a fine calculated by multiplying the unpaid tax times the number of days of delay by a factor of 0.0005.

1.4. Dividend Tax /Branch Profits Tax

Although characterized as a Stamp Tax, for every practical purpose and except under certain circumstances (still debated at the Tax Court level) a 3% charge is levied on the dividends paid to both residents and non resident shareholders, as well as on the remittances made to Parent Corporation of local branches.

1.5. Cross-Border Payments

1.5.1. Withholding Taxes

When Guatemalan sourced income is remitted abroad to a beneficiary that is a nondomiciled alien individual or entity, the payment is subject to a withholding tax.

1.5.1.1. Royalties

Royalty payments are subject to a 31% withholding tax.

1.5.1.2. Dividends

Guatemalan law does not tax dividends or profits remitted abroad to foreign companies or foreign shareholders, provided that income tax has been paid in Guatemala by the local company at corporate level.

1.5.1.3. Technical, Administrative, Scientific, Financial or Economical Services.

Payments made to non-resident alien entities for technical, administrative, scientific, financial or economical Services are subject to a 31% withholding tax.

1.5.1.4. Other

Cross-border payments.

Other payments not specifically characterized, to non-resident alien entities or individuals are subject to a 31% withholding tax.

1.5.1.5. Interest payments.

Interest payments are subject to a 10% withholding tax rate; when interests are paid to a non-domiciled first order bank or financial institution, the proceeds of the loan are sold to the Guatemalan banking system and used to generate taxable income, there is no withholding obligation.

1.5.1.6. Equity Reimbursements

Although tax liabilities may arise within this context, they would not be subject to withholding obligations.

1.5.1.7. Tax Havens

Guatemalan tax regulations do not have Tax Havens provisions.

2. Value Added Tax (VAT)

2.1. General Aspects

2.1.1. VAT´s general rate is 12%. There is as reduced rate for minor tax payers (roughly under US$9,000.00 yearly income) of 5%. There are also some VAT exemptions for specific entities.

2.1.2. Taxable Transactions

The taxable transactions are the sale of movable assets and real estate property; imports; leasing of movable assets or real estate property; donations; inventory's consumption, losses or destruction, and services rendered in Guatemala.

2.1.3. Taxable Base

As a general rule, the taxable base is the price or value of the consideration paid for the goods or services. There are cases where certain items must be either included or excluded.

2.1.4. Creditable VAT

As a general rule the VAT taxpayer is entitled to credit to the VAT payable all such VAT paid to its suppliers for tangible movable assets brought or imported and for services hired, provided that they constitute a cost or expense of the taxpayer's income producing activity. The VAT paid in the acquisition of goods that will become fixed assets for the buyer is creditable to VAT account.

2.2. Payment and Filing

VAT has a one-month taxable period. Therefore, the tax must be assessed and a VAT return filed monthly. The VAT return must be filed and paid in full on the filing date, 30 days after the closing of the monthly period.

3. Other Taxes

3.1. Property Taxes

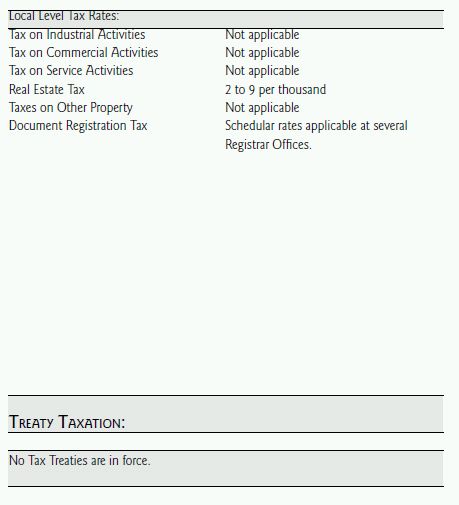

There is a Real Estate Tax paid on a quarterly basis. The tax rate ranges from 2 to 9 per thousand a year, calculated on a fiscal basis which can be appraised according to different procedures contained in the law.

3.2. Stamp Tax

This is a documentary tax applicable to all written agreements, with the exception of dividends or profits, which are levied with the 3% rate, regardless of the existence of a physical document; the Stamp Tax has fixed rates for some specific documents and agreements; for documents which are not subject to a fixed rate, there is a general tax rate of 3%. The taxable base is the full amount of the consideration agreed in the document. The general exemption for this tax is that all transactions subject to VAT, are not levied with the Stamp Tax.

3.3. Excise Taxes

In Guatemala, there are several excise taxes that apply to the consumption of national or imported goods such as cigarettes, alcoholic beverages and soft drinks. Tax rates range from 8% to 100%.

3.4. Custom Duties

In addition to import VAT, imports are also subject to custom duties that range between 0% and 30%; for most goods, the average rate is 15%. There is also the application of zero rating to certain goods in the context of Free Trade Treaties. Custom duties are computed on the CIF value of the goods, while import VAT is computed on the CIF value plus the corresponding custom duties.

3.4.1. Filling and Payment

An import tax return must be filed upon nationalization of the goods, and all import procedures must be preformed through an authorized customs agent.

4. Payroll Taxes /Welfare Contributions

4.1. Social Security System

The Guatemalan Social Security Institute manages and operates the Social Security System and the National Health System. These systems provide services and benefits related to illness treatment, disability and pensions system, old age, and maternity, death insurance. Social Security contributions are applicable to employer and employees. The contributions are based on the monthly salaries with a 12.67% for the employer and a 4.83% for the employee.

4.2. Labor Risks Insurance

This mandatory insurance is covered under the state owned monopoly of the Guatemalan Social Security Institute, and covers all the labor force.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.