Footnotes

1 Dividends and profits distributed by local branches are not subject to tax in Dominican Republic when branches have paid their corporate income tax on their Dominican Source income.

2 10% will apply when interests are paid to financial institutions. When interests are paid to non-financial institutions, the applicable withholding tax rate is of 25%.

3 In order to establish transfer pricing between related entities, the Dominican source income of branches or other forms of permanent establishments of foreign companies operating in the country will be determined based on actual results obtained from their operations in the Dominican Republic.

4 Goods subject to excise taxes are: leaded and unleaded fuel (16% ad-valorem tax); cigarettes (specific amounts of RD$29.59- RD$14.79 per cigarettes and a 20% ad-valorem tax), alcoholic beverages (specific amounts of RD$389.43- RD$317.59 per liter and a 7.5% ad-valorem), telecommunications (10%); insurances (16%) except if they fall under Law 187-01; electronic items (10-20%); among others

5 A tax of RD$1.50 per every thousand pesos (RD$1,000.00) is levied on the values of all checks or wire transfers.

6 This rate applies on the total value of the assets, including real estate properties as reflected in the tax payers' balance sheet, not adjusted by inflation and after applying the deduction for depreciation, amortization and reserves for non-collectable accounts. It will be excluded from the taxable base of this tax stock investments made in other companies, land located in rural areas, fixtures on agricultural exploitation and advance taxes.

7 Reference is made to the most usual rates, but other rates may be applicable.

1. Income Tax

1.1 General Aspects

1.1.1 Income Tax Rate.

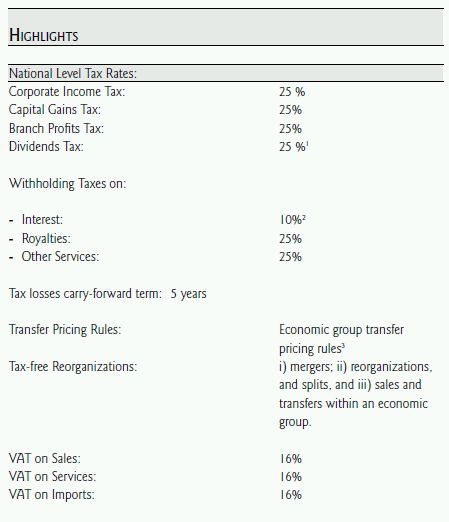

The general statutory corporate income tax rate for entities incorporated in the Dominican Republic, branches or permanent establishments of foreign companies is 25%.

1.1.2 Taxable Base.

All Dominican source income is subject to income tax unless the result is the Gross Income from which all expenses incurred in obtaining taxable income are deducted. The after-deductions result is the Net Taxable Income. The Net Taxable Income is the tax base from which the 25% corporate tax rate is applied. The result of applying the 25% tax rate is the Resulting Income Tax from which applicable Tax Credits are subtracted to find the Income Tax Liability.

[+] Sum of All Revenues

[=] Gross Income

[–] Deductible Expenses

[–] Exempted Items of Income

[=] Net Taxable Income (Minimum Presumptive Income Tax)

[=] Taxable Base [*] 25% Corporate Tax Rate

[=] Resulting Income Tax

[–] Tax Credits

[=] Income Tax Liability

[=] Income Tax Charge Payable

1.1.3 Deductions.

As a general rule all costs and expenses incurred in obtaining taxable income may be deducted, including interests, taxes (other than income tax, donation and inheritance tax, all taxes, rates or rights involved in the acquisition, maintenance and conserving capital goods, unless they have been allocated as part of the acquisition cost of such goods), insurance premiums, amongst others. The Dominican Tax Code establishes that deductions made by permanent establishments by payments of interests, royalties and technical assistance made to their foreign controlling entities will not be deductible if they have not paid the 25% withholding on the gross payment made. Expenses are generally allocated to the fiscal year in which they accrue.

The Dominican Tax Code allows for the deduction of the following concepts:

Interest on debts and expenses incurred through their constitution, renewal or cancellation, provided that they are directly related to the business and are involved in the acquisition, maintenance and/or operations of goods producing taxed income. Independently, interest on the financing of imports and loans obtained abroad shall be deductible only if the corresponding withholdings are effectively made and paid.

Taxes and rates levied on goods that produce taxed income, except income tax and its surcharges, as well as the taxes, rates and rights incurred in acquiring, maintaining and conserving capital assets, such as the Tax on Inheritances and Donations, contributions to public works that benefit private property and other taxes levied on capital income, or any other, except when the same are calculated as part of the cost transferring the asset in question.

Extraordinary damages suffered by goods that produce profits as a result of accidental causes, force majeure, or offenses by third parties shall be considered losses, but these must be reduced up to the amount of the value received by the taxpayer because of insurance or indemnification. If such value is superior to the amount of the suffered damages, the difference constitutes gross income subject to tax.

Insurance premiums that cover risks on goods that produce profits.

Depletion. In the case of the exploitation of a mineral deposit, including any gas or petroleum well, all the costs concerning exploration and development, as well as the interest attributable to it, must be added to the capital account. The amount deductible as depreciation for the fiscal year shall be determined through the application of the Unit of Production method to the capital account for the deposit.

Amortization of Intangible Assets. The depletion of the monetary cost of each intangible asset, including patents, copyrights, drawings, models, contracts and franchises whose life has a defined limit, must reflect the life of said asset and the method of recovery in a straight line.

Non-collectible Accounts. Losses arising from bad credit, in justifiable amounts, or in amounts separated to create a reserve fund for bad accounts.

Donations to Public Institutions of Public Good.

Investigation and Experimental Expenses.

Losses.

Contributions to Pension and Retirement Plans.

Individual taxpayers, except those who are salaried, that carry out activities distinct from the business, have the right to deduct from the gross income of such activities the verified expenses necessary to obtain, maintain and conserve taxed income.

1.1.4 Depreciation.

For the purposes of the DR Tax code, the concept of depreciable assets means the assets used in a business that loses value due to wear and tear, deterioration or disuse.

The amount allowed in a fiscal year for deduction for depreciation of any category of assets shall be determined by applying to an asset account, at the close of the fiscal year, the percentage applicable to such category of assets.

Depreciable assets must fall in one of the following categories:

Category 1. Buildings and other structural components used to generate taxable income may be deducted at a 5% annual rate will be calculated by applying the depreciation coefficient to the depreciable base of each asset individually.

Category 2. Automobiles and light trucks for common usage; office equipment and furniture; computers, information systems and data processing equipment may be deducted at a 25% annual rate over the acquisition or construction cost of such assets, minus the ITBIS that has been paid in the acquisition of a business.

Category 3. Any other depreciable assets may be deducted at a 15% annual rate over the acquisition or construction cost of such assets, minus the ITBIS that has been paid in the acquisition of a business.

Category 2 and Category 3 assets will be registered in a joint account and the depreciation will be calculated by multiplying the depreciation coefficient to the depreciable base of its joint account.

The initial addition to an asset account for the acquisition of any asset shall be its cost plus insurance, freight and installation expenses. The initial addition to an asset account for an asset of one's own construction shall include all taxes, charges, including customs duties and interest attributable to such asset for periods prior to its placement into service.

Amortization of intangible assets is permitted by the depletion of the monetary cost of each intangible asset, including patents, copyrights, drawings, models, contracts and franchises whose life has a defined limit, but it must reflect the life of said asset and the method of recovery in a straight line.

At the taxpayer's option, organization costs may be deducted either in the year in which they are incurred or capitalized, or amortized over a period not exceeding five years.

1.1.5 Transfer Pricing.

The Dominican Republic has transfer pricing rules applicable to transactions with related companies. The general principle is that when legal acts between a local enterprise of foreign capital and a natural person or legal entity domiciled abroad that directly or indirectly controls it shall be considered to be, in principle, made between independent parties when their provisions adhere to normal market practices between independent entities.

In order to establish the transfer pricing for related entities, the Dominican source income of branches and other forms of permanent establishments of foreign entities that operate in the country will be determined over the basis of the real results obtained for their operations in the country.

When the accounting elements of such enterprises do not reveal the real results that were obtained by their operations in the country, the tax authorities may determine the taxable income applying to the gross income received by the permanent establishment in the country, the proportion that exists between the total revenue of the controlling entity and the gross income of the establishment in the country. The tax authorities may also set the taxable income with the proportion that exists between the total revenue of the controlling entity, the proportion that exists between the total revenue of the controlling entity and the total assets of the latter.

When the prices that the branch or permanent establishment collects to its parent company or to other branch or related entity of the parent company do not relate to the values that for similar operations it is collected to independent entities, the Tax Administration may challenge the same. Such payments must be necessary to maintain and preserve the income of a permanent establishment in the country.

The tax authorities may challenge as an unnecessary expense to produce and maintain taxable income, the excess determined by the amount due and paid by interests, commissions, and any other payment, that results from credit or financial operations made with the parent or entity related to the same.

1.1.6 Inflationary Adjustments.

The Executive Power shall order an adjustment for inflation for each calendar year on the basis of the methodology established in the Regulations which is based on the Consumer Price Index of the Central Bank of the Dominican Republic.

- The adjustment ordered for any fiscal year shall be applied to

the following concepts determined as of the closure of the

preceding fiscal year:

- The steps in the tax scale for personal income tax;

- Any other amount expressed in Dominican currency ("RD$");

- Up to the limit set forth in the Regulations, any net participation in the capital of a business or in any capital asset not related to business;

- The transfer to future periods of the net losses for operations and of dividend accounts;

- The credit for taxes paid abroad; and,

- The nontaxable minimum established for individuals.

- The Regulations shall include:

- Regulations that describe how, in the case of businesses, the amount of the adjustment set forth in clause (a) shall be distributed among all the assets in the balance sheet of business, with the exclusion of cash, accounts receivable and stocks and bonds;

- Provisions for rounding-off the adjusted amounts up to the appropriate limit in order to efficiently administer the taxes; and

- Provisions that contemplate interim annual adjustments for the calculation of reserves for taxes, insufficient payments and payments in excess, undue payments, amounts paid through retention of an estimated tax and similar matters in which it is necessary to make said adjustments in order to carry out the goals of this Article.

- The Executive Power, if necessary, may establish adjustments with respect toinflation in other matters that affect the assessment of taxable income or the payment of taxes.

1.1.7 Tax Loss Carry-forward.

The Dominican Republic taxpayers may carry-forward tax losses for a maximum term of 5 fiscal years in accordance to the following rules:

- In no case in the current or future tax period, losses will be deductible from other entities in which the taxpayer has made a reorganization process nor losses generated from non deductible expenses.

- The enterprises may only deduct their losses of twenty percent (20%) of the total amount of such losses per year. In the fourth (4) year, this twenty percent (20%) will be deductible only to a maximum of eighty percent (80%) of the net taxable income related to such fiscal period. In the fifth (5) year, the maximum amount is of seventy percent (70%) of the net taxable income. The twenty percent (20%) portion of losses not deducted in a year cannot be deducted in further years nor will it trigger any reimbursement by the Dominican State. The deductions can only be made when filing the income tax returns.

The enterprises that in their first fiscal year present losses in their first income tax return will be exempted from this rule. The losses generated in their first fiscal year may be offset against 100% of their income in the second fiscal year. In the event that such losses could not be fully offset, the remaining credit will be offset following the deduction procedure explained herein. There is no carry-back possibility.

Losses arising from the sale or disposal of stock or shares may only be computed against capital gains of the same nature.

Tax losses cannot be transferred to other taxpayers.

The Dominican Republic Tax Code allows for three types of tax-free reorganizations:

- Tax-free mergers, preexisting through a third one that forms, or by the absorption of one of them;

- Tax-free split or division of an enterprise into others that jointly continue with the operations of the first, and,

- Sales or transfers within an economic group.

1.1.8 Tax-Free Reorganizations.

In order to qualify for a tax free merger, requirements are as follows:

- Approval of the local IRS office of the reorganization: All transfers of rights and obligations are subject to the prior approval of the local IRS office. The non-compliances of the formal duties of the entities whose reorganization results in their dissolution, whether by merger, splits, take over, sales or equity transfers, will be assumed by the surviving entity for the period the statute of limitations that have not yet elapsed and will be liable of any sanctions for the infractions made by the predecessor company.

- Dissolution of the absorbed entity: The mergers, acquisitions, sale or transfer of equity from one enterprise to another, leads to the closing of activities of the absorbed entity and obligates such company to make a final income tax return within sixty (60) days after the closing of its activities.

- Compliance with the Commerce Code requirements: the publication and registration requirements set forth in the Commerce Code, Law 3-02 of the Mercantile Registry, and Law 479-08 regarding Commercial Companies and Individual Limited Liability Companies must be observed.

1.1.9 Leasing Tax Treatment.

The leasing of moveable or immovable assets directly affects the corporate income tax and the Tax on the Transfer of Industrialized Goods and Services (ITBIS) of individuals and corporations.

For the leasing of assets, the rent payments will be treated as deductible expenses to the lessee's income tax, but for financial leasing such payments will be deducted provided that they are not considered to be capital amortization to the assets granted in lease.

If the payment of the lease is made to an individual (the landlord), the rent payment will be subject to a 10% withholding over the amount paid as rent and it will be considered to be a payment on account. Enterprises or corporations are not subject to any withholding when receiving rent payments.

For the landlord is a corporation, the leased asset will be considered to be part of the corporation's tax equity at the end of the operational period subject to inflation adjustments and depreciations, and consequently, affect the income tax to be paid.

To determine tax equity and further apply the inflation adjustments, the following steps must be followed:

- The financial leasing company must omit from its assets, the accounts receivables for capital settlements insofar as the company is allowed to deduct expenses for depreciation of assets granted in lease;

- The company that receives the assets in lease must omit from its liabilities (i) the accounts payable for capital settlements, and (ii) the fixed assets received in lease.

The payments made for the lease of moveable and immovable property are levied with a 16% tax rate for ITBIS applied over the lease price. If the landlord is a natural person or individual and the lessee is a corporation, the latter must withhold the 100% ITBIS amount to be paid and file the same before the local IRS. Rent of housing for personal use is exempted from the payment of ITBIS.

In the case of lease of moveable assets between entities, the paying entity is required to withhold 30% of the ITBIS to be paid.

1.2 Foreign Exchange Gains and Losses.

With respect to the application of income tax, our tax regime considers that foreign exchange gains or losses not made at the end of the fiscal year, derived from adjustments to the exchange rates over the currencies of the corporation or obligations in foreign currency, will be considered as taxable income for tax purposes or as deductible expenses depending on each particular case. To that effect, the referred exchange rate adjustments will be made in accordance to the exchange rate index published by the tax administration.

The entries subject to these readjustments are a) all asset entries in foreign currency which are permanent in the country or abroad. In this case, entries such as cash in foreign currency, account receivable entries, titles, rights, certificates, deposits and investments made in foreign currency must be adjusted; and b) all liabilities in foreign currency. The exchange adjustments to the assets in foreign currency must be made against an income-statement account "Exchange Rate Results", while the exchange rate adjustments to the liabilities in foreign currency must be made against each corresponding asset, if applicable, or against the income-statement account "Exchange Rate Result". The income-statement account will be considered for the Profit & Loss Statement and also for tax purposes.

1.3 Payment and Filing.

All enterprises or corporations incorporated in the country or abroad domiciled in the country that obtain Dominican source income and/or foreign source income from investments and financial earnings, will be obligated to file an income tax return within 120 days after the closing of the fiscal year.

The individuals or persons, including those that operate business with or without organized accounting and the other physical persons, domiciled or not in the country, taxpayers of Dominican Source income and for foreign income of investments and foreign earnings, must file annually before the tax administration a income tax return of the previous fiscal year, and pay the tax no later than March 31st of each year.

No later than March 15th of each year, the corporations or entities that act as employers shall file separately their income tax declaration on the taxes withheld and paid on the previous calendar year for the wages paid to its employees as well as the independent staff that rendered work or services.

1.4 Penalties on Unpaid Tax or Tax Paid Belatedly.

The Dominican Tax Code sets forth certain penalties for incompliance with formal requirements and for incompliance with material obligations.

Penalties for incompliance with formal requirements, are imposed on the following infractions:

- omitting presentation of tax declarations within the set period is penalized with a surcharge of 10% of the first month and an additional 4% of each month or fraction thereof, interests of 1.73% per each subsequent month or fraction of a month, and fine of five (5) to thirty (30) minimum salaries (a minimum salary is equal to approximately US$207.00 dollars). In addition to this fine, a sanction of 0.25% of the income declared in the previous fiscal year may be imposed on the taxpayer. However, the surcharges, interests and fines may be reduced up to 40% if the taxpayer voluntarily pays the due tax by rectifying its tax declarations prior to any requirement made by the tax administration and if no tax audit has been initiated for the tax or the corresponding fiscal period;

- close down of businesses, which may be applied on establishments, offices, for lacking registry books, for not registering determined goods or equipments, the delay in making the accounting registration after it has been required to do so, the destruction or hiding of goods, documents books and accounting records, among others.

Amongst penalties for incompliance with substantial obligations:

- Tax evasion: this is fined with a penalty of two (2) times the tax that has been omitted, notwithstanding the closure of the establishment. In the event that the amount of the tax evasion could not be determined, a fine will be set between ten (10) to fifty (50) minimum salaries;

- tax fraud: this is fined with a penalty from two (2) to ten (10) times the tax being evaded; the confiscation of the merchandise or products and the vehicles or other elements utilized for committing the fraud; closure of the establishment for a maximum period of 2 months; cancelation of the license, permits related to the activities performed by the taxpayer for a maximum period of 2 months. In the event of withholding or perception agents, this will be sanctioned with a penalty equal to the payment of two (2) to ten (10) times of the tax withheld or perceived after the expiration of the time limits in which they must remit them to the tax administration. When the amount of the tax fraud cannot be determined, the sanction will be from five (5) to thirty (30) minimum salaries. Imprisonment of 6 days to 2 years may apply in some circumstances.

The fine amounts may be reduced whenever the incompliance is not repeated and upon rectification or voluntary filing of the tax.

1.5 Dividends Tax / Branch Profits Tax.

Distribution of dividends by local entities or corporations of Dominican Source profits to natural persons or legal entities residing or domiciled in the country or abroad will be subject to 25 % withholding to be made and paid by the local entity or corporation making the distribution. However, the withholding made by the local entity or corporation shall constitute a tax credit against their corporate income tax for the fiscal year in which the withholding taxes take place. If during the fiscal year, the tax credit allowed to a legal entity exceeds the taxes of such legal entity for corporate income tax, said excess shall be transferred and shall be considered as a tax credit for the following year.

Repatriation of Dominican source profits made by branches to their foreign parent company is exempted from withholding tax.

1.6 Cross-border Payments

1.6.1 Withholding Taxes

Those who pay or credit on account taxable income from Dominican sources to persons neither residing nor domiciled in the country, which is not interest paid or credited on account to financial institutions from abroad, nor dividends, nor income to natural persons, must withhold and pay to the Administration, as sole and definitive payment of the tax, twenty five percent (25%) of such income.

The gross income paid or credited on account is understood to be, without admitting evidence to the contrary, net income subject to withholding, except when theDR Tax Code establishes the presumptions referring to obtained net income, in which case the tax base for the calculation of the withholding shall be this latter one.

1.6.1.1 Dividends.

See 1.5

1.6.1.2 Royalties.

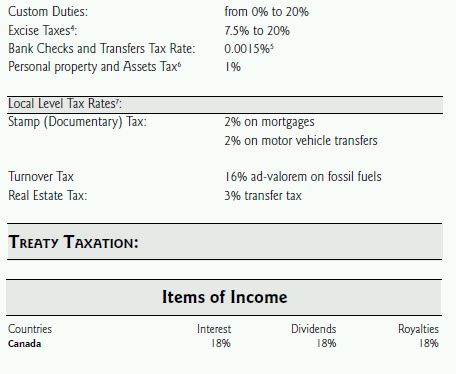

Royalty payments made to non domiciled companies or natural persons are subject to a 25% withholding tax. If the double taxation treaty with Canada applies, an 18% withholding will apply.

1.6.1.3 Technical Assistance, Engineering and Consulting Services.

Technical assistance, engineering and consulting services rendered by non domiciled corporations or natural persons are subject to a 25% withholding tax.

1.6.1.4 Interest on Loans obtained abroad.

Interest payments on loans obtained abroad are subject to a withholding rate of 10% on the interest paid if the beneficiary is a bank or financial institution incorporated in its jurisdiction. If the beneficiary of the loan is a not considered to be a financial institution in its jurisdiction, the withholding rate of 25% on the interest paid will apply.

1.6.1.5 Payments to non-residents:

Payments to non-residents working on a temporary basis in Dominican Republic will be subject to a 25% withholding tax on the gross income paid;

1.6.1.6 Rental Payments on moveable property:

are subject to a withholding rate of 10% when the beneficiary of the payment is a natural person. When the beneficiary is an entity or corporation, no withholding tax will apply;

1.6.1.7 Rental Payments on real estate property:

are subject to a withholding rate of 10% when the beneficiary of the payment is a natural person. When the beneficiary is an entity or corporation, no withholding tax will apply;

1.6.1.8 Proceeds from the sale of any type of property:

are subject to a 3% transfer tax and, if applicable, a capital gains tax of 25%. To determine the capital gain subject to tax, the acquisition or production cost adjusted by inflation shall be deducted from the price or value of the transfer of the asset.

When dealing with depreciable assets, the acquisition or production cost to be considered shall be their residual value, and on this the referenced adjustment shall be made.

1.6.1.9 Others:

The general withholding rate applicable to other cross-border payments not included within those mentioned above are subject to a general withholding rate of 25%.

2 Value Added Tax (VAT)

2.1 General Aspects

2.1.1 Tax Rates.

The VAT rate is of 16% which applies to all goods and services. There are also some VAT exemptions for specific public entities of the national or local territorial level, religious institutions, free zones, health services, financial services – including insurance -, pension and retirement plans, ground transportation for persons or freight, electricity, water and garbage disposal services, rent of housing for personal use and personal care services amongst others.

2.1.2 Taxable Transactions.

Transactions subject to VAT are the sale of goods, the provision of services in the Dominican Republic and the importation of goods. In some cases, services rendered outside the Dominican Republic are exempted from the payment of VAT. However, the tax authorities do not always accept this exemption.

2.1.3 Taxable Base.

The taxable base is the price or value of the consideration paid for the goods or services.

2.1.4 Creditable VAT .

As a general rule the VAT taxpayer has shall have the right to deduct from the gross tax the amounts that, by reason of this tax, have been advanced within the same tax period:

- To local suppliers for the acquisition of goods levied by this tax; and

- In customs, for the introduction into the country of goods levied by this tax.

2.2 Selected VAT Incentives.

Some entities or corporations under a special tax regime law are exempted from the payment of VAT:

2.2.1 Free Zones Entities under Law 8-90.

Free Zone entities are exempted from all taxes, including the payment of VAT for the importation of goods and services, and from the acquisition of goods or services.

2.2.2 Tourism Development Law 158-01.

Investments made on some tourism projects are exempted from the payment of VAT but limited to the machinery, equipment, materials and moveable assets that are necessary for the construction and for the initiation of operations of the tourism facilities.

2.2.3 Law 28-01 for Border Development.

Corporations and entities that install their operations in the border provinces with Haiti are exempted from the payment of VAT.

2.2.4 Renewable Energy Law 57-07.

Renewable energy projects are exempted from the payment of VAT.

2.2.5 Law 56-07 that declares as a national priority the textile, tailoring, accessories, leather, fabrication of leather footwear industries. Corporations and entities under this law are exempted from the payment of VAT.

2.2.6 Law 122-05 regarding non for profit organizations.

Non for profit organizations are exempted from the payment of VAT.

2.2.7 Law 19-00 regarding the Dominican Securities and Exchange Market.

The operations for the sale and purchase of Dominican securities approved by the Superintendence of Securities are exempted from the payment of VAT.

Other incentive laws grant selective tax incentives.

2.3 Payment and Filing

VAT returns must be filed within the first twenty (20) days of each month. In the case of definitive imports, the tax is determined and paid along with custom duties.

3 Other Taxes

3.1 Personal Property and Assets Tax

This is a 1% tax levying company assets which are included in the taxpayers' general ledger, not adjusted by inflation, after applying all deductions by depreciation, amortization, provisions for bad debts, investment in shares in other companies, land located in rural areas, properties affixed to rural production plants and advance taxes.

The financial intermediation entities or corporations defined by the Monetary and Financial Law. 183-02, The National Bank for Housing Development as defined by Law 6-04, The Pension Fund Administrators as defined by Law 87-01 which creates the Dominican Social Security System and the Pension Funds,, the stock market trading corporations, the investment funds managers and those equity issuing companies as defined in Law 19-00, as well as the electrical companies dedicated to generation, transmission and distribution, as defined by the General Electricity Law No. 125 -01, shall pay this tax on the basis of their total fixed assets, net of depreciation as it appears in their balance sheet.

The liquidated amount in respect of this tax, when applicable, shall be considered to be a tax credit against the corporate income tax corresponding to the same fiscal year. In the event that this liquidated amount equals or exceeds the assets tax to be paid, the payment obligation shall be considered extinguished. If after the payment is made, there is a difference to be paid, in the event that the assets tax exceeds the income tax, the taxpayer shall pay the difference in two equal installments, the first due within 120 days from the end of the fiscal year and the remaining balance within a term of six (6) months from the due date established for the first payment.

The following tax payers shall be exempted from this tax:

- The corporations that are exempted from Income Tax (IT);

- Those investments as defined by the local IRS as Intensive Capital Investment, meaning;

- Those investments that by the nature of its activities have an installation, production and operation cycle of more than 1 year;

- Taxpayers who are operating under the umbrella of a law that includes tax exemptions in connection to corporate income tax;

- The investments defined regularly by Tax Administration as intensive capital or the investments that by their nature have an installation, production and commencement of operations cycle exceeding one (1) year, performed by new or pre-incorporated companies, may benefit from a temporary exemption of this tax, after providing proof that their assets qualify as new or derive from an investment capital; and,

- Those tax payers that declare losses in their income tax returns may request a temporary exemption for the payment of Assets Tax.

The Assets Tax declaration must be filed along with the income tax return of the company and shall be paid in two equal installments: 50% at the date of filing of the declaration and the 50% remaining balance shall be paid six (6) months later. If an extension is granted by the local IRS in filing the income tax return, it will also extend the term to file the assets tax declaration.

For physical persons (resident or non-resident) a personal property tax is levied of 1% on the real estate properties that are destined for housing, commercial and industrial activities owned by individuals whose value – including the land – exceeds RD$5,000,000.00. This value is annually adjusted pursuant to local official inflation rates.

The personal property tax must be filed by the physical person during the first 60 days of each year and liquidated in two installments: (i) 50% of such tax on March 11 of each year; and (ii) the remaining balance of 50% on September 11 of each year.

3.2 Municipal Tax

Entities or corporations who privately use or utilize the soil, subsoil or public roads to exploit and supply services which affect all or some part of the municipality will be subject to pay a 3% municipal tax levied on their gross income generated from their annual invoices for each municipal term.

3.3 Stamp Taxes

A transfer tax levies the transfer of real estate property in the Dominican Republic. The tax rate is of 3% over the purchase price of the real estate property as set forth in the purchase and sale agreement or the value of the property assigned by the tax authorities, whichever is higher.

All other real estate operations (registration of mortgages, liens or encumbrances, among others) are subject to a 2% ad-valorem tax.

The transfer of motor vehicles is subject to a unified 2% ad-valorem tax rate applied over the value of the motor vehicle.

3.4. Bank Checks and Transfers Tax Rate

This tax is of RD$1.50 per thousand pesos on the values paid by checks or wiretransfers. Payments made to public entities such as the Social Security Treasury Department, the Tax Administration and the General Customs Department are exempted from the payment of such tax.

3.5. Selective Consumption Tax

The selective consumption tax levies all transfers of goods produced locally at the manufacturing level, as well as its importation or the rendering of local services. The applicable tax to these services is as follows:

- 1 0% on telecommunications;

- Specific amounts per liter of pure alcohol; and

- Specific amount per cigarettes packages.

The individuals, corporations, national or foreign companies that produce and manufacture these goods are obligated to pay these taxes at the last phase of the process, regardless of the fact that their intervention occurs through services rendered by third parties, importers of goods levied by this tax by their own account or by third parties, and the service providers levied by this tax.

The payment of this tax shall be made within the first 20 working days of the month following the declared fiscal period. Importers shall pay this tax along with any custom taxes.

Insurances are levied by this tax at a rate of 16%. Insurances set forth by Law 187- 01 are exempted. Electrical appliances are levied with a selective consumption tax between 20% and 10% respectively.

The products derived from tobacco and alcohols are levied with a selective consumption tax, which shall apply on the retail prices of such products. The rates are of 7.5% for the products derived from alcohol and 20% for products derived from tobacco. For the application of the foregoing taxes, the retail prices shall be determined by increasing the price lists without any discounts, gratuities, donations or other similar items, as follows:

- An increase of 30% for alcohol products;

- An increase of 20% for beer; and

- An increase of 10% for tobacco products.

The table of specific amounts to collect the Selective Consumption Tax to the products deriving from alcohol and tobacco are modified on an annual basis.

4 Customs Regime – General Aspects

4.1 Custom Duties

Importation of goods and are subject to import VAT at a rate of 16% plus custom duties that range between 0% to 20% depending on the type of asset imported, and except for assets with special treatment.

4.2 Taxable Base

As a member of the WTO and having subscribed the Agreement for the Application of Section VII of the GATT, the value of the goods is established on account of theprice paid. If this is not possible, other methods of valuation and the corresponding adjustments are applied. Duties are computed on the CIF value of the goods.

4.3. Transfer Pricing

See 1.1.5

4.4. Filing and Payment

An import return must be filed and the pertinent tax must be paid before the good is nationalized and cleared from customs.

4.5. Selected Custom Duties Regimes Available

There are several import regimes applicable in the Dominican Republic:

4.5.1. Ordinary Importation Regime.

It applies to all goods that will remain permanently in the Dominican Republic territory without any use or jurisdictional restrictions. Full payment of custom duties and import VAT is required upon nationalization.

4.5.2 Temporary Importation Regime.

It applies to merchandise that is to remain in the country for a specific purpose to be re-exported within a period of 90 days from the date of entry of such good in the Dominican Republic. This time period may be renewed for three (3) additional periods of ninety (90) days by request of the requested party which shall be renewed if the basis of this request is considered to be valid by the Customs Department.

The temporary importation regime benefits the following products: (a) professional equipment, including press and television, computer programs and cinematography and radio equipment necessary for the business activities, or profession of the business person that qualifies for the temporary entry of products in accordance to Foreign Investment Law 16-95; (b) merchandises used for exhibition or display; (c) commercial, movies and advertising samples; and (d) merchandises admitted for sporting events.

Several conditions must be met to import these merchandises to Dominican territory.

5 Payroll Taxes / Welfare Contributions

Employees are liable for both income tax and social security contributions to be withheld to their salaries as required by applicable law. Employers are also designated as withholding agents for tax and contribution purposes, thus subject to withhold income tax and said contributions to its employees and pay directly such taxes to the competent authorities. On the other hand, employers are liable for withholding their own employees' social security contributions. Both withholdings and contributions are collected and paid monthly on the basis of the gross remuneration.

5.1 Retirement Contributions

The employee's withholding for retirement funds equals to 2.87%, calculated on the employee's wage. Employers whose main activity is to hire or provide services must also contribute to the social security system for retirement funds in an amount equivalent to 7.10% of the monthly wage paid to the employee. The maximum wage applicable would be the equivalent of 20 minimum wages.

5.2 Health Contributions

The employee must be affiliated to a Family Health Insurance ("FHI"). Contributions to the FHI administering entity must be equal to 10.13% of the employee's wage, 7.09% of which is paid by the employer while the remaining 3.04% is contributed by the employee. The employer is responsible for withholding the employee's corresponding 3.04% and for paying the Treasury of the Social Security 100% of the monthly health contribution. The maximum wage applicable shall be the equivalent of 10 minimum wages.

5.3 Workers Compensation Insurance System

This insurance will be financed with an average contribution of one point twenty percent (1.20%) of the wages, totally covered by the employer. The total contribution from the employer will have two (2) components:

- A fixed base rate of one percent (1%) to be applied evenly to all employers; and

- A variable rate of up to zero point six percent (0.6%) established in agreement with the field of activity and risk factor of each enterprise. In both cases, said percentages shall be applied on the basis of the applicable wages.

The maximum contribution in this insurance is of four (4) wages.

5.4 Technical Professional Training Institute:

All companies are subject to the payment of a monthly contribution to INFOTEP (the governmental Institute of Technical Professional Training). This contribution is equivalent to 1% of the wage of the employee.

The employee must pay 0.50% of the annual bonuses received from the employer if the bonuses apply.

5.5 Payroll Taxes and Contributions

Payroll taxes and contributions in the Dominican Republic shall be made in accordance to the following chart:

Payroll Taxes

|

Annual Wages |

Rate |

|

Income until RD$349,326.00 |

Exempted |

|

Income from RD$349,326.01 to RD$523,988.00 |

15 % of the surplus of RD$349,32601 |

|

Income from RD$523,988.01 to RD$727,761.00 |

RD$26,199.00 plus 20% of the surplus of RD$523,988.01. |

|

Income from RD$727,761.01 and beyond |

RD$66,954.00 plus 25% of the surplus of RD$727,761.01 |

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.