- within Finance and Banking topic(s)

- with readers working within the Advertising & Public Relations and Retail & Leisure industries

- within Immigration, Insurance and Accounting and Audit topic(s)

Kenya has made a significant stride in reforming the capital markets licensing framework by enacting the Capital Markets (Licensing Requirements) (General) Regulations, 2025 (the “2025 Regulations”), repealing the Capital Markets (Licensing Requirements) (General) Regulations, 2002 (the “2002 Regulations”). The 2002 Regulations were developed for a market initially characterised by clearly delineated intermediaries, exchange-centric trading and limited technological intermediation. In contrast, the 2025 Regulations respond to a fundamentally different market environment shaped by digital distribution channels, automated advisory models and alternative trading systems, marking a shift from a rules-based, entity-focused regime to a more activity-based and supervisory-led framework. We set out below the key developments.

- Expansion of the regulatory perimeter

The 2025 Regulations expand the Capital Markets Authority (“CMA”) regulatory perimeter to capture digital platforms and new categories of market intermediaries. Alongside traditional categories, the 2025 Regulations introduce:

- Broker-dealers: a hybrid licence permitting a single entity to act as both stockbroker and dealer, as well as arranging the underwriting of securities issuances. This departs from the 2002 framework, which treated stockbroking and dealing as strictly separate functions, and allows market participants engaging in both agency and proprietary trading to operate under a single licence.

- Over the counter (“OTC”) platforms: digitally enabled trading systems facilitating the trading of listed or unlisted securities, commodities, currencies or other instruments directly between two parties without intermediation of a central exchange or broker.

- Intermediary Service Platform (“ISP”) Providers: digital platforms that aggregate, market and distribute capital markets products and services. However, the definition under the 2025 Regulations excludes platforms deployed by existing licensees solely for improving efficiency and crowdfunding platforms. ISP Providers must also enter into written agreements with licensed intermediaries and submit quarterly reports to the CMA.

- Robo-advisers: the definition of "investment adviser" expressly captures digital platforms providing automated, algorithm-driven investment advice with little to no human supervision. Additional requirements include maintaining a principal bank account in Kenya, adequate capital, secure systems and a robust data protection policy.

- Custodians: custodial services have been elevated to a standalone licensing category. A custodian must be a bank licensed by the Central Bank of Kenya or a licensed financial institution.

- Trustee: a unified licensing regime for trustees, bringing together note trustees appointed in respect of debt instruments and trustees of collective investment schemes.

- Recalibration of capital requirements

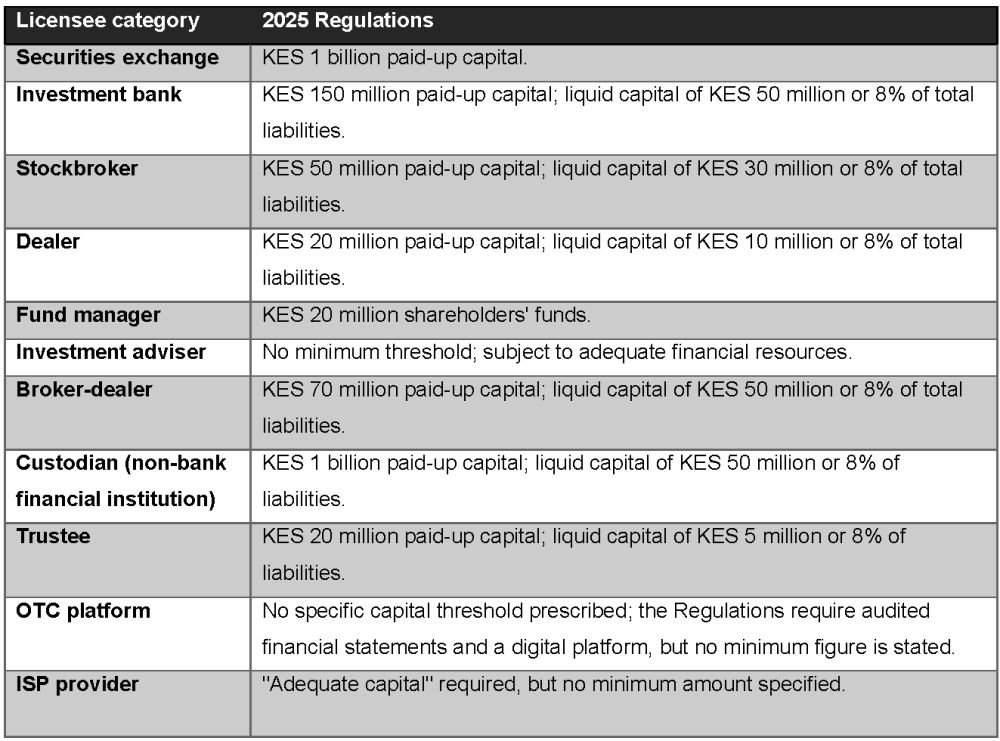

The 2025 Regulations recalibrate the minimum capital thresholds for a number of licensee categories as follows:

The recalibration reflects a targeted rebalancing of entry barriers. The reduction in the paid-up capital requirement for investment banks may make those activities more accessible, while the increased fund manager threshold imposes tighter prudential requirements, potentially driving recapitalisation or market consolidation.

- Expanded authorised functions of investment banks

The 2025 Regulations add market-making activities to the authorised functions of investment banks, expanding beyond the advisory, broking, dealing, underwriting and fund management functions permitted under the 2002 framework.

- Risk-based supervision and reporting

All market intermediaries must now submit monthly risk-based capital adequacy reports and management accounts to the CMA within 15 days of each month-end. Audited financial statements must be submitted within three months of each financial year-end, marking a shift from periodic reporting to continuous prudential supervision.

- Streamlined licensing process

The 2025 Regulations formalise an "approval in principle" mechanism, under which the CMA may grant preliminary approval to an applicant that substantially satisfies the prescribed requirements. This permits the applicant to establish operating facilities and recruit staff, but not to commence operations until the final licence is issued. An approval in principle is only valid for 6 months.

- Licence validity

A licence granted under the 2025 Regulations remains valid indefinitely, subject to ongoing compliance obligations and annual regulatory fees, unless suspended or revoked by the CMA. This replaces the annual renewal requirement under the 2002 Regulations.

- Enhanced fit and proper requirements

The 2025 Regulations expand the criteria for determining whether a person is "fit and proper" to hold a position as a director, chief executive officer or other key personnel of a market intermediary. The expanded criteria encompass probity, competence and soundness of judgement; past performance and expertise; technical knowledge and professional qualifications; and creditworthiness.

- Multi-licence regime

The 2025 Regulations expressly permit a licensee to apply for more than one licence.

- Securities exchange governance

Each securities exchange must be demutualised. Boards must include at least one-third independent and non-executive directors, with a maximum of two directors elected from trading participants. The chairperson's tenure is capped at 3 years and the chief executive officer's at 5 years, each renewable once.

- Transitional provisions

All licences issued under the 2002 Regulations remain valid. However, existing licensees must meet any additional requirements within 12 months of commencement, translating to 11 December 2026. Persons operating OTC platforms or ISPs that were previously unregulated must apply for a licence within the same period.

Conclusion

The 2025 Regulations represent a fundamental modernisation of Kenya's capital markets licensing framework. The expansion of the regulatory perimeter, the shift to risk-based supervision, enhanced governance standards and recalibrated capital thresholds will require significant adjustments from both existing licensees and newly captured market participants. We encourage all affected parties to conduct gap analyses and develop compliance roadmaps well in advance of the 11 December 2026 transitional deadline.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]