- with readers working within the Accounting & Consultancy, Banking & Credit and Retail & Leisure industries

- within Government, Public Sector and International Law topic(s)

The Jumpstart Our Business Startups Act, or the JOBS Act, significantly reduces regulation and the attendant cost of raising capital, conducting an IPO and related public company reporting obligations. These changes create many new opportunities for Canadian and other non-U.S. companies as well as U.S. companies. Canadian and non-U.S. companies can better access the U.S. capital markets either in an IPO or in stages and take advantage of the higher valuations and increased liquidity that come with U.S. capital market access for dually listed companies.

The JOBS Act enables non-U.S. issuers to access capital:

- through immediately effective changes to the offering process

for SEC registered IPOs and reduced SEC reporting obligations for

companies with less than $1 billion in gross revenues;

- by permitting broad publicity for private placements,

especially in traditional Reg. D/Rule 144A/Reg. S offerings;

- by providing a stripped down registration and reporting system

for companies raising capital of up to $50 million annually;

and

- by facilitating passive markets for trade execution as a

convenience for U.S. shareholders of non-U.S. companies.

This memorandum summarizes the key changes of the JOBS Act and emphasizes the implications of those changes and the new opportunities for Canadian and other non-U.S. issuers.

I. "Emerging Growth Companies": A New, Easier Path to an IPO with Reduced Burdens Thereafter

The JOBS Act establishes a new category of issuers – Emerging Growth Companies ("EGC"), which may take advantage of an easier IPO process and lesser disclosure requirements during and after registration with the SEC. An EGC is a U.S. or non-U.S. company with annual gross revenues of less than $1 billion during its most recently completed fiscal year.1 Most companies that recently conducted IPOs in the United States would have qualified as EGCs. Additionally, non-U.S. companies could register under the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act"), list their shares for trading in the United States and still qualify as an EGC. However, EGC status is not available to companies whose initial public offerings occurred on or before December 8, 2011. Consequently, existing public companies are not EGCs.

Non-U.S. companies can register under the Exchange Act, list their shares, for trading in the United States and still qualify as an EGC. A non-U.S. private issuer that qualifies as an EGC may take the advantage of the benefits available to EGCs to the extent those benefits apply to the form requirements for foreign private issuers.2 Similarly, Canadian issuers filing under the Multi-Jurisdictional Disclosure System (MJDS) can qualify as EGCs if they meet the requirements of the definition.3

EGC status and the related benefits are not permanent. An eligible company remains an EGC until the earliest of:

- the last day of the fiscal year during which its annual gross

revenues exceeds $1 billion;

- the last day of the fiscal year following the fifth anniversary

of its IPO of common equity in the United States;

- the date on which the issuer has issued more than $1 billion in

non-convertible debt during the prior three-year period; or

- the date on which it becomes a "large accelerated

filer" (i.e., when its public float is $700 million or

more).

An EGC that is a foreign private issuer could benefit from the concessions given to EGCs during the five-year phase-in period and when its EGC sales and related concessions expire, use the concessions available to Canadian and other non-U.S. issuers.

The following benefits are available to EGCs:

Reduced Financial Disclosure Requirements in IPOs. EGCs need only provide two years of audited financial statements in their IPO registration statements, instead of three years. Also, an EGC need not disclose in any periodic report or registration statement financial data for any period before the earliest audited period presented for the IPO.

No SOX 404(b) Auditor Attestation of Internal Controls. Like other public companies, EGCs must establish and maintain internal controls over financial reporting and provide a management's report on those controls. The CEO and CFO certifications of financial statements also remain. However, EGCs are exempt from providing an auditor's attestation report on internal control over financial reporting, which is required for public companies with a market float of $75 million or more under Section 404(b) of the Sarbanes-Oxley Act.

Deferred Compliance with New Accounting Rules and Exemption From Certain Auditing Requirements. EGCs using U.S. GAAP need not comply with any new or revised accounting standard until that standard applies to private companies, which is usually 1-2 years after the standard is imposed on public companies. EGCs need not comply with future PCAOB rules mandating auditor rotation or any supplement to the auditor's report in which the auditor must provide additional information about the audit and the financial statements of the issuer, in the auditor discussion and analysis section.

Reduced Executive Compensation Disclosure. As long as companies are EGCs and for three years after their IPO4, EGCs need not comply with the full SEC requirements for executive compensation disclosure. Specifically, EGCs need not (a) hold an advisory shareholder vote to approve the compensation of executives, (b) obtain shareholder approval for golden parachute compensation, and (c) disclose the ratio of CEO-to-worker compensation. EGCs may otherwise comply only with the compensation disclosure requirements for smaller reporting companies, under which a company (a) must disclose the compensation of three executive officers (rather than five) and a summary compensation table that covers two years (rather than three), and (b) need not include a compensation discussion and analysis (CD&A). Also, EGCs need not disclose the relationship between executive compensation actually paid and the financial performance of the issuer.

Advantages in Marketing and IPO Procedures for Research Reports. Broker-dealers may now publish research reports about an EGC before or after its IPO, without black-out periods, even if the broker-dealer is participating or will participate in the IPO.

Test-the-Water Marketing. An EGC may "test the waters" through oral or written communications with potential investors that are "qualified institutional buyers" ("QIBs") or institutions that are "accredited investors"5 to determine whether they may have an interest in the securities, either before or after the filing of a registration statement. These new "test-the-waters" provisions do not require the filing with the SEC of the materials used to solicit investor interest, which could result in the distribution of uneven information among investors, among other risks.

Confidential Submission. An EGC may confidentially submit to a draft registration statement for confidential review by the Staff of the SEC before making a public filing, provided that the initial confidential submission and all amendments are publicly filed with the SEC no later than 21 days before the start of road show. Recently, this advantage has become more significant for foreign private issuers because the SEC withdrew confidential treatment for foreign private issuers, except for dually listed companies or those concurrently listing outside the United States. If a foreign private issuer intends to rely on EGC status to take advantage of other EGC benefits, then it will be subject to the 21 day limitation before it must publicly submit its materials.6

ECG confidential submissions are not available for the Exchange Act filings such as Form 20-F or 40-F, which are also used for listing on a U.S. stock exchange.

EGCs May Elect Full Compliance. An EGC may elect to comply with the U.S. Securities Act of 1933, as amended (the "Securities Act") and Exchange Act requirements applicable to other public companies instead of taking advantage of the exemptions from those requirements available to EGCs.

If an EGC elects full compliance, the EGC:

- must make its choice when it is first required to file a

registration statement or report with the SEC under Section 13 of

the Exchange Act and notify the SEC of that choice; and

- may not pick and choose which standards to comply with, but

instead must comply with all the Securities Act and Exchange Act

standards to the same extent that a non-EGC must comply with those

standards for so long as the issuer remains an EGC.

Some EGCs may choose to comply voluntarily with selected disclosure requirements applicable to larger issuers if the reduced disclosures would adversely affect market reaction to the company's offering.

II. Deregulating Offers: General Solicitation and Advertising Will Be Permitted in Private Placements to Accredited Investors and QIBs

The JOBS Act directs the SEC to adopt rules to permit general solicitation and advertising in Rule 506 private placements, provided that all purchasers in the offering are accredited investors. Similarly, the SEC must permit general solicitation and advertising in re-sales of securities under Rule 144A under the Securities Act provided that all of the purchasers are reasonably believed to be QIBs. Consequently, securities may be offered to persons other than accredited investors and QIBs, by means of general solicitation and advertising, provided that the securities are sold only to persons that the seller and any person acting on its behalf reasonably believe is an accredited investor or QIB, as applicable. These changes could be used for early marketing of an offering as well as announcing offerings and placement agents in press releases. Issuers will have to establish compliance procedures to verify that purchasers of the securities are accredited investors or QIBs, as applicable.

The SEC will likely address in its rulemaking the prohibition on "directed selling efforts" in the United States for offerings outside the United States under Reg. S, which is very similar to "general solicitation" and "general advertising" and needed for offerings outside the United States side-by-side with offerings in the United States.

Exemption from Registration as a Broker-Dealer. For intermediaries offering and selling securities under Rule 506, the JOBS Act provides a new exemption from registration as a broker-dealer under Section 15(a)(1) of the Securities Act. This exemption will permit internet platforms to offer and sell securities broadly to the public. Specifically, the Act states that a person will not be subject to registration as a broker-dealer solely because that person:

- maintains a platform or other mechanism for the offer, sale,

purchase, or negotiation of securities, or permits general

solicitation, general advertisements, or similar or related

activities by the issuers of the securities;

- a person associated with that person co-invests in the

securities; or

- a person associated with that person provides "ancillary

services" for the securities.7

This new exemption only applies if the person receives no compensation in connection with the purchase or sale of the security; the person does not have possession of customer funds or securities in connection with the purchase or sale of the security; and the person is not subject to a statutory disqualification under Section 3(a)(39) of the Exchange Act (i.e., not a "bad actor") and does not have any person associated with that person subject to such a statutory disqualification.

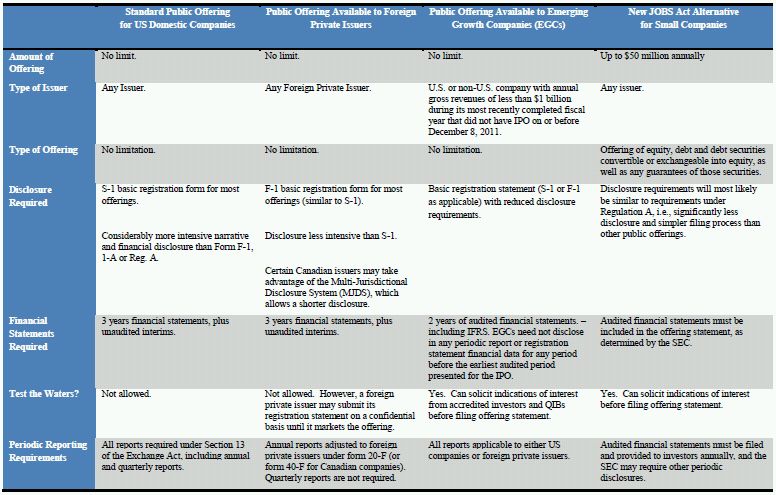

III. An Alternative for Public Offerings of up to $50 Million Every 12 Months

The JOBS Act creates a stripped down, less burdensome and less expensive procedure for qualifying public offerings with the SEC for companies to sell up to $50 million in securities within a 12 month period.8 The issuers can use this abbreviated registration procedure to sell equity, debt and debt securities convertible or exchangeable into equity, as well as any guarantees of those securities. The securities may be sold publicly, will not be restricted securities (i.e., can be publicly traded) and the issuer may solicit interest before the filing (test the waters) subject to such terms and conditions as the SEC may adopt. This exemption is expected to apply both to U.S. and non-U.S. issuers.

Although this procedure will be shorter and simpler than a full registration process, the SEC may require companies that are issuing securities through this process to file with the SEC and distribute to prospective investors an offering statement, including audited financial statements, a description of the issuer's business operations, financial condition, corporate governance principles, use of investor funds, and other appropriate matters. Additionally, the issuer will be required to provide audited financial statements with the SEC annually, and the SEC may require additional periodic disclosures about the issuer, its business operations, financial condition, corporate governance principles, use of investor funds, and other appropriate matters. Last, the SEC may disqualify "bad actors" from using this exemption.

The exact requirements of this registration are not yet clear and will be determined by the SEC. However, it appears to be a similar process and type of registration as is currently available under Regulation A, which is currently limited to $5 million and to US domestic and Canadian issuers.

Attached is a table that compares a standard public offering and Reg. A offering with the new exemption under Section 3(b)(2) of the Securities Act.

IV. Increase in Record Holder Threshold for Exchange Act Registration

The JOBS Act changed the threshold in Section 12(g) of the Exchange Act that requires registration as a reporting company when a company's shares become widely-held. Now, an issuer must register under the Exchange Act if, on the last day of its fiscal year, it has more than $10 million in total assets and a class of equity securities with either 2,000 holders of record or 500 holders of record who are not accredited investors. The former Exchange Act threshold was 500 shareholders of record. The new higher threshold will also apply to private funds relying on Section 3(c)(7) of the U.S. Investment Company Act.

Excluded from the calculation of total number are holders of securities acquired through the crowdfunding exemption, as discussed in the section below, and holders of securities received under employee compensation plans of the issuer under exemptions from Securities Act registration. These exclusions are in addition to the pre-existing exclusion for beneficial owners who are not also record holders, such as those persons who hold their securities through brokerage firms or other intermediaries. Private companies and their transfer agents may now have to monitor ownership of equity securities by non-accredited investors, which would add to the cost and complexity of maintaining stock records.

The JOBS Act also sets the thresholds for banks and bank holding companies with $10 million in assets and 2,000 record holders, with no separate threshold for record holders who are not accredited investors.

The new higher threshold could result in a substantial increase in the trading of non-U.S. issuers in the U.S. security markets and for private company securities in the secondary market because many such companies will be free to acquire a much larger shareholder base than was permitted. However, non-U.S. issuers must still monitor their shareholder base to maintain their status as a "foreign private issuer."

V. A New Exemption for Crowdfunding

The JOBS Act created a new exemption from registration under the Securities Act to permit crowdfunding, or raising small amounts of capital from large numbers of investors, for private companies, typically through the internet. The new crowdfunding exemption in Section 4(b) of the Securities Act permits a U.S. issuer that is non-reporting under the Exchange Act to raise up to $1 million within any 12 month period, including any amount sold in reliance on the crowdfunding exemption. The crowdfunding exemption is not directly available to non-U.S. issuers, U.S. public companies, or investment companies. 9 However, because of the publicity about crowdfunding, we describe the exemption below.

Limits on Purchasers. The company is limited to a maximum investment from each investor, which includes any amount sold in reliance on the crowdfunding exemption, plus any amount sold during the 12 months preceding the date of the transaction. This amount cannot exceed:

- the greater of $2,000 or 5% of the annual income or net worth

of the investor, if either the annual income or the net worth of

the investor is less than $100,000; or

- 10% of the annual income or net worth of the investor, not to

exceed a maximum aggregate amount sold of $100,000, if either the

annual income or net worth of the investor is equal to or more than

$100,000.10

Company Information. The company must file with the SEC and provide certain disclosures to investors and the relevant broker or funding portal concerning, among other items, the company business, business plan, pricing, ownership, capital structure, valuation, risk factors, financial condition, intended use of proceeds and target offering amount. The disclosures must include, for offerings that, together with all other crowdfunding offerings of the company within the preceding 12-month period, have, in the aggregate, target offering amounts of :

- $100,000 or less: (a) the income tax returns filed by the

company for the most recently completed year (if any); and (b)

financial statements of the company, which must be certified by the

principal executive officer of the company to be true and complete

in all material respects;

- more than $100,000, but not more than $500,000: financial

statements reviewed by an independent public accountant; and

- more than $500,000 (up to $1 million): audited financial

statements.

Any advertising of the offering must direct potential investors to the intermediary.

The intermediary must also disclose all amounts paid to compensate solicitors promoting the offering through the broker or funding portal.

Issuers relying on the exemption must file with the SEC and provide to investors, at least annually, reports of the results of operations and financial statements as the SEC may determine.

Intermediary Must be Used. The crowdfunding must be conducted through a broker or a funding portal that is registered with the SEC and the applicable self-regulatory organization. These broker-dealer or funding portal intermediaries must provide certain disclosures, complete a due diligence inquiry on the principals of the issuer, make certain company information available to the SEC and take certain other precautions.11

Funding Portals. All capital raises conducted through crowdfunding have to be conducted through a registered broker-dealer or funding portal. A "funding portal" is a new category defined as a person that acts as an intermediary in a transaction involving the offer or sale of securities for the account of others, solely under the new crowdfunding exemption. It is unclear whether a funding portal must be an electronic system, rather than a manual brokerage operation. However, a funding portal may not engage in the following basic brokers' activities: (a) offering investment advice or recommendations, (b) soliciting purchases or sales, (c) compensating employees, agents or other persons for those solicitations or based on the sale of securities, (d) holding, managing or otherwise handling investor funds or securities, or (e) engaging in such other activities as the SEC may determine.

Funding portals must register with the SEC as a funding portal or as a broker-dealer. Those entities that chose to register as a funding portal will be conditionally exempt from broker-dealer registration. A registered funding portal must (i) be a member of FINRA (which can be a lengthy process), (ii) remain subject to SEC examination, enforcement and rulemaking authority, and (iii) meet such other requirements that the SEC may determine.

State Securities Laws. Crowdfunded securities will be "covered securities", which are exempt from state securities law regulating offerings. However, as for all covered securities, the states will retain enforcement authority. State regulation of funding portals would also be preempted, subject to limited enforcement and examination authority.

Additional Factors. Certain "bad actors" will be disqualified from offering or selling securities under this exemption. During the first year after their issuance, securities issued under the crowdfunding exemption may only be transferred to the company, accredited investors or certain family members or sold in a public offering. Holders of securities acquired in a crowdfunding transaction will not be considered record holders that count for purposes of the threshold triggering SEC registration under the Exchange Act.

Raising capital from a large number of shareholders in small amounts raises potential challenges for a company, such as increased record keeping responsibilities. It also remains to be seen whether venture capital funds and other later stage investors will avoid crowdfunded companies or, if not, how crowd funders will react to later dilution or lower priority resulting from later rounds of financing.

VI. Effectiveness of JOBS Act

The JOBS Act was enacted on April 5, 2012. Most provisions of the JOBS Act became effective at the time of enactment, such as those relating to EGCs and the higher shareholder threshold for Exchange Act registration. Some reforms cannot become operative until the SEC completes rulemaking, such as those relating to the elimination of the ban on general solicitation and advertising (July 5, 2012, i.e., 90 days after enactment), the crowdfunding exemption (270 days after enactment), and the new Regulation A type exemption. Other reforms, such as several of those that provide EGCs with relief from disclosure and other regulatory burdens, can be operational immediately but may require SEC guidance or rulemaking to be fully effective.

Footnotes

1 The $1 billion limit is subject to adjustment by the SEC every five years for inflation.

2 SEC Interpretation: Jumpstart Our Business Startups Act Frequently Asked Questions, April 16, 2012, question 8.

3 Id, question 10.

4 Or one year if the issuer was an EGC for more than two years before its IPO.

5 As these terms are defined in section 230.144A and section 230.501(a) of title 17, Code of Federal Regulations.

6 SEC Interpretation: Jumpstart Our Business Startups Act Frequently Asked Questions, April 16, 2012, question 9.

7 Ancillary service is defined in Section 201(c)(3) of the rule as ''(A) the provision of due diligence services, in connection with the offer, sale, purchase, or negotiation of such security, so long as such services do not include, for separate compensation, investment advice or recommendations to issuers or investors"; and ''(B) the provision of standardized documents to the issuers and investors, so long as such person or entity does not negotiate the terms of the issuance for and on behalf of third parties and issuers are not required to use the standardized documents as a condition of using the service.''

8 This amount is subject to adjustment every two years.

9 Funds exempt from registration under the Investment Company Act of 1940 by reason of Section 3(c), including hedge funds and private equity funds, cannot take advantage of the crowdfunding provisions. Further, non-U.S. dealers or funding portals cannot participate in crowdfunding.

10 These amounts will be indexed for inflation every five years.

11 Specifically, the broker-dealer or funding portal must:

- provide certain disclosures, including disclosures related

to risks and other investor-education materials,

- ensure that each investor: reviews investor-education

information and affirms that the investor understands that he may

lose the entire investment and can bear that loss and understands

the level of risk for emerging businesses and the risk of

illiquidity;

- conduct due diligence on the principals of the issuer,

including obtaining a background and securities enforcement

regulatory history check on each officer, director and person

holding more than 20% of the outstanding equity of every company

whose securities are offered by such person,

- within 21 days before the first sale to an investor, make

available to the SEC and potential investors the company

information described below;

- ensure that the offering proceeds are provided to the

issuer when the aggregate capital raised is equal to a greater than

the target offering amount;

- allow investors to cancel their commitment under terms

determined by the SEC; and

- make efforts to ensure that no investor in a 12-month

period has purchased securities offered pursuant to a crowd funded

offering that, in the aggregate, from all companies, exceed the

investor's limits.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.