- within Government, Public Sector, Wealth Management and International Law topic(s)

- with readers working within the Media & Information industries

Australia proposes to introduce standardised, internationally aligned requirements for mandatory disclosure of climate-related financial risks and opportunities for large businesses. The mandatory climate reporting requirements are proposed to commence in a staged approach from the financial year starting 1 July 2024 for the initial reporting entities.

In January 2024, after more than a year of consultation, the Australian Government released an exposure draft Bill to give effect to the new mandatory reporting regime through the Corporations Act 2001 (Cth) (Corporations Act). Although the draft Bill was open for further public consultation, the policy design for the regime has been finalised. Any changes following the consultation are likely to be minor, and we expect the draft Bill to be introduced to Parliament shortly to enable the proposed regime to commence from 1 July 2024.

Under the proposed regime, additional reporting requirements will be required of entities that already prepare and lodge financial reports under Chapter 2M of the Corporations Act (public companies, disclosing entities, large proprietary companies, registered schemes and registrable superannuation entities) and meet one or more of the following:

- certain thresholds associated with their size;

- classified as a registered corporation (or required to apply to be registered) under the National Greenhouse and Energy Reporting Act 2007 (Cth) (NGER Act);

- asset owners, where the value of the assets exceeds the

applicable threshold,

(Reporting Entities).

Others will be indirectly affected as Reporting Entities seek the data they require to meet their reporting obligations related to Scope 3 emissions from across their value chain. As the largest businesses and emitters will report on Scope 3 emissions from the financial year commencing 1 July 2025, others will be quickly drawn into the climate-related disclosure regime.

Climate related disclosures will be made in the form of a 'Sustainability Report' that will be included in an entity's annual financial report and must be audited. Reporting Entities will need to keep records relating to the Sustainability Report for 7 years.

As with annual financial reports, public companies must provide the Sustainability Report to members and include it in the business of an AGM, and we expect this to become standard practice for other Reporting Entities too.

Although, initially, the Sustainability Report will be limited to mandatory climate-related disclosures, we expect future extensions to the reporting structure to include disclosures relating to other aspects of sustainability.

See here for some commonly used climate emissions terminology.

Why is this regime being introduced?

The new regime seeks to ensure that large businesses, greenhouse gas emitters and energy users in Australia disclose their climate-related strategy, governance, risks and opportunities, in line with international standards and similar reporting regimes elsewhere. This will provide businesses, investors, regulators and the public with a clear and common understanding of the climate-related strategies, risks and opportunities associated with the Reporting Entities. The explanatory materials for the draft Bill also explain that improved climate disclosures will support regulators to assess and manage systemic climate related risks to Australia's financial system.

Many public companies already voluntarily report against sustainability criteria, which are largely market focussed, as part of their annual reporting documents. As the new regime will be data driven, with assurance requirements, it is intended that investors will be provided greater transparency about an entity's climate-related strategies and comparable information to make more meaningful decisions. This should also limit opportunities to engage in greenwashing.

Who is required to prepare a Sustainability Report?

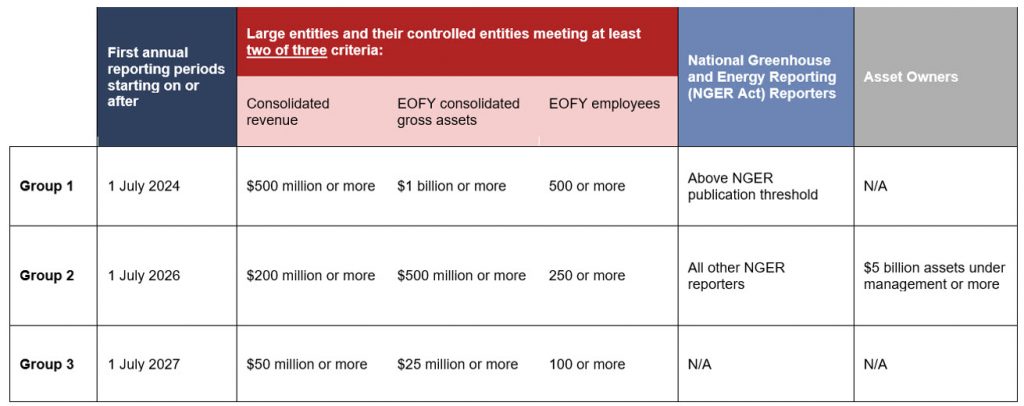

The disclosure obligations will apply to 3 groups, phased-in over a

4 year period. The timing of obligations depends on meeting

criteria as set out in the table below. All Reporting Entities will

be required to prepare Sustainability Reports in respect of the

financial year commencing 1 July 2027 at the latest.

The requirements to prepare a Sustainability Report apply to entities that must prepare and lodge annual reports under Chapter 2M of the Corporations Act and fall within one (or more) of the 3 categories set out in the table.

An entity that is a registered corporation (or required to make an application to be registered) under the NGER Act will be required to prepare a Sustainability Report. Its first annual reporting period will start on 1 July 2024 if the entity meets the threshold at which the Clean Energy Regulator publishes emissions data for the entity, including its corporate group. For example, a corporate group meets the threshold for a financial year if the combined Scope 1 and Scope 2 greenhouse gases emissions by members of the group is at least 50 kilotonnes CO2e-, or a member of the group emits at least 25 kilotonnes CO2e-, or produces or consumes 100 terajoules of energy.

A company limited by guarantee with annual (consolidated) revenue of $1 million or more, and which meets any of the other thresholds, is also required to prepare a Sustainability Report to members who choose to receive it.

Reporting Groups

Entities will not be required to make climate-related financial disclosures if they are:

- below the thresholds above; or

- exempt from lodging financial reports under Chapter 2M of the Corporations Act, including where exemptions have been made through ASIC class orders, where registered foreign companies comply with s 601CK (being under Chapter 5B) of the Corporations Act, or where the Entity is registered with the Australian Charities and Not-for profits Commission.

For example, sole traders, partnerships, trusts and State statutory corporations are unlikely to be directly caught by the regime.

What will Reporting Entities have to do?

Prepare a Sustainability Report

Reporting Entities will need to prepare a Sustainability Report each financial year, which will form part of their annual financial report and consist of:

- a climate statement for the year;

- notes to the climate statement;

- any statements prescribed by regulation; and

- the directors' declaration on whether the climate statements are made in accordance with the Corporations Act and in compliance with the relevant sustainability standards.

Climate statements must disclose:

- the Reporting Entity's material climate risks and opportunities for the financial year;

- any metrics and targets of the Reporting Entity for the financial year related to climate, including scope 1, scope 2 and scope 3 emissions; and

- any governance or risk management processes, controls and procedures of the Reporting Entity related to these matters.

The climate statements must be prepared in line with the relevant sustainability standards issued by the Australian Accounting Standards Board (AASB). The proposed AASB sustainability standards are intended to align with the International Sustainability Standards Board (ISSB) as much as possible, with modifications where necessary to apply these standards in the Australian context. The AASB released draft standards in October 2023 for consultation which closes on 1 March 2024 and proposes to issue the final Australian climate-related disclosure standards in Q2 2024.

Scope 1 and Scope 2 emissions are already defined under the NGER Act and are already relevant to reporting under the NGER Act. However, the draft Bill introduces a definition of Scope 3 emissions into the Corporations Act, which is to have the same meaning as in the Corporate Value Chain (Scope 3) Accounting and Reporting Standard, published by the Word Business Council for Sustainable Development and the World Resources Institute.

Prepare for Auditing

Audit and assurance of climate disclosures will be phased, with assurance of Scope 1 and Scope 2 emissions disclosures commencing from the financial year beginning 1 July 2024 and full assurance of climate disclosures from 1 July 2030.

Audits must be conducted by the auditor of the entity's financial reports (with support from climate and sustainability experts) in accordance with new assurance standards to be published by the Auditing and Assurance Standards Board, which will mirror international assurance standards. Existing auditor duties will extend to these new reports. New strict liability offences will apply.

Keep Records

Reporting Entities are required to keep records that correctly explain and record its preparation of its climate statements for 7 years. These sustainability records include documents and working papers that explain the methods, assumptions and evidence from which the statements are derived.

Include in Equity Fundraisings

Entities issuing a prospectus for listed securities or a product disclosure statement relating to a managed investment scheme, must inform investors of their right to obtain a copy of the most recently lodged Sustainability Report, where relevant.

Similarly, for securities offered under an offer information statement, such statement must include a copy of the most recent Sustainability Report prepared by the offering entity.

Are there any qualifications to disclosure requirements?

Materiality exemption for Group 3 Entities

Group 3 entities will only be required to make climate-related disclosures if they face material climate-related risks or opportunities for that financial period. Materiality is to be assessed in accordance with the sustainability standards.

If Group 3 entities believe they do not have any material climate-related risks or opportunities, they will only be required to disclose a statement to that effect.

Scope 3 emissions from second reporting year

Reporting Entities are exempt from reporting on Scope 3 emissions for their first compliance year. It is also intended that Scope 3 disclosures need only represent information that is available at the reporting date without undue cost or effort to the Reporting Entity.

What is the liability for not complying?

To ensure directors engage fully with climate disclosure obligations and to support investor confidence in the information disclosed, the new regime will be subject to existing liability frameworks under the Corporations Act and Australian Securities and Investments Commission Act 2001 (Cth) e.g. directors' duties, misleading and deceptive conduct and general disclosure obligations.

However, for sustainability reports issued between 1 July 2024 and 30 June 2027, Reporting Entities will not be financially penalised for inaccuracies relating to scope 3 emissions and certain climate-related forward-looking statements. During this transition period, the regulator may only bring an action seeking an injunction or declaration (e.g. to amend an incorrect or misleading statement) regarding such disclosures. The regulator may also direct a Reporting Entity to confirm that a statement is correct or complete, and to correct, complete or amend a statement in accordance with a direction. Failure to comply with a direction will be subject to a penalty.

Beyond this transition period, the existing liability arrangements will apply. As Group 3 entities will be subject to the existing liability regime from their first reporting year, it is important that they monitor the directions and enforcement activity of the regulator during the transition period.

What do you need to do next?

You should prepare for the new mandatory reporting regime by:

- Skilling up: Understand the new requirements, particularly your Board's duties to understand climate risks and opportunities within your organisation and develop strategies to address these, and reporting compliance obligations.

- Setting a timeline: Assess the nature and size of your organisation to determine which reporting group your organisation falls into and when your reporting obligations will start. Consider when others in your value chain may seek emissions data from you to be able to report their scope 3 emissions.

- Collecting data / building a reporting trail: Perform a preliminary gap analysis to understand your climate risks and opportunities and emissions metrics, and those of your value chain, particularly when you need to begin reporting scope 3 emissions. Consider how you will collect and manage data, including from and to others in your value chain. Consider whether contracts within your value chain need to be amended to provide for the provision of emissions data.

- Assembling a team: Engage with your legal and accounting advisors and other consultants who can assist you to collect and measure data to understand how and what you need to report.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.