- within International Law topic(s)

- within International Law and Law Department Performance topic(s)

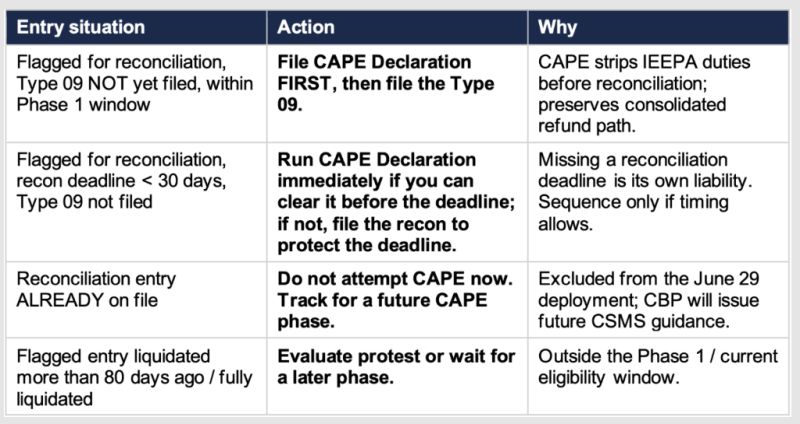

If you have entries flagged for reconciliation and a reconciliation deadline inside the next 30 days, the order in which you file has just become a decision that can cost you your IEEPA refund. Under CBP’s June 29, 2026, CAPE deployment, once you file the reconciliation entry (Type 09), the underlying entries are locked out of CAPE in this phase. File the recon first, and you have stripped your own entries of the consolidated IEEPA refund path — permanently, for now. The new functionality is genuinely good news. The trap is in the sequence.

Key points:

- New as of June 29, 2026: CAPE will accept entries flagged for reconciliation (Entry Types 01, 02, 06) even when no Type 09 reconciliation entry has been filed yet.

- The sequence that wins: File the CAPE Declaration FIRST. CAPE strips the IEEPA duties from the flagged entries, then you file the reconciliation.

- The sequence that loses: File the reconciliation entry first. The underlying entries are then ineligible for CAPE in this phase.

- Still not covered: Entries where the reconciliation entry is already on file — those wait for a future CAPE phase.

Same eligibility limits as Phase 1 carry over: unliquidated entries and entries within 80 days of liquidation only.

The Challenge: Reconciliation Was a Hole in Phase 1

When CBP launched Phase 1 of the Consolidated Administration and Processing of Entries (CAPE) tool on April 20, 2026, it gave importers a consolidated, automated path to recover duties paid under the International Emergency Economic Powers Act (IEEPA) — the tariffs the Supreme Court struck down. We covered the mechanics in detail in our CAPE Refund Process overview and our ongoing IEEPA Tariff Refund Updates.

But Phase 1 had carve-outs, and one of the most disruptive was entries flagged for reconciliation. Reconciliation lets importers enter goods with the best available information and finalize specific elements — value, classification, 9802, or FTA claims — later, via a single Type 09 reconciliation entry. For importers who flag entries for reconciliation as standard practice (automotive, apparel, related-party pricing, and any program with transfer-pricing true-ups), a large share of IEEPA-bearing entries sat outside CAPE entirely.

That created a real dilemma. Reconciliation deadlines are hard deadlines. IEEPA refunds are large. And the two processes were colliding with no clean way to handle an entry that needed both.

What Changed: CSMS #69035485 (Effective June 29, 2026)

CBP’s CSMS #69035485 adds the missing functionality. Effective June 29, 2026, CAPE will accept entries flagged for reconciliation — Entry Types 01, 02, and 06 — for which the reconciliation entry (Type 09) has not yet been filed. The eligibility window is unchanged from Phase 1: only unliquidated entries and entries within 80 days of liquidation qualify.

Here is the mechanism that matters, and it is the entire reason sequence is everything:

- You file a CAPE Declaration listing the reconciliation-flagged entries.

- CAPE removes the IEEPA duties from those flagged entries before the reconciliation entry is filed — separating the IEEPA refund from the reconciliation calculation.

- You then file your Type 09 reconciliation entry, which no longer has to carry the IEEPA duty math.

- Once the reconciliation entry is filed, CBP assumes all CAPE Declarations tied to those reconciled entries were filed and accepted, and the underlying entries become ineligible to be added to a CAPE Declaration in this phase.

Why the Order Is Non-Negotiable

Read that last bullet again. Filing the reconciliation entry closes the CAPE door on the underlying entries for this phase. If you file the Type 09 before you have run those entries through a CAPE Declaration, you have not lost the right to a refund in the abstract — but you have removed them from the consolidated, automated CAPE path and pushed yourself toward slower, manual, entry-by-entry remedies. With consolidated interest-bearing refunds flowing through CAPE on a 60–90 day cycle, that is not a clerical preference. It is real money and real time.

The One Scenario CSMS #69035485 Does NOT Solve

If your reconciliation entry is already on file, these entries are not part of the June 29 deployment. CBP has confirmed this group will be handled in a future CAPE phase. Critically, CBP’s guidance is explicit that the CAPE process does not stop an entry from being reconciled — so if a reconciliation filing deadline is close to expiring (CBP uses less than 30 days as the marker), you must prioritize filing the reconciliation and let the IEEPA refund follow in a later phase. Do not blow a reconciliation deadline waiting on CAPE.

Decision Matrix: What to Do With Each Entry

The Strategy: A Five-Step Sequencing Protocol

- Pull and tag your reconciliation-flagged inventory now. Work with your broker to identify every Entry Type 01, 02, or 06 carrying an IEEPA Chapter 99 code (9903.01 / 9903.02) that is flagged for reconciliation, with the reconciliation filing deadline and liquidation date for each.

- Split the list by Type 09 status. Recon not yet filed = eligible for the June 29 path. Recon already filed = parked for a future phase. This single split drives every downstream decision.

- For each “recon-not-filed” entry, check the clock. Confirm it is unliquidated or within 80 days of liquidation, and note how many days remain on the reconciliation deadline.

- File CAPE before reconciliation — every time the calendar allows. Submit the CAPE Declaration, confirm acceptance, then file the Type 09. Build the sequence into your broker SOP, so no one files a reconciliation entry on an IEEPA-bearing matter without a CAPE check first.

- Escalate the tight deadlines. Any entry with a reconciliation deadline under 30 days needs a same-week decision: clear CAPE first if achievable, or protect the deadline and pursue the refund later. Do not let a refund-optimization goal cause a reconciliation default.

The Outcome: Protect the Refund Without Defaulting the Reconciliation

Importers who build the CAPE-before-Type-09 sequence into their workflow this week capture their reconciliation-flagged entries on the consolidated, interest-bearing CAPE refund path instead of forcing those duties into slower manual channels. Importers who don’t — who let a reconciliation entry get filed first out of habit — lock those entries out of CAPE for this phase. The difference between the two outcomes is process discipline, not legal entitlement.

And underneath all of this sits the larger strategic question we have flagged since the CAPE rollout began: voluntarily processed CAPE refunds are not guaranteed to be insulated from later government recoupment or offset, and the Administration has signaled it will contest refunds aggressively. Sequencing your CAPE and reconciliation filings correctly is the operational layer. The strategic layer — whether to also preserve rights through a CIT challenge — is a conversation every materially affected importer should be having now.

How Diaz Trade Law Can Help

Diaz Trade Law is actively advising importers on IEEPA refund strategy — from building reconciliation-vs-CAPE sequencing protocols and coordinating with your broker, to evaluating whether a parallel CIT challenge should be filed to preserve your rights. If you have reconciliation-flagged entries and IEEPA duties at stake, the time to map your filing order is before June 29, not after a Type 09 has already gone in.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]