- within Strategy, Coronavirus (COVID-19) and Accounting and Audit topic(s)

The Department of Justice ("DOJ") has filed a civil

antitrust lawsuit challenging the $20 billion proposed acquisition

by Anheuser-Bush InBev ("ABI") of the remaining 50

percent interest in Grupo Modelo S.A.B. de C.V.

("Modelo"), the producer of Corona Extra, the

best-selling imported beer in the United States. The lawsuit

alleges that the transaction would not only eliminate head-to-head

competition, resulting in increased prices and less innovation, but

also would remove Modelo as a disruptive pricing influence in the

overall marketplace. The DOJ rejected ABI's attempt to resolve

the DOJ's concerns through a voluntary supply agreement, which

would have allowed Modelo's existing joint venture partner in

the U.S., Constellation, to gain exclusive control over the import

of Modelo beer into the United States for a period of at least ten

years.

ABI is the largest brewer in the United States and owns more than

200 beer brands, including the number one domestic brand (Bud

Light). Modelo is the third largest brewer in the country and

owns several brands, including Corona Extra, the top-selling U.S.

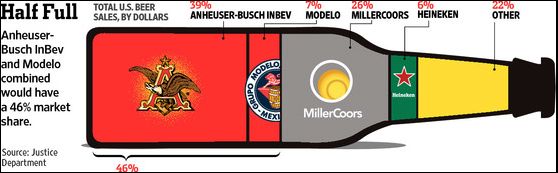

import. The DOJ complaint states that together ABI and

Modelo control about 46 percent of annual beer sales in the United

States, as reflected in graph below.

The complaint also states that the proposed acquisition would

substantially lessen competition in the market for beer in 26

metropolitan statistical areas ("MSAs") and also on a

national basis. In addition to combined national shares of

about 46 percent, the parties would have between 34 and 64

percent of annual sales in the 26 relevant MSAs.

The DOJ also alleged that head-to-head competition between ABI and

Modelo has resulted not only in lower prices, but also increased

innovation. The complaint states that ABI introduced Bud

Light Lime in a clear bottle to mimic Corona and that it had once

considered launching a new line, "Michelob Especial" to

compete with "Modelo Especial." The other examples

of "innovation" in the beer industry were plans to

acquire beers that would appeal to consumers currently buying

Mexican imports.

Modelo's share is relatively low for a merger challenge based

on the theory that the postmerger company alone can cause price

increases ("unilateral effects"). But the DOJ

complaint's allegations suggest the government's theory is

that, after the transaction, the market's suppliers will find

it easier tacitly to coordinate their competition

("coordinated effects"). The complaint highlights

Modelo's history as a disruptive price competitor, one that

chose not to follow ABI's annual and "transparent"

price increases.

The DOJ's complaint makes numerous references to the

parties' own documents. According to the DOJ, ABI's

internal company documents acknowledge that Modelo has "put

increasing pressure" on ABI competitively and that

Modelo's strategy to gain share through price competition is

"at odds with ABI's well-established practice of leading

prices upward with the expectation that its competitors will

follow." The complaint also highlights ABI's

"Conduct Plan," a strategic plan for pricing "that

reads like a how-to manual for successful price

coordination."

According to the complaint, "in an effective acknowledgement

that the acquisition of Modelo raises significant competitive

concerns," ABI had voluntarily entered into an agreement to

grant Constellation the exclusive right to import Modelo beer into

the U.S. for the next ten years, if the Modelo acquisition

closes. Constellation currently imports and sells Modelo

products into the U.S. through a 50/50 joint venture with Modelo

called Crown Imports. Making Constellation the exclusive

importer may have seemed like a logical fix. (The DOJ's

2008 settlement regarding InBev's acquisition of Anheuser-Busch

may have inspired this attempted voluntary remedy. In 2008,

the DOJ required InBev to sell Labatt USA to a DOJ-approved

acquirer and to grant that acquirer a license to brew and sell

Labatt beer for consumption in the United States. In

addition, at the option of the acquirer, InBev had to supply Labatt

brand beer for up to three years to the acquirer in quantities and

units and at prices agreed to between InBev and the acquirer with

the approval of the DOJ. Labatt USA was sold to KPS, a

private equity firm that had acquired a brewery earlier that year.

The DOJ's 2008 order expires ten years from the date

issued.)

Here, ABI planned to sell Modelo's existing 50 percent interest

in Crown to Constellation and then enter into a ten year exclusive

agreement to supply Constellation with Modelo beer to import into

the US. Unlike in the 2008 InBev settlement, the DOJ did not

approve the divestiture beneficiary or the terms of the

agreement. The complaint criticizes the proposed remedy,

which did not include licensing of the Modelo brand or the

divestiture of brewing facilities, alleging that an importer

without its own brewing facilities or brands would be totally

dependent on ABI for its supply of Modelo brand beer. Furthermore,

Constellation's internal documents demonstrated that, unlike

Crown and Modelo, "Constellation's executives have sought

to follow ABI's pricing lead."

The DOJ alleged that the close supply relationship between ABI and

Constellation would further facilitate joint pricing between the

two companies, given the information exchange and ABI's

opportunity to reward or punish Constellation for pricing

actions. In contrast, although ABI already owns just over 50

percent of Modelo, the DOJ concluded that firewalls and a lack of

voting or effective control had successfully insulated Modelo from

ABI's influence.

A lesson from the ABI remedy proposal is, parties may hope to save

time by crafting their own proposed remedies in advance, but the

federal antitrust agencies will likely approach pre-packaged

settlements with initial skepticism. While proposing remedies

can expedite the merger review timeline, parties should be prepared

to engage with the agencies in the remedy planning process and be

prepared to modify their proposals, especially with regards to the

identity of the divestiture acquirer. The DOJ's complaint

also demonstrates that there are no market share "safe

harbors" in an antitrust agency's merger review. The

US antitrust agencies will carefully review the competitive

dynamics in each affected market segment and they will challenge

transactions even where one of the merging parties has less than

10% market share. In this case, like other recent DOJ merger

challenges Bazaarvoice/PowerReviews and H&R Block/Tax Act, the

DOJ relied on internal company documents to support its competitive

theories of harm. The DOJ will not only rely on the

parties' internal documents, but also third parties'

internal documents, like customers and suppliers'

documents. Moreover, while comments made about market share

and ability to raise prices post-transaction raise red flags, the

DOJ is also sensitive to documents discussing efforts to signal

competitors to follow competitive actions. While there is

nothing wrong with competitors monitoring and reacting to each

other's prices, plans to "stabilize" pricing are

suspect.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.