- within Government and Public Sector topic(s)

The Chancellor delivered his Autumn Budget today, setting out the Government's tax policy for the next fiscal period. Forewarned of a "balanced approach" in advance, there was little that surprised, other than in respect of the proposed CGT changes for non-residents investing in commercial property. However, a welcome announcement for first-time buyers was made, exempting stamp duty land tax on the first £300,000 of the purchase price, provided the price itself is under £500,000.

Otherwise, the Chancellor made very few substantive tax announcements in his Budget speech, the key points being published in the background papers. Even then, the number of definite changes were limited, with a raft of consultations announced but few confirmed proposals. He promised to face the tax challenge posed by the digital economy, proposing to impose UK income tax on multinational digital businesses where their royalties are paid to low tax jurisdictions from April 2019, as well as dealing with online VAT fraud by making suppliers and online marketplaces jointly and severally liable for VAT.

Brexit was mentioned and the Chancellor confirmed that £3bn has been set aside for Brexit with £700m already spent. However, none of the measures focused on post-Brexit Britain. Indeed it might come as no surprise that several of the measures to be introduced will not take effect until after March 2019, when Britain is likely to have left the EU.

In this briefing we highlight some of the main points of interest.

Major changes for non-UK property investors

Capital gains

From April 2019, the Government intends to bring non-UK residents within the scope of UK corporation tax or capital gains tax (CGT) on gains arising on the disposal of UK commercial property. Important features of the new rules include:

- The new rules will apply a single, unified regime to both UK residents and non-UK resident investors.

- There will be a valuation "rebasing" of interests in UK commercial properties held by non-residents from April 2019 (so historic gains will not be subject to the new tax). Note that there will be the option to disapply these rules on direct property sales if rebasing would give rise to a worse result.

- The new rules will apply to both the direct disposal of UK property, but also the disposal of indirect interests in UK property. This will include the sale of a "property rich" company by a person (or connected persons) who have at least a 25% interest in that company. A "property rich" company will broadly be one where 75% or more of its gross value at disposal is represented by UK property.

- For so-called indirect disposals, there will be a reporting requirement for the non-resident investor's UK advisers, who must report a sale to HMRC within 60 days (unless they are reasonably satisfied that the non-resident has reported it).

- The Government will introduce certain "anti-forestalling" rules and a Targeted Anti-Avoidance Rule (TAAR) to give the changes more teeth.

The current CGT exemption for non-UK resident investors in UK commercial property has long since been under siege, given the annual raft of changes to the UK tax code governing UK residential real estate. The Government has now decided to kick the front door in from April 2019. These are major changes: non-resident investors in UK commercial property will have to factor in UK tax on capital gains arising on disposals from April 2019. The proposals are still being consulted on, but the Government has made it clear that the core aspects of these changes are going to come into force, so it is only really consulting on the detail. It is not only non-UK resident investors in commercial property who will be hit. For example, the current CGT regime for residential property provides an exemption for "widely held" non-resident companies – this carve out will be removed as owners of residential property in those circumstances will simply be subject to the same rules as those owning commercial property. Will the changes make the UK less attractive? The answer is clearly yes from a tax point of view, but the impact on behaviour will remain to be seen. Will it drive more investors onshore, in search of tax efficient vehicles? For example, Real Estate Investment Trusts and PAIFs will be extremely attractive vehicles, assuming that the Government does not seek to tinker with the tax benefits associated with their ring-fenced property investment businesses.

Non-resident landlords to be brought within the scope of corporation tax?

The Government has stated that it shall or will publish a response to the consultation on bringing non-resident companies within the scope of corporation tax on their property income "shortly after the Autumn Budget".

Bringing non-resident landlords within the scope of corporation tax, rather than income tax, at first sight sounds favourable. After all, corporation tax is lower at 19%, falling to 17%, compared with 20% income tax. Unfortunately, recent changes to the corporation tax rules mean that this decision, to be consulted on further next year, and taking effect from 6 April 2020, could increase the net tax from UK property receipts. This is because companies paying corporation tax can be restricted on the amount of interest and other finance costs they can deduct beyond the restrictions applicable to income tax payers. In addition, companies paying corporation tax can be subject to the hybrid rules if, as is common in some structures, individual entities or interests in entities have different tax treatment in different countries. This decision is consistent with other measures, whether announced in earlier Budgets or this Budget, to equalise the tax take from UK activities irrespective of how the assets are held or financed. It may mean that corporate taxpayers and their advisers in due course may not have to be so concerned about the Non-Resident Landlord Scheme and withholding from rent, if HMRC are more confident that corporation tax can be collected. This proposal forms part of a wholesale revision of the tax treatment of UK property (for example, the extension of capital gains tax to non-UK resident investors in commercial property).

SDLT and first-time buyers

There are a number of miscellaneous changes to SDLT announced in the Spring Budget 2017.

First-time buyers

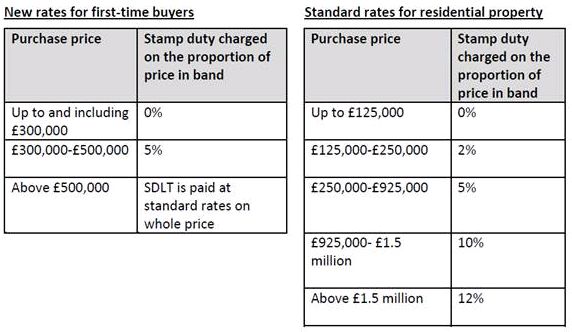

The Government has extended the stamp duty land tax (SDLT) relief for first-time buyers of residential property with a value up to £500,000.

The relief will mean that first-time buyers purchasing homes intended to be their only or main residence:

- up to £300,000 will benefit from a new 0% rate of SDLT, and

- between £300,001 and £500,000 will be subject to a 5% rate on any sums over £300,000.

A comparison of the new rates with the "standard" residential rates is set out below:

This is a welcome change for those falling within the definition of "first-time buyer". This definition will broadly mean someone who has never owned an interest in any residential property anywhere in the world at any time. The maximum saving will be £5,000.

Changes to 3% additional rate for residential property

As announced at the Autumn Budget 2017, the Government has stated that it will legislate in Finance Bill 2017-18 to make some minor amendments to improve the operation of the 3% SDLT surcharge for additional residential properties by granting relief in certain cases where:

- a court order issued on a divorce or dissolution of a civil partnership prevents someone from disposing of their interest in a main residence;

- an individual buys property from their spouse;

- a person buys a property in a child's name or on a child's behalf, where they are doing so in their capacity as the deputy of that child; or

- a purchaser adds to their interest in their existing main residence.

These changes will take effect from 22 November 2017.

The relief noted at point 4 above is particularly helpful as it gives relief from the surcharge for the price paid for lease extensions on a main residence, which was one of the more unfair applications of the rules. However, the draft legislation shows that this relief will be subject to certain carve outs, including where the existing interest is a lease with a remaining term of less than 21 years.

14 day SDLT filing and payment window

The Government has confirmed that the SDLT filing and payment window will be reduced from 30 days to 14 days, applying to land transactions with an effective date on and after 1 March 2019.

The new time limit will be onerous for professional advisers, particularly on larger scale portfolio transactions. The only plus point is that the Government is planning improvements to the land transaction return to make compliance with the new time limit easier. Legislation will be introduced in Finance Bill 2018-19.

Trusts and offshore structures

As announced in December 2016, the Government is introducing new anti-avoidance rules relating to offshore trusts. Draft legislation was published on 13 September 2017. The new rules ensure that where a benefit is provided to a close family member of a UK resident settlor, the benefit is taxable as if received by the settlor. A trust distribution to a non-resident on or after 6 April 2018 will no longer be matched against the pool of trust gains. Where a beneficiary receives a trust distribution tax-free (because he is non-resident or a non-domiciled remittance basis user who does not remit the payment), but then makes an onward gift to a UK resident, the UK resident is treated as if he had received a trust distribution equal to the amount of the gift. Following consultation, minor changes have been made to the legislation, including to ensure that the onward gift rules can still apply if the close family member rule applies and in certain specific circumstances, to clarify the position in the year of the settlor's death, and in relation to onward gifts to multiple recipients. The changes will have effect on and after 6 April 2018.

The Government will publish a response to its consultation, carried out between December 2016 and February 2017, on its proposal to require businesses or intermediaries creating or promoting certain types of complex offshore financial arrangements to notify HMRC of these structures and the details of their clients using these arrangements. The response document will be published on 1 December 2017.

The Government will publish a consultation in 2018 on how to make the taxation of trusts generally simpler, fairer and more transparent.

The Government has reaffirmed its commitment to simplify the tax system, but attempts by previous Governments to deliver reductions in complexity have usually come to nothing and the volume of tax legislation has grown inexorably. The rewrite of tax law to date has used simpler language but at much greater length and without resolving the underlying complexity in the legislation. Nevertheless we would welcome a genuine simplification of the taxation of trusts given the complexity of the current rules.

Finally, clients still have a narrow window of opportunity until 5 April 2018 to "wash out" gains within offshore trusts, meaning that those gains never come within the charge to tax. This is a one-off tax windfall that should not be missed.

Reforms to investor reliefs

The Government plans to make reforms to the Venture Capital Schemes (Seed Enterprise Investment Scheme (SEIS), Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCTs)). These reforms reflect a drive by the Government to incentivise investment in entrepreneurs and start-ups looking to grow their businesses. Relief to investors under the Venture Capital Schemes will be increasingly focussed on companies where there is a real risk to the capital being invested. The Government intends to release guidance on these changes shortly after the publication of Finance Bill 2017-18. HMRC will no longer provide advance assurance in respect of investments that do not meet the 'capital risk condition' on or after the date of publication of the guidance.

Other reforms to be introduced in Finance Bill 2017-18 include:

- Doubling the limit on the amount an individual may invest under the EIS in a tax year to £2 million, provided any amount over £1 million is invested in one or more knowledge intensive companies;

- Increasing the annual investment limit for knowledge intensive companies receiving investments under the EIS and from VCTs to £10 million from the current limit of £5 million;

- Introducing measures to move VCTs towards higher risk investments; and

- Introducing measures to provide that all risk finance investments, whenever made, will count towards the lifetime funding limits for companies receiving investments on or after 1 December 2017 under the EIS and VCTs.

These reliefs can provide generous income tax and capital gains tax breaks to investors who have the appetite to invest in smaller, higher risk trading companies. Growing companies and social enterprises relying on these reliefs to attract investment should seriously consider seeking advice before any funding rounds as the qualifying rules continue to become increasingly prescriptive. Companies that get it wrong will have to deal with some very unhappy investors.

Entrepreneurs' Relief

The Government plans to consult on a major change to Entrepreneurs' Relief in Spring 2018. Under the current rules, broadly a person should qualify for the reduced 10% rate of capital gains tax if they hold at least 5% of the ordinary share capital in a qualifying company and can exercise at least 5% of the voting rights for at least 12 months prior to their disposal of the shares. The Government's consultation will examine how entrepreneurs can remain eligible for the relief where additional funds are raised by issuing new shares to outside parties which consequently dilutes an individual's shareholding and/or voting rights below the 5% qualifying level.

The Government foresees that these measures will incentivise entrepreneurs to remain involved in businesses whilst still being able to raise outside investment. The changes should provide reassurance to entrepreneurs at the point of investment that any future fund raises by the company will not jeopardise their personal tax position and will sensibly remove the need for complex anti-dilution planning and agreements between the entrepreneurs and the company.

Disguised remuneration

Further to announcements made in 2016 and earlier this year, the Government has, as expected, pledged to continue to be proactive in addressing tax avoidance through the means of disguised remuneration schemes, both existing and future. The aim of these measures is to help ensure that users pay their fair share of Income Tax and National Insurance Contributions (NICs).

In the Finance Bill 2017-18, the Government will legislate to:

- introduce the close companies gateway, which is intended to clarify when Part 7A of Income Tax (Earnings and Pensions) Act 2003 (ITEPA 2003) applies to the remuneration of owners of close companies and tackle cases where it is felt that remuneration is not being paid in connection with employment;

- require all employees and self-employed individuals who have received a disguised remuneration loan to provide information to HMRC by 1 October 2019, thereby assisting HMRC in ensuring that the new charge on loans made after 5 April 1999 is complied with;

- ensure that, where the employer is located offshore, the liabilities arising from the new loan charge are collected from the appropriate person (a concept to be clarified in the legislation); and

- clarify and ensure that, with effect from today (22 November 2017), Part 7A of ITEPA 2003 applies regardless of whether contributions to disguised remuneration avoidance schemes should previously have been taxed as employment income.

These announcements follow HMRC's success earlier this year in the Rangers Football Club case, in which the Supreme Court ruled that income tax will be charged on all remuneration, regardless of whether or not it is paid directly to the employee or to a third party. It was held that contributions to an EBT (rather than to the players of the club) which were then directed into a number of sub-trusts belonging to each player, did in fact represent remuneration for employment. It seems inevitable that HMRC will continue to build on their success in this case, which has furnished them with the tools to progress their efforts in this area and arguably broadened their interpretation as to what may be captured by the definition of "disguised remuneration".

VAT

VAT threshold

The VAT registration and deregistration thresholds will stay at £85,000 and £83,000 respectively until April 2020.

Online marketplaces

Online marketplaces will be jointly and severally liable for VAT with the sellers of the goods in two circumstances:

- In respect of UK sellers, online marketplaces will be liable provided HMRC has notified the online marketplace.

- In respect of non-UK sellers, online marketplaces will be liable if the online marketplace knew or should have known that the seller should have been registered for VAT in the UK but in fact was not.

Online marketplaces will also be required to ensure the validity of a seller's VAT number and to display this number on their platform. These requirements will be supported by a regulatory penalty.

As regards future measures, on 1 December 2017, the Government will publish a response to its call for evidence (launched after the Spring Budget 2017) to develop a split payment model in respect of online payments.

Future changes

Threshold: The Government will consult on the design of the VAT threshold but will retain the existing thresholds for the next two years.

Grouping provisions: On 1 December 2017, the Government will publish a summary of responses to its consultation paper on UK VAT grouping provisions.

Labour provision in the construction sector: There will be a technical consultation on draft legislation for a VAT reverse charge in Spring 2018 to shift responsibility for paying VAT from the sub-contractor to the main contractor. The eventual changes will take effect from 1 October 2019.

Vouchers: There will be legislation in the Finance Bill 2018-19 to implement changes to simplify the VAT treatment of vouchers, including the point at which they will become subject to VAT, and their value for VAT purposes. The eventual changes will take effect from 1 January 2019.

OTS review: The Government has written to the Office of Tax Simplification (OTS) setting out how the Government will respond to the OTS's review of the VAT regime, which was published on 7 November 2017.

Many of these future changes are expected to take effect post-Brexit, when it is assumed the UK will have greater policy freedom over VAT matters without the current constraints imposed by EU law.

Tightening of the screw – business tax changes

Another withholding tax change?

The government will consult on a proposed extension of UK withholding tax on royalties, intended to take effect from April 2019. As the consultation document is yet to be published, the principal clue was in the Chancellor's speech to the effect that it was aimed at royalties derived from UK sales flowing into tax havens where they are not (or are only lightly) taxed. His comments were in the context of multinationals avoiding tax and he suggested the measures might raise £200m.

As with all anti-avoidance measures the concern will be the impact of whatever new rules emerge on unintended targets, not just multinationals, or more types of royalty income. Existing royalty payers under long-term contracts may wish to examine who bears the risk of new taxes being introduced – the licensor or the payer? – and parties negotiating new agreements or renewing existing deals should consider allocating the tax risk.

Double Tax Relief

One of the target areas for tax reform has been the phenomenon of 'double tax relief' where tax relief provisions intended to prevent a cross-border transaction from being taxed twice (in each relevant jurisdiction) actually apply twice, with the result that the transaction is not taxed at all. A draft measure in the Finance Bill 2018/19 (which is proposed to take effect from today) will prevent a company which has an overseas permanent establishment ("PE") from claiming a tax deduction for a business cost incurred by the PE if the company has already received overseas relief in respect of that business cost.

This change is in line with the general trend towards making tax reliefs more targeted, and so should not come as a shock, but businesses with overseas PEs may wish to review their corporate structures to ensure they do not lose a tax deduction unexpectedly.

Corporation Tax Indexation Allowance

When companies dispose of capital assets and subsequently calculate their chargeable gains, they are currently allowed to take into account the cost of inflation by using an 'indexation allowance' based on the RPI between the date of acquisition and disposal. The Finance Bill 2018/19 (which will take effect from 1 January 2018) will freeze the indexation allowance as at December 2017. This change will mean that companies will start to pay corporation tax on inflationary gains when selling capital assets at a profit. This tax raising measure is expected to start small (raising an estimated £30m of additional tax in 2017/18) but is projected to raise more than £500m a year by 2022/23.

This change may have been introduced to harmonise the corporation tax and capital gains tax ("CGT") rules in the context of the proposed consultation on bringing immovable property disposals within the corporation tax net. Without this change, the corporation tax rules were more generous to the taxpayer than the CGT rules are. This will be an unwelcome change for businesses, although current low rates of inflation will soften the blow. Companies should seek tax advice before disposing of significant business assets as many reliefs remain available, particularly for trading assets.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.