- within Insolvency/Bankruptcy/Re-Structuring, Strategy and Law Department Performance topic(s)

M&A in 2026: a market defined by strategic focus, geopolitical pressures, and regulatory shifts

The first six months of the year saw strong M&A values but fewer transactions as the conflict in the Middle East weighed on activity. Rather than terminating deals, parties instead delayed them in anticipation of an end to hostilities, and processes in the second half of the year will be influenced by the trajectory of relations between the U.S. and Iran. In our latest edition of M&A insights we explore the themes shaping dealmaking across the world, including an uptick in carveouts by corporates and the enduring influence of Middle Eastern sovereign investors.

In brief

- Strategic buyers are a primary driver of current M&A, with corporates pursuing scale, resilience and portfolio optimization through acquisitions and carve-outs. DZ Capital is flowing into assets linked to strategic resilience, including defense, renewables, critical minerals and AI infrastructure. DZ Regulatory change continues to shape deal strategy across the U.S., EU and Australia, with antitrust, foreign subsidies, FDI and tax reforms affecting timing and execution.

During the first six months of 2026, global M&A activity was distinctly “K-shaped”, with a split between robust deal values and falling transaction volumes. A combination of war in the Middle East, supply chain disruptions and sticky interest rates served to lengthen deal timelines without derailing transactions, particularly those with strong strategic rationales.

The pattern across the world is one of more selective activity, as boards, sovereign investors and corporate acquirors continue to pursue deals with compelling industrial objectives. Against this backdrop, carve-outs are gaining momentum, while private equity (PE) firms remain active despite continued pricing mismatches between buyers and sellers. With that said, in Europe we are seeing greater caution among PE investment committees when it comes to new investments, while financial sponsors globally are leaning harder on continuation vehicles and secondary buyouts to exit assets that have often been held for a considerable time.

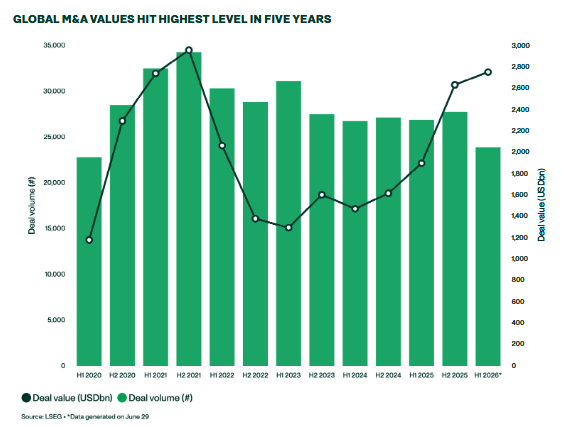

VALUES HOLD FIRM WHILE DEAL VOLUMES FALL

Global M&A values in the year to June reached USD2.8 trillion, the highest half-year total since H2 2021. However, deal volumes were down 14% compared to H2 2025, with the number of transactions in Q2 (10.309) representing the lowest quarterly count since the turn of the decade.

The headline figures across major regions largely followed a similar pattern. North American M&A by value exceeded USD1.5tn, the highest six-month total in history, although volumes fell 16.2% versus H2 2025 to 6,261 transactions, the lowest deal count this decade. In Europe, deal values hit USD661.5 billion, the highest half-year figure since H2 2021, while volumes fell 17.8% compared to H2 2025.

In Asia Pacific, dealmaking bucked the global trend with values falling 25% to USD433bn and volumes dropping by 6% to 8,672 transactions. Middle Eastern M&A was more resilient at USD45.4bn, up 7% on H2 2025 despite regional instability.

STRATEGIC BUYERS SET THE PACE

Strategic acquirors were a strong driver of activity across regions. Many corporates are looking to dispose of non-core assets amid pressure on revenues, while others are seeking scale to address persistent macro headwinds. In the UK, strategic buyers drove a flight to quality, with U.S./UK public company deals another enduring trend; during the period to June, Unilever’s foods business combination with McCormick and Ingredion’s GBP2.7bn takeover of Tate & Lyle were prime examples.

In North America, high transaction values were heavily influenced by a series of transformational deals, including SpaceX’s USD250bn acquisition of xAI and USD60bn post-IPO buyout of Anysphere, Paramount Skydance’s pending USD111bn acquisition of Warner Bros. Discovery and Devon Energy’s USD58bn merger with Coterra.

VOLATILITY DELAYS DEALS RATHER THAN DERAILING THEM

The U.S./Iran conflict was a drag on market sentiment, but M&A processes across the world were delayed rather than abandoned. The war compounded stubborn inflation and uncertainty around interest rates to widen pricing gaps between buyers and sellers, while in Europe in particular we are seeing a sharper divide between corporates pursuing acquisitions with confidence and financial sponsors that are more hesitant.

CAPITAL IS BEING DEPLOYED SELECTIVELY INTO ASSETS THAT PROMOTE RESILIENCE

From a sector perspective there is growing interest in assets tied to sovereign resilience. Defense and renewable power assets continue to attract significant investor attention in Europe, driven by supply-chain disruption, high energy prices and a more consolidation-friendly EU regulatory environment for domestic businesses.

Mining and critical minerals are a focus in North America and Australia, with buyers pursuing rare earths, lithium and other critical materials amid similar security-of-supply concerns. AI is another clear investment priority in every region, with corporates seeking technology and skills to accelerate their transformation, despite AI- and data-related deals facing heightened pressures amid the global focus on data and technological sovereignty.

The disruption of the European car sector from electric vehicles (EVs) is another prominent driver of M&A, with foreign investors exploring opportunities across the auto supply chain. Chinese EV makers for example are looking to acquire European manufacturing facilities as a hedge against geopolitical uncertainty and a volatile tariff environment.

MIDDLE EASTERN SOVEREIGNS REMAIN IMPORTANT OUTBOUND INVESTORS

As far as cross-border capital flows are concerned, Middle Eastern sovereign investors continue to pursue outbound opportunities, including in China, with their allocations holding steady as those from parties in other jurisdictions have stalled.

Their long-term focus is providing structural support to M&A pipelines globally, with major funds such as PIF and MGX targeting AI and digital infrastructure assets, which in turn is boosting reciprocal investments into the Middle East. Japan remains a hot market for inbound investors from all regions as the weak yen makes Japanese assets relatively cheaper compared to similar opportunities in other markets. The UK, too, remains in focus for foreign acquirors, with USD202bn of inbound M&A in the first six months of the year, the highest figure since H2 2021 and more than double the total for H2 2025.

REGULATION IMPACTS DEAL PROCESSES ACROSS THE WORLD

Regulatory change continues to impact deal strategy and timing. In the U.S., Hart-Scott-Rodino filing requirements remain in flux after changes by the federal antitrust agencies introduced in 2025 were struck down by the courts. Currently parties are using the older, less burdensome form, although the Federal Trade Commission (FTC) is considering fresh reforms that could take effect in 2028. Meanwhile in the EU, the European Commission’s review of European merger guidelines is intended to make consolidation easier for domestic investors, while its enforcement of the Foreign Subsidies Regulation has intensified. In Australia, proposed FDI reforms and changes to the country’s capital gains tax regime have the potential to shape future processes, although the measures remain in draft form.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]