Reprint of an article originally published in Tax Notes International on February 25, 2002

The crisis in the technology sector worldwide has been widely acknowledged. As financing sources dwindle and company valuations brutally cut, the uninitiated might conclude that venture capital investments in technology have all but vanished. The reality is, however, that venture capital still flows into the technology sector, albeit in smaller quantities and with greater prudence. In this new environment, in which continuing financing is not guaranteed and the "exit horizon" is measured in years rather than months, the need for careful tax planning of the investment structure is accentuated.

The Israeli technology sector, still vibrant and innovative, offers many investment opportunities. This article lays forward the general factors that need to be considered when planning an investment in an Israeli technology company and describes several common structures that are used for that purpose.

A. Israeli Taxation of Investments: General Principles

Before dwelling on the specific aspects of venture capital investments, the following provides a short exposition to the general principles governing investment taxation in Israel.

1. The Taxation of Income and Capital Gains

In general, gains realized upon the sale of assets can be treated as either business income or capital gains. When the assets involved are corporate securities, real estate or similar assets that are commonly used for long term investment, the inclination would be to treat the resulting gain as a capital gain. Nevertheless, Israeli courts held more than once that repetitive transactions in investment assets, in which the taxpayer manifests knowledge and expertise and employs a developed infrastructure, will result in classification of the gain as ordinary business income rather than capital gains1.

Ordinary income, of both active (business, vocation or employment) and passive character, is taxable under the Israeli Income Tax Ordinance, 1961 (ITO) if "…accrued in, derived from or received in Israel"2. This territorial scope of the Israeli income tax is broadened in certain situations, for example when income was derived abroad from a business, the management and control of which are exercised in Israel.

Capital gains are taxed under two separate laws: capital gains derived from the sale of real estate located in Israel (including the sale of shares in companies whose main assets are real estate) are taxed under the provisions of the Land Appreciation Tax Law, 1963. Capital gains derived from dispositions in any other asset are taxed under Chapter E of the ITO. In both cases the basis of the taxpayer in the asset sold is indexed to the Consumer Price Index so that the inflationary portion of the nominal capital gain is separated from the real gain. The inflationary gain is taxed at 0%3, whereas the real gain is taxed at the ordinary rates, i.e. up to 50% for individuals and a flat 36% for companies4.

When shares are sold as capital assets, several specific provisions apply in addition to the above: First, the part of the gain relating to undistributed earnings of the company is taxed at the reduced rate of 10%; second, capital gains derived from shares traded in Israel are exempt from tax, and if the shares are traded abroad the capital gain is taxed at the reduced rate of 35%.

Another important feature of the capital gains tax is its geographical scope: As mentioned above, the Israeli international tax system is based on the territorial principle. As a consequence, both residents and non-residents are subject to Israeli tax on capital gains derived from assets located in Israel or rights (direct or indirect) to such assets. In marked deviation from the territorial principle, however, the Ordinance imposes tax on the capital gains of Israeli residents worldwide.

2. Incentives for Capital Investments

Israel offers a wide range of incentives for capital investments, of which only those most relevant to technology companies will be discussed in the present context. The incentives benefiting technology companies are naturally those related to investments in industrial enterprises and in research and development activities.

The Law for the Encouragement of Capital Investments

The Law for the Encouragement of Capital Investments, 1959, offers incentives in the form of government grants, reduced tax rates and tax holidays to "Approved Enterprises", i.e., industrial enterprises recognized by the authorities as contributing to the strengthening of the Israeli industry, producing exports and expanding employment opportunities. Grants of up to 20% of the investment in fixed assets, or, alternatively, tax holidays of up to 10 years, are available to Approved Enterprises, depending on their location5.

All Approved Enterprises enjoy a reduced income tax rate of 25% for a period of 7 years from the first year they derive taxable income6. Furthermore, dividends distributed out of the Approved Enterprise’s income are subject to tax at the rate of 15%, compared with the ordinary rate of 25% applicable to other dividends. Additional tax benefits are granted to companies in which foreigners are invested ("Foreign Investors’ Companies"): these companies enjoy a further reduction in the tax on their income, correlated to the share of foreign investment in their equity. The effective tax rate of these companies is thus as follows:

|

|

Share of Foreign Investors in Equity |

|||

|

|

0%-49% |

49%-74% |

74%-90% |

90%-100% |

|

25% |

20% |

15% |

10% |

|

Tax on Dividends |

15% |

15% |

15% |

15% |

|

Effective Tax Rate |

36.25% |

32% |

27.75% |

23.5% |

Incentives to Research and Development Activities

The Law for the Encouragement of Industrial Research and Development, 1984, offers grants of up to 50% of the R&D outlays to projects approved by the Chief Scientist of the Ministry of Industry and Trade. The grants are repaid in royalties on the sales of products developed in the R&D project7. In addition to the grants under the R&D Law, several bi-national funds offer grants to R&D projects in which enterprises of the two countries participate8. Other paths for R&D financing are the EU’s Framework Programs for Research and Technological Development and EURIKA, in which Israel is a full participant.

Alongside governmental aid in financing R&D activities, the Israeli tax system offers tax incentives to such activities in the form of current deductions. These deductions are available both for enterprises incurring R&D expenses for the development of their own business and for taxpayers participating in the financing of others’ R&D projects, so long that they gain rights to the fruits of such projects9.

B. Israeli Technology Companies: Common Structures

The factors described above influence the business model adopted by Israeli technology companies: The availability of government support to development activities; abundant skilled labor; and labor costs that are significantly lower than in the U.S. – all these favor locating the R&D activities in Israel. Concurrently, the primary market for Israeli technology products is still in the U.S., and U.S. capital markets are by far the most accessible to Israeli companies. Therefore, a U.S. presence is usually required at an early stage. European markets (both for products and for capital) are usually targeted at a later stage. The common traits of the business model result in a relatively homogeneous set of structures for the companies. These structures are described below.

The common structures for technology companies in Israel can be broadly classified into three categories: (i) those involving a U.S. parent and an Israeli subsidiary; (ii) those involving an Israeli parent and a U.S. subsidiary; and (iii) those involving an offshore parent with Israeli and U.S. subsidiaries.

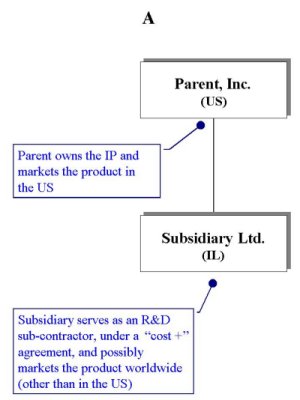

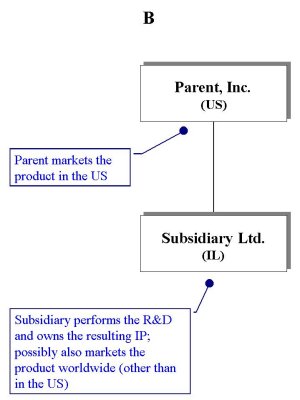

1. U.S. Parent – Israeli Subsidiary Structures

The U.S. parent – Israeli subsidiary structures come in three main variants, deferring in the scope of activities undertaken by each member of the group:

The common feature of all three variants is that the parent of the group, and hence – the company in which the founders and venture capitalists invest, is a U.S. corporation. The experience of many companies has been that U.S. investors prefer an investment in a domestic corporation to a similar investment in a foreign one. Moreover, this structure allows non-U.S. investors to benefit from the fact that the U.S. does not tax foreigners’ capital gains.

As noted above, Israel taxes its residents’ capital gains on a worldwide basis. To defer the potential tax liability for Israeli investors in these structures, Israelis will usually hold their shares in Parent, Inc. through an LLC. The status of LLCs under Israeli tax laws is not yet clear, however the Israeli tax authorities have indicated several times that LLCs will be treated as companies rather than tax-transparent entities. A sale of Parent, Inc.’s shares by the LLC will therefore not trigger Israeli taxation, and the profits will be taxable in Israel only when repatriated10. From the U.S. tax rules’ perspective, the LLC is transparent and the gains will be treated as derived by the ultimate Israeli shareholder.

The three variants entail similar tax consequences for the shareholders, but defer in the tax consequences to the companies involved. Locating the IP in Israel (Structure B) enables the Israeli subsidiary to enjoy the incentives described in section I.2 above, and enables the group to allocate a larger share of its income to Israel, where it is subject to a significantly lower tax rate. The downside of this structure is the potential high Israeli tax liability if the IP itself is sold. Moreover, if the Israeli subsidiary establishes branches outside of Israel, U.S. CFC rules might cause part of the subsidiary’s income to be currently taxed in the United States.

In structures A and C, the Israeli subsidiary acts as an R&D sub-contractor. To qualify as an "Approved Enterprise" under the Law for the Encouragement of Capital Investments, the Israeli subsidiary would have to bill the principal (be it a U.S. entity or an offshore one) on a "cost + 12.5%" basis – a relatively high margin. On the other hand, upon a sale of the IP the Israeli tax is avoided, and the sale will be taxed at the lower capital gains tax rate of the U.S. (in structure A) or the offshore jurisdiction (structure C). Note that if the IP is held by Parent, Inc. (the situation investors prefer for non-tax reasons), a significant share of the group’s income will have to be allocated to the parent and be subject to the U.S. corporate tax rate.

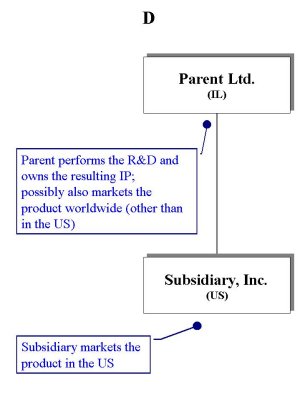

2. Israeli Parent – U.S. Subsidiary Structures

This structure, depicted in drawing D below, allows the company to maximize its use of the "Approved Enterprise" benefits and allocate most of the income to Israel, where it is subject to an effective tax rate of as low as 10%. The main detriment to using this structure is the fact that Israel, as noted above, imposes a tax on non-residents’ capital gains on Israeli stocks. Careful planning and the use of tax treaties can mitigate this exposure, nevertheless the risk may deter potential investors, especially those investing through offshore vehicles.

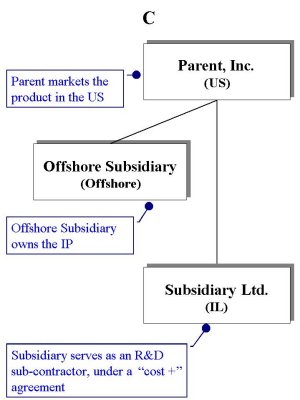

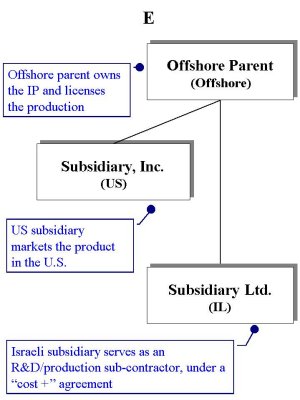

3. Offshore Parent Structures

Under this structure, depicted in drawing E, a parent located in an offshore jurisdiction owns the IP, and sub-contracts the R&D and production activities to the Israeli subsidiary on a "cost plus" basis. Sales are made by the U.S. subsidiary, possibly under a "cost plus" arrangement as well. The benefit of this structure is the low or no tax imposed by the offshore jurisdiction on the income allocated to the parent and on the gain from a sale of the IP. On the other hand, the minimal 12.5% margin required in Israel, as noted above, and the exposure to the risks of redomiciliation (i.e., the Israeli tax authorities claiming that the offshore company is resident in Israel because it is "managed and controlled" therefrom) and permanent establishment claims in the various countries where the products are sold render this structure extremely challenging for the tax planner.

C. Venture Capital Funds: Structuring Israeli Investments

Venture capitalists are a peculiar kind: willing as they are to undertake substantial business risk by investing in young companies at seed and even pre-seed stages, they manifest a distaste to any risk concerning their tax liability. Nonetheless, in cross-border investments such certainty regarding the tax outcomes of an investment structure is hard to achieve, as the following discussion will show.

1. Main Tax Factors Influencing the Structure of Investments

Income Tax Aspects

The dividing line between ordinary income and capital gains, briefly discussed in section I.1 above, plays a key role in the context of VC funds’ investments in Israeli companies. VC funds are usually structured as limited partnerships, in which the fund managers participate as general partners. The Israeli tax authorities take the stance that the fund managers operate a "business of investments", and therefore gains derived from the portfolio are taxable as ordinary income rather than capital gains11. Moreover, since the managers are the active partners in the limited partnership, their business is imputed to the partnership with the result that the whole of its income becomes ordinary rather than capital in character.

Israeli investors in VC funds may not be adversely affected by such recharacterization, given that the tax rate on capital gains is currently equal to that of ordinary income12. Foreign investors and managers, however, might find themselves with a "permanent establishment" in Israel, the income of which is taxable in Israel under most tax treaties. This may have been acceptable if the tax paid in Israel could have been credited against the tax due in the investors’ residence country, however in most cases this is not so: many investors (e.g. pension funds) are exempt from tax in their residence country, and even those that are not will find the tax non-creditable, because the residence country refuses to go along with the recharacterization and continues to treat the profit as a capital gain. The U.S. tax authorities’ position, for example, is that such profits may not be taxed in Israel under the terms of the U.S.-Israeli tax treaty, and hence no credit is allowed for the tax paid.

Some funds choose to avoid the risk of an Israeli permanent establishment through creative planning, while others opt for a ruling from the Israeli tax authorities to mitigate the adverse tax consequences discussed above. Both alternative are presented in the next section.

Value-Added Tax Aspects

Israeli VAT at the rate of 17% is imposed on transactions and services rendered in Israel or with respect to assets located in Israel. Business entities (termed "dealers") are entitled to deduct VAT paid on business inputs ("Inputs VAT") from the VAT owed by them on transactions ("Transactions VAT"). Excess Inputs VAT is refundable, and therefore careful planning for VAT may result in significant cost savings.

The Israeli VAT authorities have issued in 1996 a general ruling with respect to VC funds. Under this ruling, the fund and its management company are recognized as "joint dealers" for VAT purposes, and are allowed to deduct 25% of the Inputs VAT paid by them. This ruling applies to all funds, and no specific ruling request is required.

In considering the utilization of said ruling one should note that such utilization amounts to a representation that the fund and the management company operate a business in Israel, and such representation has bearing on the income tax issues noted previously. Hence, the decision on the VAT position should be taken as part of the general structure of the fund’s Israeli investments.

2. Structures Using the Standard Income Tax Ruling Alternative

In recent years the Israeli income tax authorities have reached an understanding with the VC funds regarding a standard ruling, available upon request, that aims to reduce the uncertainty associated with the tax consequences of a fund’s investments in Israel.

Under the standard ruling, foreign investors that are exempt from tax in their home country on gains from investments enjoy a similar exemption with respect to their share of the fund’s gain from its Israeli investments. Other foreign investors are subject to tax at the reduced rate of 20%. Foreign investors and foreign managers of the fund will not be subject to tax in Israel on gains from non-Israeli investments.

The standard ruling contains several restricting terms, most prominently a requirement that no Israeli residents be among the investors and a minimal requirement for investments in Israel (67.5% of the total investments made by the fund, usually coupled with a minimum amount of no less than $20,000,000).

The main benefits of operating under the ruling are the certainty achieved with respect to the tax consequences in Israel and the exemption granted to tax-exempt foreign investors. The ruling does, however, restrict the investment decisions of the fund and imposes limits on its operations, which funds may find too restrictive. The ruling also fails to address the major problem of characterization misalignment noted above: Foreign tax authorities, most notably in the U.S., continue to view the profits as capital gains that Israel has no right to tax under the applicable tax treaties. The resulting double taxation is somewhat mitigated by the lower tax imposed in Israel, but is not solved. As further discussed in section III below, recent changes have been made to address this issue.

3. Structures Avoiding the Ruling Requirement

The shortcomings of the standard ruling have caused several funds investing in Israel to forego this structure in favor of more complex ones that aim to bypass the Israeli permanent establishment risk. For that purpose, an Israeli company may be used as an advisor to the fund, with no representative powers and no authority to bind the fund. Nonetheless, these structures are exposed to challenge by the tax authorities given the high level of managerial involvement that characterizes VC investments in technology companies.

A compromise solution is the dual fund structure. In this alternative, a twin-fund is established for purposes of investment in Israeli companies. The "Israeli" fund applies for a ruling, however the restrictive terms of such ruling bind only that latter fund and do not effect the operations of the general fund.

D. Recent Changes and the Look Ahead

The crisis in the high-tech sector has not passed over the Israeli technology companies. In an effort to ameliorate the companies’ difficulties in raising financing, the Ministry of Finance has made efforts to address several of the factors that perceivably are the main obstacles to foreign investments in the Israeli technology sector.

1. Recent Changes to the Reorganizations Provisions of the ITO

Amendments introduced in 2000 to the Income Tax Ordinance13 extended the flexibility of the reorganization provisions of the law and introduced new forms of reorganizations. The 2000 legislation also expanded the authority of the Minister of Finance and the Income Tax Commissioner to promulgate regulations and rules governing cases that deviate from the formal requirements prescribed in the law. Based on this legislation, the income tax authorities are now able to better adopt the tax consequences to the specific circumstances of the transactions in question.

2. The Exemption from Tax of Capital Gains from Technology Investments

In September 2001, Israeli Minister of Finance issued a notice according to which foreign investors in Israeli technology companies will be granted an exemption from tax on the income they derive from their investments14. This general statement was followed by an agreement between the Minister and the Israeli Venture Association concerning the implementation of the exemption.

Under the agreement, the exemption from tax is available to foreign investors in funds that meet one of the following conditions ("the Israeli-focused investment test"):

- At least 20%-30% of the aggregate amount raised by the fund (net of management fees and depending on the fund’s first year of operation) is invested in Israeli companies; or

- At least 30% of the aggregate amount raised by the fund is expensed, directly or indirectly, in Israel (as salaries to R&D personnel, rent for the portfolio company, etc.), without accounting for any management fees paid to Israeli managers of the fund.

The exemption is available only under a specific pre-ruling, hence investors in funds operating in "no ruling" structures, discussed in section III.3 above, will not be able to benefit from it. Nonetheless, the exemption form tax removes one of the acute impediments to the ruling alternative, and it is therefore expected that more funds will choose this path in the future.

3. The Look Ahead

The 2000 amendment to the ITO and the newly-granted exemption to foreign investors are important steps at the right direction. In addition, the shift by the Israeli tax authorities from private, unpublished rulings to greater transparency should be encouraged, as it enables investors (and their advisors) to better assess beforehand their position and the likely tax consequences of the structures adopted. Whether these steps are enough to encourage foreign investments in the Israeli technology sector is yet to be seen. According to the Israeli Venture Association, the delay in taking these steps for over a year obstructed some 3 billion dollars of investments. Hopefully, at least part of these sums can now be regained.

1

In a recent case, a lawyer who purchased an apartment and sold it after three years was found to have conducted a business transaction. The holding was based primarily on the significant skill and expertise used in the transaction and the short period of time in which the asset was held. Other factors commonly reviewed by the Israeli courts in considering the character of transactions are the financing used, the existence of a managerial organization and the extent of entrepreneurial and stewardess efforts invested in the asset by the taxpayer.2

The Israeli Income Tax Ordinance, 1961, which is the major Israeli tax legislation, has its roots in the legislation enacted by the British during the mandatory period (1918-1947), hence the term "Ordinance". In 1961 it has been restated into an authoritative Hebrew "New Version" and has been amended numerous times since then.3

Inflationary gains accrued until December 31, 1993, are subject to a 10% tax.4

The tax on real estate capital gains differs from the tax on other capital gains in this issue: The former is imposed on the gain as if it were the taxpayer’s only income (i.e., all the progressive tax brackets are applied), whereas the latter is computed by adding the capital gain on top of the taxpayer’s other income for purposes of applying the brackets.5

The country is divided into three zones, largely concentric to the economic center of Israel – the Tel Aviv metropolitan. The area farthest from the center is "Zone A". The following table summarizes the grants and tax holidays available in the different zones:|

Zone |

Grant (Percentage of Investment) |

Tax Holiday (in years) |

|

A |

20%* |

10 |

|

B |

10% |

6 |

|

C |

-- |

2 |

|

* Zone A enterprises are entitled to a two-year tax holiday in addition to the grant |

||

6

When an Approved Enterprise chooses to enjoy a tax holiday rather than a grant, the 7-years low tax period is proportionally shortened. Hence, for example, Zone B Approved enterprises that elect the 6-years tax holiday will be entitled to an additional one year of low tax rate.7

The royalties are due on a sliding scale of 3% of the sale price of the products during the first three years of sales, 4% during the next three years and 5% thereafter, until the entire amount of the grant is repaid. The project itself is subject to certain limitations, such as a requirement that the production of resulting products be done in Israel and that any resulting intellectual property remain in Israel. Violation of these requirements entails penalties.8

Two examples are the U.S.-Israeli R&D fund ("BIRD-F") and the Canadian-Israeli R&D fund ("CIIRD-F").9

This latter deduction for cost-sharing agreements is limited to projects approved under the R&D Law.10

Israeli CFC rules have been proposed but not yet enacted. Note that, given the territorial focus of the current system, dividends distributed by such LLC and first received outside of Israel will not come within the scope of ITO §2 and therefore will not be subject to tax in Israel.11

As noted above, the main characteristics of a "business" under Israeli tax laws are the frequency of transactions, the utilization of a managerial organization and the employment of knowledge and expertise by the taxpayer. Obviously, these are common traits of VC funds.12

In fact, Israeli investors may find this to their benefit, since the rules for ordinary loss carry-forwards are more flexible than those of capital losses, and any financing expenses may be currently deductible rater than capitalized. On the other hand, if the Israeli company is registered for trade abroad, capital gains are taxed at the reduced rate of 35%.13

For prior coverage see D. Herman, "Taxation of Corporate Reorganizations in Israel: Greater Flexibility in Design, Stricter Enforcement of Implementation", Tax Notes Int’l (May 14, 2001), 2499.14

For prior coverage see D. Herman, "Foreign Investors in Tech Companies Get Capital Gains Exemption", Tax Notes Int’l (October 1, 2001), 32.The content of this article does not constitute legal advice and should not be relied on in that way. Specific advice should be sought about your specific circumstances.

NB This article refers to the law as it stood in February 2002