At the current stage of development of Kazakhstan, raising investment capital for non-resource industry is crucial for economic growth and general national development. In this respect, close attention is paid to national industrialization, namely, the emergence of novel industries, production regions, and goods branded, 'made in Kazakhstan'. To this end, the first special economic zones (SEZs) appeared in 1996, and since 2003, various measures have been introduced to promote investment activities in the form of material investment incentives and State support for projects to create new industries in prioritized economy sectors.

2018 has so far been marked by significant legislative changes, which, among other things, affected investment projects and SEZ taxation. The innovations are undoubtedly favourable as they provide additional opportunities for State support for projects that had been left unaddressed earlier owing to statutory limitations. Evaluation of the novelties in practice is a matter of time and ability of the authorities and business to work side by side.

In this article, we would like to offer an overview of current State measures to support investors with a focus on the changes in legislation in 2018 specifically. In the meantime, the article does not cover State measures to stimulate growth to specific industries, such as agriculture, subsoil use or finance.

What the investor can obtain?

The State offers the following investment incentives and support measures to investors:

1. Import incentive in the form of customs duties and VAT exemptions when importing technological equipment and spare parts thereto as well as raw materials and materials for the end products;

2. State in-kind grants in the form of land plots, buildings, structures and other property (up to 30% of investment);

3. Tax incentives in the form of corporate income tax, property tax and land tax exemptions;

4. Investment grants by reimbursement of actual expenses (not exceeding 30%); and

5. Accelerated tax depreciation of industrial buildings and structures, machinery and equipment.

For State aid, the investor must either launch an investment project or become a SEZ participant. Subject to certain conditions, accelerated tax depreciation can be applied in the absence of an investment contract.

Types of investment projects

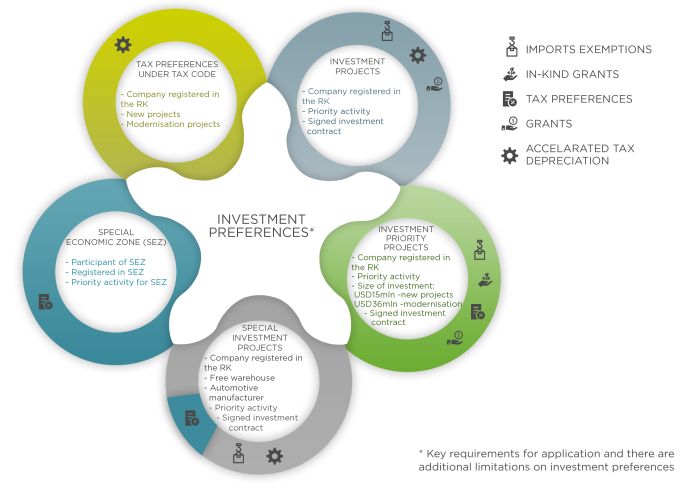

The Business Code determines three major groups of investment projects, each of which has a specific set of requirements and incentives (please see the infographics).

Special investment projects are carried out by SEZ participants, owners of a free warehouse or under contracts for industrial assembly of motor vehicles. For investment incentives, a legal entity must be carrying out a priority activity. Investors implementing special investment projects are given import incentives in the form of import duties and tax exemptions.

Investment projects imply investments that seek to create new production facilities as well as expand and/or update existing production facilities with regards to priority activities. The laws do not set minimum investment requirements for such projects. Under the investment project, the investor can apply import incentives as well as qualify for State in-kind grants.

The most significant incentives are granted to investors who concluded contracts for investment priority projects. Namely, the investor executing such a project is entitled to apply for all types of incentives and support measures, including tax incentives, import incentives, grants and subsidies. However, this does not mean that all types of incentives and support will be provided simultaneously. The set of incentives is determined for each investor individually with due consideration of the balance of interests between the investor and State.Let us have a closer look at the investment priority projects as the main legislative changes are aimed specifically at these projects. Until 2018, only new enterprises could qualify for incentives and only for new production areas. From this year, incentives have been added for projects for the modernization and reconstruction of production if such investments amount to at least 5 million MCI (approx. 36.5 million USD)1. Furthermore, the investor is no longer required to be a newly incorporated legal entity. Now, the existing enterprises can qualify for a contract for an investment priority project for both new production areas (with investments of approximately 15 million USD) and for upgrading production (with investments of 36.5 million USD) with respect to priority activities set for such projects.

Special mention should be made of the issue of priority activities. The list of activities for the implementation of investment priority projects is three times less than the similar list for the implementation of investment and special investment projects. At the same time, all activities for priority projects are on the list for investment projects save for the production of other vehicles and ceramic products. Hence, the analysis of the applicability of investment incentives to a new project requires preliminary review of the lists of activities approved by the Government.

Another significant change is the abolition of the requirement that the income from the investment project should be at least 90% of the total annual income of the legal entity managing the investment project. This innovation adds to the flexibility of the laws as it allows investors to diversify their activities within a single enterprise. Hence follows a new requirement in the tax laws on the conduct of separate accounting for investment projects.

Novelties for SEZ

To date, there are 10 SEZs in Kazakhstan. Each SEZ is focused on the development of certain types of activities. Notwithstanding, all SEZs provide practically identical tax incentives to their participants, including full CIT, land tax and property tax exemptions. Nevertheless, each SEZ has its own features.

With that in mind, an investor should conduct a comparative analysis of the advantages of each SEZ in terms of permissible types of activities, provided incentives and other business factors prior to executing a project to create new production. It is of significance that now, a legal entity must be registered in a SEZ and not only possess an object of taxation.

The SEZ laws have also seen various positive changes. The key change was the elimination of the requirement of a minimum volume in total annual income from the sale of an entity's own goods (90/10 or 70/30). This is certain to contribute to opportunities for the application of incentives in a SEZ, e.g., during the construction period, and will also resolve the issues with control of other types of income pertaining to SEZ participants. Together with the ending of the requirement to observe the ratio, this necessity was introduced to maintain separate records for the priority and other activities.

A number of SEZs themselves saw individual changes, i.e., individual entrepreneurs can now be participants of 'The International Centre for Cross-Border Cooperation, 'Khorgos''. They have the right to reduce income tax by 100%. Further, the SEZ 'Innovative Technology Park' has considerably facilitated conditions for the application of social tax incentives.

How to harness investment incentives?

In order to harness investment incentives, one must file with the competent body an application and supply documents confirming compliance with the requirements. In the case of the competent body's approval, an investment contract is concluded with the provision of investment incentives.

The laws set a 20-business day period for considering an application for investment incentives. The term for signing the investment contract is 10 business days from the date of the decision to grant incentives. However, in practice, the entire process constituting the filing of the application to contract signing can take up to more than six months depending on the entirety of the provided set of documents and other requirements of State bodies.

Beginning in 2018, the application for investment incentives does not require copies of documents justifying the estimated cost of all works and fixed assets, raw materials and materials used for the project. This means that the process of accepting and registering an application may be significantly accelerated, hence approval will also be faster.

The effort involved in the determination of the work programme has also been reduced, and now the work programme is not required to reflect the main production indicators of the project after commissioning. The work programme must reflect just the calendar work schedule for project implementation prior to commissioning. This can also facilitate the process of reconciling data at the application acceptance stage.

In general, the approval process for incentives remains complicated, formalized and demands much of the investors' time and energy. Careful planning and preparation of all supporting documents can aid the process, but even this approach cannot guarantee 20 business days deadline is met.

What comes next?

Prior to applying for investment incentives, the investor should carefully evaluate all opportunities and establish the indicators achievable under the investment project. The terms of the contract should be as realistic and feasible as practically possible. This will provide an opportunity to assess risks and prevent adverse consequences.

In case of failure to fulfil or improper fulfilment of the contractual terms, including the work programme, the competent body and investor, provided that the investor submits documents justifying the possibility of further implementation of the investment project, can. within three months, agree on amending the contract and work programme. However, the investment contract and work programme can be amended by agreement of the parties only once a year. In order to make amendments, the following documents confirming fulfilment of obligations under the investment contract must be provided:

- For works actually performed: tax invoices and customs declarations; and

- For the further period: justification of the estimated costs of construction and installation works along with the costs of acquiring fixed assets, raw materials and (or) materials used in the execution of the investment project.

During the implementation of the investment project, control over compliance with the investment's contractual terms is ensured in the form of a desktop audit and visits to the investment activity site, including review of documents surrounding the implementation of the work programme and the terms of the investment contract. After the conclusion of the investment contract, the legal entity must submit semi-annual reports on the implementation of the investment contract with a proper breakdown according to the cost items determined in the work programme as well as the documents confirming the commissioning of fixed assets, supply and use of spare parts for technological equipment, raw materials and (or) materials.

After the completion of the work programme, the legal entity must submit, within two months, an audit report to the competent investment body. Hence, when carrying out activities under the investment contract and harnessing incentives, one must maintain that all records and internal documentation is in perfect order.

A material risk of investment projects and leveraging incentives is that, in the case of a breach or unilateral termination of the investment contract, whether at the initiative of the investor or the State, all incentives will be cancelled from the start of provision thereof. In this case, the investor will be obliged to calculate and pay all sums and taxes not paid based on investment incentives, and return the received in-kind grants and subsidies.

Additional incentives

Legal entities may, at their own discretion, apply accelerated tax depreciation to industrial buildings and structures newly commissioned in Kazakhstan, machines and equipment as well as during reconstruction and modernization thereof. However, one must take into account the set requirements and limitations for the deadlines of deductions, the timing of commissioning, types of activities and other requirements. These incentives can be used by Kazakhstan legal entities that do not carry out activities under the investment priority project in the absence of an investment contract.

***

In general, we can observe from what has been put forth herein the trend of enhancing laws regulating the investment climate in Kazakhstan. These changes are targeted at removing previously existing barriers and complications in leveraging and applying investment incentives. Such innovations are expected to contribute to raising large amounts of investment capital, which, in turn, will entail the development of infrastructure, the State economy and the social security of the Kazakhstani population.

Footnotes

1 Hereinafter the exchange rate is as of 30 January 2018

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.