- within Antitrust/Competition Law, Consumer Protection and Technology topic(s)

COVID-19 outbreak has far-reaching impacts on the all aspects on our lives and businesses. During the first week of April 2020, Slovak government and parliament worked hard to adopt a first set of measures to help citizens and businesses during the COVID-19 Outbreak. This first set focuses mainly on the most vulnerable – individuals, sole traders and SMEs. Another group of measures aimed at large employers is expected very soon.

Below is an overview of the key measures as adopted by parliament up to 6 April 2020:

1 Employment and social security2 Licences and permits3 Tax and accounting4 Financial aid5 Certain measures in the supervision over financial markets

1 Employment and social security

1.1 Labour Code

During the COVID-19 state of emergency that started on 12 March 2020 (the "COVID-19 pandemic") and two months after its termination, the following specific rules will apply to labour relationships:

1.1.1 employers may order its employees to work from home (if and where possible);

1.1.2 employees have the right to work from home, unless there are serious operational reasons on employer's side to the contrary;

1.1.3 wage compensation payable to employees who must stay at home with no work (so-called "obstacles to work on the side of the employer") due to the COVID-19 pandemic is reduced from 100% of the average wage to 80% (but not less than the statutory minimum wage);

1.1.4 certain notification obligations of employers towards employees are softened, in particular:

(i) the distribution of working time must be announced to the employee at least two days1 in advance (unless a shorter period is agreed);

(ii) taking paid leave must be notified to the employee at least seven days2 in advance (unless a shorter period is agreed);

(iii) taking unused paid leave accrued from the previous year must be notified to the employee two days in advance (unless a shorter period is agreed);

1.1.5 Employers must excuse an employee's absence from work due to quarantine or self-isolation. In such cases, an employee is entitled to "quarantine sick pay" amounting to 55% of his/her average gross salary, paid from the first day of work absence by the state Social Insurance Company (and not by the employer, who would normally cover the first 10 days of sick leave).

1.1.6 Nursing compensation in the amount of 55% of an employee's average gross salary will be paid by state Social Insurance Company for the whole period the employee is taking care of:

(i) a child (max. 11 years old; if disabled max. 18 years old) due to closure of schools and preschools, or

(ii) a relative in case the social service facility taking care of such relative is quarantined or shut down by an order of the relevant state body.

1.1.7 An employee who is quarantined, in isolation or who takes care of relatives described in point 1.1.6 above shall be considered as temporarily unable to work and so should enjoy a higher level of protection under the Labour Code (e.g., prohibition of termination by notice).

1.2 Social security payments by employers and sole traders

1.2.1 Social security payments made by sole traders and by employers (note: not the portion of social security deducted from employees' wages) for the month of March 2020 may be suspended until 31 June 2020, if their turnover falls by more than 40%.

1.2.2 The government is expected to issue a decree with details on the calculation of reduced turnover. The decree may also specify whether a similar social security moratorium shall apply to the following months (April, May, etc.).

1.3 Job retention grants

1.3.1 The government has promised to pay 80% of an employee's salary (up to EUR 1,100 per employee) to employers that have had to close their facilities due to the COVID-19 pandemic.

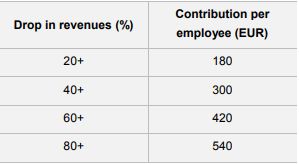

1.3.2 Contributions for employers that have not closed but which recorded a drop in revenues will depend on how much they were affected. The government should contribute as follows3:

1.3.3 Grants will be limited to EUR 200,000 per employer per month and EUR 800,000 per employer in total. Details of the grant payment mechanics and the calculation of reduced turnover are expected to be published shortly.

1.4 Act on Occupational Health and Safety ("OHS")

1.4.1 During the COVID-19 pandemic, employers are not required to notify employees about OHS rules or carry out obligatory OHS trainings if such trainings cannot take place for objective reasons. Lack of training will not be considered as a breach of OHS rules.

1.4.2 Certain deadlines under the OHS Act shall not apply and it shall be sufficient to fulfil the respective obligations within one month following the end of the COVID-19 pandemic. This shall apply for example to the obligation to update various certificates, such as certificates of inspection technicians, certificates for repairs of reserved technical devices, certificates of safety technicians, certificates of authorised safety technicians, certificates of service of technical devices, etc.

2 Licences and permits

2.1 During the COVID-19 pandemic it is possible to suspend trading under a trading licence (in Slovak: ~ivnosť) for up to three years without losing the respective licence.

2.2 The Ministry of Interior and Ministry of Foreign Affairs may limit their capacities dedicated for receiving and processing applications for the issuance of (i) passports (ii) personal ID cards (iii) driving licences (iv) technical documents of vehicles and (v) private security service licences.

2.3 The validity of all residence permits expiring during the COVID-19 pandemic is prolonged until two months after termination of the state of emergency in response to the COVID-19 pandemic.

3 Tax and accounting

3.1 All income and corporate tax returns and tax payments falling due during the COVID-19 pandemic are automatically postponed until the end of the month following the month in which the COVID-19 pandemic ends. Tax must be paid by the same deadline. This suspension however does not apply to payments of regular (monthly or quarterly) tax advances. Advances must still be paid as planned, unless the taxpayer asks the Tax Authority for an individual waiver. In our experience, individual waivers are now granted by the Tax Authorities expediently without much additional questioning.

3.2 No special rules have been introduced for VAT. If taxpayers wish to suspend filing of VAT returns and VAT payments, they may do so and additionally request the Tax Authority for an individual waiver of related penalties. The Tax Authorities have declared that they would be benevolent and acknowledge the COVID-19 pandemic as a justified reason for waiving any such penalties.

3.3 Even if individual waivers under points 3.1 and 3.2 above are not granted by the Tax Authority or requested by the taxpayer, any unpaid tax, tax advance, road tax, withholding and payroll taxes due during the COVID-19 pandemic shall be considered as properly settled if paid by the end of the month following the month in which the COVID-19 pandemic ends. The Tax Authorities will not apply default interest on such late payments.

3.4 Filing payroll tax settlement reports (in Slovak "hlásenie o vyúčtovaní dane"), normally due by the end of April for the previous calendar year, has been suspended until the end of second month following the month in which the COVID-19 pandemic ends.

3.5 The government has also heard the voice of non-profit organisations and has prolonged the deadline to file the declaration on allocation of 2% or 3% of income tax for charity purposes until the end of the month following the month in which the COVID-19 pandemic ends.

3.6 Tax inspections and tax procedures should be postponed upon the subject´s request during the COVID-19 pandemic.

3.7 Tax blacklists published by the Tax Authority (e.g., list of tax debtors) shall not be updated during the COVID-19 pandemic.

3.8 Tax executions shall not take place during the

COVID-19 pandemic.

3.9 Any and all obligations under the Accounting Act (e.g. obligations to keep and file accounts and annual reports, to take inventory, reporting obligations, any many others) shall be deemed to be performed on time if they are met by the earlier of:

3.9.1 the end of the third month following the month in which the COVID-19 pandemic ends, or

3.9.2 the (extended) deadline for filing the relevant tax return to which these accounting obligations relate.

4 Financial aid

4.1 The Ministry of Finance may provide SMEs with financial aid in the form of (i) state guarantees of bank loans or (ii) reimbursement of interest on bank loans.

4.2 Financial aid will be provided to SME employers that have properly paid their tax and social security obligations prior to the COVID-19 pandemic and have no arrears due for more than 180 days. Guarantees will not be available to temporary employment agencies and undertakings in difficulties (under bankruptcy or restructuring proceedings).

4.3 Further conditions for obtaining aid may be stipulated by the bank and/or the Ministry of Finance. The total of the financial aid granted to a single undertaking must not exceed EUR 200,000 over any period of three fiscal years (EUR 20,000 in the agriculture sector).

5 Certain measures in the supervision over financial markets

5.1 The National Bank of Slovakia (the "NBS") may suspend supervision proceedings over financial institutions because of the COVID-19 pandemic.

5.2 The NBS may prolong the statutory deadlines for its decisions (e.g., time to grant prior consent under the Act on Banks, etc.). Any suspended deadlines shall fall due no later than within 30 days following the end of the COVID-19 pandemic.

5.3 Upon reasoned request or on its own initiative, the NBS may prolong the statutory deadlines for the fulfilment of any obligations of supervised financial institutions. However, any suspended deadlines shall fall due no later than within 30 (in extraordinary cases 60) days following the end of the COVID-19 pandemic.

5.4 During the COVID-19 pandemic, supervised financial institutions may deliver requests, applications, appeals and other documentation to the NBS using their electronic mailboxes. Once the COVID-19 pandemic ends, financial institutions will be obliged to deliver hardcopies of documents to the NBS within 30 days.

Footnotes

1. under normal circumstances, one week would apply

2. under normal circumstances, 14 days would apply

3. contributions for March 2020 should be halved

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]