For taxpayers that have bought and sold homes, particularly if they work in construction or real estate, a CRA housing audit is undoubtedly around the corner. The CRA is actively engaged in a house flipper audit blitz and has conducted over 60,000 audits. This has resulted in over $2 billion in taxes and penalties assessed. Further, the CRA has broadened the scope of when a sale will be considered house flipping, deeming all sales within 1 year of purchase a house flipping. Of course, even owning a home for 2, 3, or more years, will not shield a sale from being treated as house flipping. If you or your client is at risk of a house flipping audit, you should take steps to ensure that the proper documents are at the ready.

Why is the CRA on the Hunt for House Flippers?

When an individual sells a home, the home is treated as either a capital sale (e.g. it was personal property) or an inventory sale (e.g. they are builder). Whether the property is capital or inventory, depends on various factors. For example, in determining whether the taxpayer was a builder, the Tax Court of Canada will consider factors such as: i) the taxpayer's intention at the time the property was acquired; ii) the nature of the property; iii) the improvements made by the taxpayer to the property; iv) the length of time the taxpayer owned the property; and v) the frequency and number of transactions carried out by the taxpayer. If the sale is a capital sale, then the capital gain is subject to a 50% income inclusion, unless the principal residence exemption applies. If the sale is an inventory sale, then it is fully taxable and the principal residence exemption cannot apply.

The CRA has determined that taxpayers have been failing to report taxes owing from the sale of houses, by relying on the principal residence exemption, even when they are builders. As such, the CRA has engaged in a housing audit blitz, the assessments from which appear to suggest there was a substantial amount of unreported house flipping. To help its hunt for house flippers, the CRA has heightened reporting obligations. In particular, since 2016, the CRA has required that taxpayers report the sale of real estate (including principal residences) using their individual income tax return.

How has the CRA Broadened the Hunt for House Flippers?

The CRA has now broadened when a sale will be treated house flipping, resulting in automatic tax consequences. In particular, as of 2023, the CRA has established a new residential property flipping rule. Under the new rule, if a taxpayer owns a home for less than 365 days and sells it, then the sale will be deemed an inventory sale and taxed accordingly. Under the rule, the profits cannot be treated as a capital gain (e.g. only subject to a 50% income inclusion) and the principal residence exemption cannot apply. There are limited exceptions for this new rule. These exceptions include where the sale is further to a death, separation, disability or serious illness, the termination of employment, or a bankruptcy.

What Should Taxpayers Do To Prepare for a Potential CRA Housing Audit?

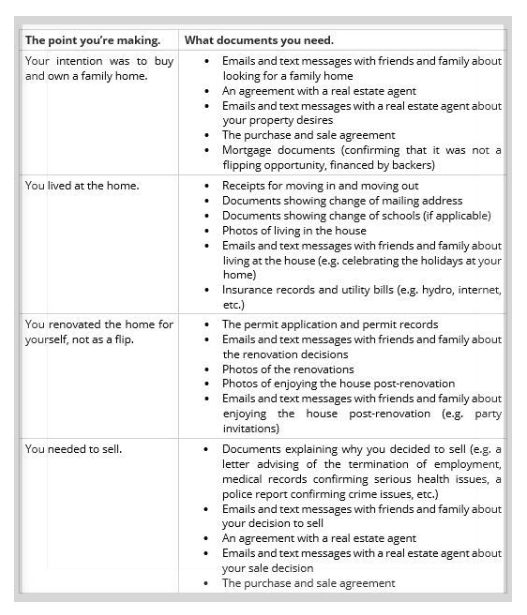

For taxpayers that have bought and sold homes, particularly if they work in the construction or real estate, they should be ready to respond to a CRA housing audit. To that end, they should be prepared to provide the following documents:

When responding to an audit, some taxpayers are tempted to focus on arguing that if they were a builder, they would have spent less on renovations or would have sold the property for more money. This argument is rarely helpful. It is about as effective as defending yourself against murder allegations by writing a book called If I Did It.

In reviewing the above, it is important for taxpayer to be prepared to respond to a CRA housing audit thoughtfully and comprehensively. Otherwise, the taxpayer may be subject to a significant assessment which, if it is issued under the Excise Tax Act further to the taxpayer being a builder, is subject to immediate collection efforts.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.