Review

In 2013, the venture capital market produced a strong performance for the third consecutive year. Financing activity approached the highest level since the end of the dot-com boom, and the number of venture-backed US issuer IPOs was the largest since 2007. Based on activity to date in 2014, both financing and liquidity conditions appear to remain favorable for VC-backed companies.

Financing Activity

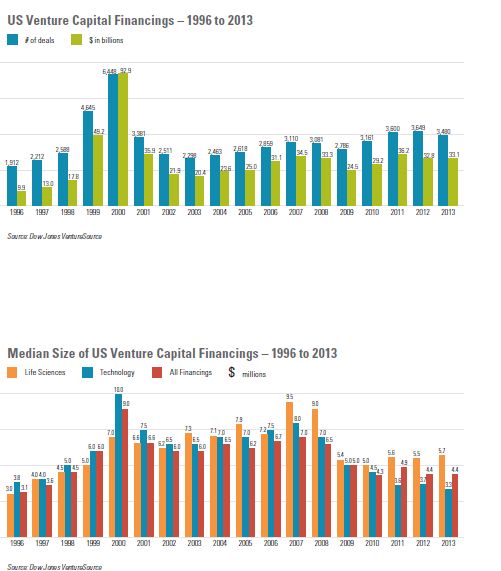

The number of reported venture capital financings dipped 5%, from 3,649 in 2012 to 3,480 in 2013. Despite the normal lag in deal reporting, the tally for 2013 was the third-highest annual total since the collapse of the dot-com bubble. Once all 2013 deals are accounted for, the decline from 2012 is almost certain to be erased and the 2013 count is likely to end up as the highest since the all-butunapproachable total of 6,448 financings in 2000. The quarterly figures of 849, 874, 856 and 901 financings in 2013 are particularly encouraging in light of delayed reporting of some second-half transactions.

Year-over-year, total venture capital financing proceeds inched up 1%, from $32.8 billion in 2012 to $33.1 billion in 2013. The 2013 tally was 14% higher than the average of $29.0 billion in annual gross proceeds over the preceding 10 years, and is likely to increase further after all 2013 financings have been reported.

The median size of all venture capital financings in 2013 was unchanged from the prior year, remaining at $4.4 million. The median size of seed and first-round financings continued to fall in 2013, driven by reduced startup cash needs for many companies due to technological advances as well as the desire of founders to minimize dilution. The median size of seed financings declined from $700,000 in 2012 to $500,000 in 2013, while the median size of first-round financings declined from $2.7 million to $2.5 million. By comparison, in 2005, the median seed financing was $800,000 and the median first-round financing was $5.0 million—twice the amount in 2013.

The median size of second-round financings increased slightly, from $5.4 million in 2012 to $5.7 million in 2013, but fell well short of the $8 million-plus figures that prevailed between 2005 and 2008. The median size of later-stage financings, which has remained steady in recent years, was $10.0 million in 2013—the same amount as in both 2012 and 2005.

The median financing size for life sciences companies ticked up from $5.5 million in 2012 to $5.7 million in 2013, but remained in line with the sector's average since 2009. For technology companies, the median financing size decreased from $3.7 million in 2012 to $3.3 million in 2013. The decline in the median financing size for technology companies in recent years is partly due to technological advances that have enabled startups to commence and grow their operations with a lower level of funding than historically required—in many cases, open-source software and cloud computing have replaced the need to purchase expensive server racks, hire support staff and acquire costly software licenses.

After declining between 2011 and 2012, the number of very large financings increased in 2013. The number of financing rounds of at least $50 million increased from 84 in 2012 to 101 in 2013, and the number of financing rounds of at least $100 million increased from 21 to 28. The largest venture financing of 2013 was completed by Uber ($361 million), followed by Spotify ($250 million) and Pinterest (separate rounds of $225 million and $200 million).

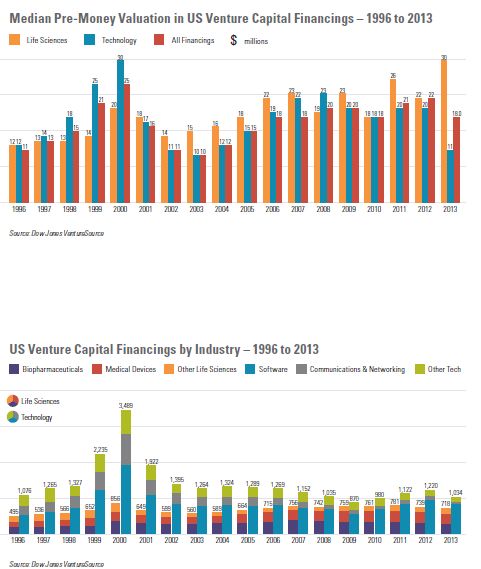

The median pre-money valuation among all venture financings decreased from $22.0 million in 2012 to $18.0 million in 2013, after increasing in each of the two prior years due to strong competition for attractive companies. The median pre-money valuation for financings by life sciences and technology companies— which was comparable in both sectors in 2012—diverged in 2013. Among life sciences companies, the median pre-money valuation increased 34%, from $22.2 million in 2012 to $29.8 million in 2013. Technology companies saw a sharp decline in median pre-money valuation, from $19.8 million in 2012 to $11.0 million, reflecting a large influx of early-stage technology companies seeking financing.

Seed and first-round venture capital financings accounted for 45% of all venture financings in 2013—shy of the 48% in 2012 but higher than any other annual percentage since the 47% figure in 2000. The annual average of 46% of all venture financings accounted for by seed and first-round transactions over the past three years now exceeds the annual average of 45% that prevailed from 1996 to 2000.

Proceeds from seed and first-round deals represented 18% of all venture capital financing proceeds in 2013, down from 21% in 2012. The percentage in both years is well short of the 32% average for the 1996 to 2000 period, reflecting the proliferation of earlystage companies receiving smaller financing amounts and surviving on lower burn rates than historical norms.

Technology companies accounted for 30% of all venture capital financings in 2013, compared to 33% in 2012. After declining for three consecutive years, the market share for life sciences companies increased from 20% in 2012 to 21% in 2013. The next-largest sectors in 2013 were business and financial services (22% market share) and consumer services (20% market share).

California—which has led the country in financings in each year since 1996 (the first year for which this data is available)— accounted for 40% of all venture financings in 2013 (1,389 financings).

New York, home to companies with 349 financings in 2013, finished second in this category for the second year in a row, ahead of Massachusetts with 294 financings. Texas (150 financings) and Pennsylvania (95 financings) rounded out the top five positions for 2013.

Liquidity Activity

With a boost from strong capital market conditions, the number of venture-backed US issuer IPOs increased 39%, from 51 in 2012 to 71 in 2013, continuing the recovery that began in 2010 after VC-backed IPOs had all but disappeared in 2008 and 2009. The largest VC-backed IPO of 2013 was the $1.82 billion offering by Twitter, followed by the IPOs of FireEye ($304 million), Veeva Systems ($261 million), Tableau Software ($254 million) and zulily ($253 million). The median amount of time from initial funding to an IPO decreased from 7.3 years in 2012 to 6.8 years in 2013.

The median amount raised prior to an IPO increased 29%, from $78.4 million in 2012 to $100.9 million in 2013. The median pre-IPO valuation decreased 20%, from $362.2 million in 2012 to $289.3 million in 2013. As a result, the ratio of pre-IPO valuations to the median amount raised prior to an IPO by venture-backed companies going public fell for the second consecutive year, from 4.6:1 in 2012 to 2.9:1 in 2013 (a lower ratio means lower returns to pre-IPO investors). This ratio was between 3.2:1 and 5.5:1 for each year from 2001 to 2012, other than a spike to 9.0:1 in 2009 based on a very small sample size of VC-backed IPOs that year.

To view the full & original text of this article please click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]