- within Employment and HR topic(s)

- with readers working within the Business & Consumer Services industries

The FTA has recently issued a public clarification under UAE VAT law that discusses the Time-frame for recovering Input Tax.We have summarized below the gist of the key UAE VAT positions discussed in the clarification:

- The credit on any procurement made from the vendor is to be

recovered in the first tax period wherein both conditions,

mentioned-below are satisfied as per Article 55(1) of the

Decree-law:

- The tax invoice is received from the vendor; and

- Recipient of procurement pays consideration for the supply or any part thereof

- Further, Article 54(2) of the Executive Regulations make a reference to Article 55(1) of the Decree-law, wherein it has been stated that payment is considered to be made, to the extent person intends to make payment before the expiry of 6 months after the agreed date of payment of supply.

- On a concurrent reading, input tax must be recovered in the

first tax period in which the two conditions are satisfied

- The tax invoice is received; and

- There is an intention to make payment of consideration before the expiry of 6 months after the agreed date of payment;

- The clarification further discusses that once the invoice is received by the taxable person, intention to make payment shall arise only once the internal approval process for payment is completed and forms an intention to actually make the payment within the prescribed time.

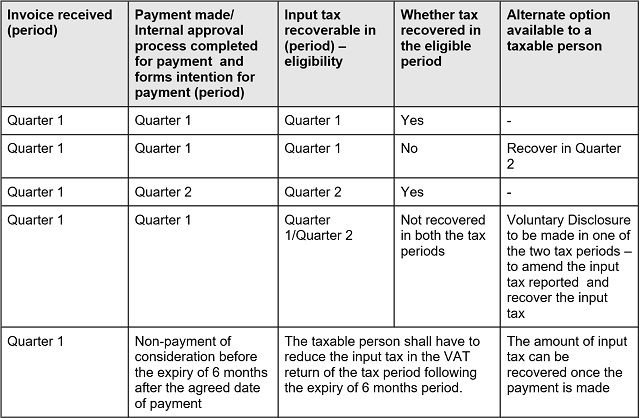

We have tabulated various situations which have been discussed in the clarification with respect to input tax recoverability for ease of understanding

The principles stated above should be used in order to recover input tax as an indicator to analyze the time period within which the Input tax can be recovered. The taxpayer should consider all the facts and circumstances of the transaction on a holistic basis and accordingly recover the input in the period in which the above conditions are satisfied.

Our Comments

1. This public clarification resolves the long-standing ambiguity on the subject matter of recovery of input tax in the case wherein the same is not recovered on account of non-payment/non-receipt of valid Tax invoice as per the VAT law.

2. It is pertinent for Companies to re-look at the input tax recovered in a period wherein the payment has not been made/internal process for payment is not completed, and an intention is not formed actually to make the payment. In case any deviations are observed from the position taken by the company, relevant steps should be taken to discharge appropriate liabilities.

The public clarification can be checked here.

Originally published 5 May, 2020

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]