- in United States

- within Insolvency/Bankruptcy/Re-Structuring, Transport and Corporate/Commercial Law topic(s)

It is an interesting week for businesses and tax professions in the United Arab Emirates ("UAE"), as e-invoicing provisions make a grand entrance into key tax legislations of the UAE. On 30 September 2024, the annexure to the 784th issue of the Official Gazette of the UAE introduced newly issued legislation amending the currently effective Federal Decree-Law No. 28 of 2022 on Tax Procedures ("Tax Procedures Law") and the Federal Decree-Law No. 8 of 2017 on Value-Added Tax ("VAT Law").

This Article aims to shed further light on the amendments recently introduced to the Tax Procedures Law and VAT Law, highlighting the legislative introduction of the e-invoicing regime as incorporated into the UAE tax legislation, as well as other amendments introduced together with e-invoicing provisions.

Amendments to the Tax Procedures Law

The Tax Procedures Law, which has been in effect since 1 March 2023 (being the date it has replaced the former Federal Law No. 7 of 2017 on Tax Procedures), has undergone its first amendment as per the Federal Decree-Law No. 17 of 2024 on Amending Certain Provisions of the Federal Decree-Law No. 28 of 2022 on Tax Procedures.

The new Decree-Law, supposedly effective as of 30 October 2024, introduced a total of five amendments, summarized below:

- Introduction of "e-Invoicing System" as a new defined term within Article 1 of the Tax Procedures Law, covering the issuance and exchange of both tax invoices and tax credit notes.

- Introduction of Article 4 (bis), empowering the Minister of Finance to issue Ministerial Decisions specifying the rules and regulations applicable to the new e-invoicing regime and persons subject to such regime.

- Replacing the title of Chapter One of Title Two of the Tax Procedures Law, previously stating "Keeping of Accounting Records and Commercial Books" with the following text:

"Keeping of Accounting Records and Commercial Books and e-Invoicing System"

- Replacing Article 3 of the Tax Procedures Law, previously stating "The provisions of this Decree-Law shall apply to the procedures related to the administration, collection and enforcement of the Tax Laws and the Administrative Penalties imposed by the Authority for breaching the provisions of this Decree-Law or the Tax Law." with the following text:

"The provisions of this Decree-Law shall apply to the procedures related to the administration and enforcement of the Tax Laws, and the collection of Taxes and Administrative Penalties imposed in accordance with the provisions of this Decree-Law or the Tax Law."

This change appears to be of a substantively insignificant nature. However, it does introduce more accurate wording that better explains the scope of the Tax Procedures Law.

- Replacing the term "obligation" with "tax obligation" wherever mentioned within the Tax Procedures Law. Again, this appears to be of a substantively insignificant nature. However, it does introduce tailored wording for tax purposes.

Amendments to the VAT Law

The VAT Law, which has been amended for the first time back in early 2023, has also undergone its second amendment as per the Federal Decree-Law No. 16 of 2024 on Amending Certain Provisions of the Federal Decree-Law No. 8 of 2017 on Value Added Tax.

The new Decree-Law, supposedly effective as of 30 October 2024, introduced a total of 10 amendments, summarized below:

- Amendments to the definitions of "Tax Invoice" and "Tax Credit Note" to encompass electronic tax invoices and electronic tax credit notes.

- Replacing the definition of the term "Non-Resident" in Article 1, previously stating "Any person who does not own a Place of Establishment or Fixed Establishment in the State and usually does not reside in the State." with the following text:

"Any person who does not have a Place of Establishment or Fixed Establishment in the State and usually does not reside in the State."

This is a key amendment in the sense that a person can now be considered a Non-Resident if they do not 'have' a "Place of Establishment or Fixed Establishment in the State", regardless of the ownership criterion. Accordingly, persons who have a "Place of Establishment or Fixed Establishment in the State" that have previously assumed themselves as falling outside the scope of the term 'Non-Resident' due to non-ownership of such "Place of Establishment or Fixed Establishment in the State" must carefully reassess their tax position in light of the new amendment.

- Introduction of three new defined terms within Article 1, being "e-Invoicing System", "Electronic Invoice", and "Electronic Tax Credit Note".

- Amendments to Articles 55, 65, and 70, for the purposes of incorporating provisions related to the new e-invoicing system.

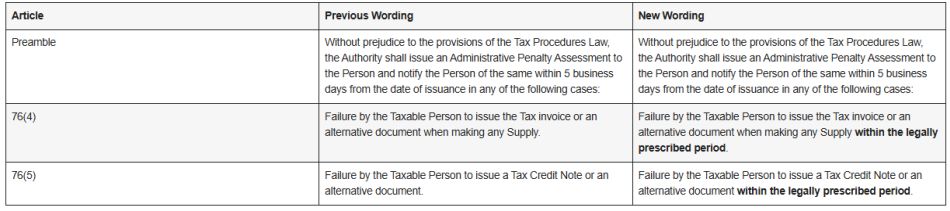

- Amendments to Clauses 4 and 5 of Article 76, as showcased in the table below:

This is a logical change in light of the fact that taxpayers could previously argue that if they have issued a tax invoice or a tax credit note, regardless of whether such issuance was in a timely manner or not, they should not be subject to administrative penalties.

Conclusion

In conclusion, the recent amendments to the Tax Procedures Law and VAT Law mark a significant step in the development of the UAE's taxation framework, particularly with the introduction of e-invoicing provisions. These legislative changes not only clarify existing regulations but also streamline the invoicing process, enhancing compliance and operational efficiency for businesses operating within the UAE. As the effective date of these amendments approaches, it is important for taxpayers to familiarize themselves with the new regulations to ensure compliance and avoid potential penalties. Overall, the integration of e-invoicing represents a progressive move towards a more digitized and transparent tax environment in the UAE, aligning with global best practices and supporting the country's economic growth objectives.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.