- within Finance and Banking, Technology and Criminal Law topic(s)

- with Finance and Tax Executives

- in United States

- with readers working within the Banking & Credit and Securities & Investment industries

Introduction

If the 2008 global financial crisis and subsequent failures of various banks around the world have taught us anything, it is that regulatory capital is pivotal in sustaining the resilience of banks and the overall stability of a country's financial system. The new minimum capital requirements introduced by the Central Bank of Nigeria (CBN) did not therefore entirely come as a surprise to the Nigerian market particularly given that the Governor of the CBN had indicated that this move was in view during the Bankers' Dinner in November 2023.

Twenty years after the minimum capital requirements for banks were last reviewed, the CBN through a circular dated 28 March 2024 has announced an upward review of the minimum capital requirements for commercial, merchant, and non-interest banks in Nigeria (the "Recapitalisation Circular") aimed at strengthening the Nigerian financial system and expressly noted as part of the Nigerian Government's objective to achieve a US$1 trillion economy in gross domestic product (GDP) terms by 2030.

This client alert highlights the significant changes made by the Recapitalisation Circular and the implications for the Nigerian banking sector.

Key Aspects of the Circular & Market Impact

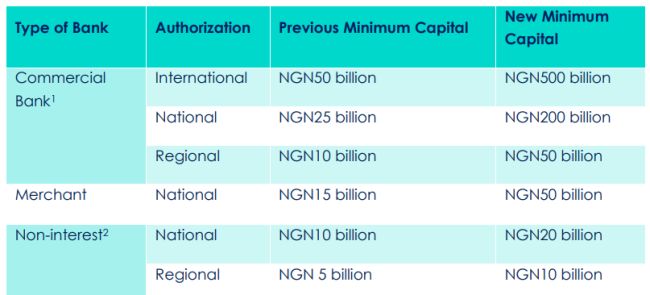

- Minimum Capital Requirements

Referred to as the Banking Sector Recapitalization Programme, the new minimum capital requirements are as follows:

A key concern regarding the new capital requirements – which notably introduce a 900% increase for each of the international and national commercial bank categories – is whether the affected banks are positioned to attract the required capital within the 24 months deadline set by the CBN.

It is estimated that an aggregate of over N4 trillion in fresh capital injection is required to satisfy the new capital requirement and this would by no means be an easy feat. Based on the capital eligibility criteria set by the Recapitalisation Circular, no bank appears to meet the new minimum capital requirement. It is estimated, based on publicly available information, that the eight largest commercial banks in Nigeria will need at least N2.6 trillion in aggregate to meet the 500 billion capital mark whilst six merchant banks are estimated to require approximately N229 billion. Furthermore, at least 20 banks will need to raise more than 100% of their current capital base.

Prior to the Recapitalisation Circular, there were already reports that 17 of the current 24 Deposit Money Banks (DMBs) in Nigeria might struggle to fulfil the CBN new capital requirements if increased by 15-fold from 25 billion. Issuance of the Recapitalisation Circular has not allayed such concerns, and the hard question of whether all banks can realistically achieve this target within the 24 months' timeline has to be addressed.

- Eligible Capital

The Capitalisation Circular mandates that the required minimum capital shall consist solely of paid-in share capital (i.e., paid-up capital and share premium) and that such other components of bank capital as (i) retained profits (ii) other reserves and (iii) even Additional Tier 1 (AT1) capital shall be disregarded for the purpose of meeting the new minimum capital requirements.

From a regulatory perspective, the focus on paid-up capital and share premium only will ensure that the banks have a solid foundation of core capital that is funded directly by shareholders through initial and subsequent share issuances and not through internal capital generation mechanisms which are vulnerable to artificial inflation through internal bookkeeping entries. Furthermore, that retained earnings are not eligible for the purposes of calculating a bank's minimum capital is indicative of the CBN's preference for fresh capital infusion from shareholders, which will enhance the ability of banks to absorb losses with funds that do not need to be repaid and are free of obligations.

The above notwithstanding, there is a concern that the ineligibility of 'other reserves' such as retained earnings and other accumulated profits could limit banks' flexibility for the purposes of meeting the new minimum capital requirements.

Retained earnings are a vital source of capital accumulation, representing profits that can be reinvested to support growth initiatives or cushion against unexpected losses. Therefore, where such accumulated capital is not deemed eligible for the purposes of calculating a bank's minimum capital, this impacts on the ability of several banks (particularly banks that rely heavily on retained earnings for capital reinforcement) to meet the new capital mark. Moving forward, this could also disincentivise banks from maintaining a large pool of retained earnings. Although it is important to note that the Recapitalisation Circular does not exclude retained earnings from being applied towards a bank's overall regulatory capital as relevant reserves will continue to be recognized in the computation and determination of the risk-based capital adequacy ratio (CAR) in line with the CBN's Guidelines on Regulatory Capital.

Given historic events in the Nigerian banking system, the introduction of eligible capital is well understood and to some extent, welcome. However, the Recapitalisation Circular appears in some respect to be a deviation from the CBN Guidelines on Regulatory Capital and by extension the Basel III standards which consider the composition of regulatory capital to include both minimum capital and supplementary capital elements such as additional capital without limiting same to paid up capital and share premium.

In light of the above an argument can be made for a balanced approach which considers both the nature and diversity of capital components, and which could, in the long term, be a better option for structuring minimum capital requirements. For example, many other jurisdictions allow for the inclusion of retained earnings and other reserves as part of minimum capital requirements, albeit subject to certain conditions and limitations such as a requirement for retained earnings to be (i) audited, free from encumbrances, and available for distribution if necessary (ii) limited to a maximum percentage of the total minimum capital to prevent overreliance (iii) subjected to additional regulatory approval upon a financial heath stress test or (iv) subjected to risk based adjustments based on the risk profile of a bank's assets and activities such that banks with higher risk exposures may be required to hold a greater proportion of tangible equity capital relative to retained earnings. This is an approach that the CBN may wish to consider in the near future once this phase of recapitalisation has been completed and the course of the financial system has been corrected.

- Compliance with Existing Capital Adequacy Ratio (CAR)

Requirements

Under the Recapitalisation Circular, Banks are still required to comply with the minimum capital adequacy ratio (CAR) requirement applicable to their license authorization and banks in breach will be required to inject fresh capital to regularize their position. To this extent, regulatory capital as otherwise previously defined and understood will continue to apply for CAR testing purposes.

CAR is a fundamental metric used in assessing a bank's financial health and resilience by testing a bank's capacity to meet liabilities and counteract credit and operational risks effectively. Under extant laws, international banks and Domestic Systemically Important Banks (D-SIBs) are mandated to maintain a CAR of 15%, while other banks, including national and regional ones, must uphold a CAR of 10%.

In view of the CBN's move to ensure that the banking sector is adequately positioned to absorb risks prevalent in its operations in the financial market, this is an important compliance requirement for banks to bear in mind, especially in the face of the new minimum share capital requirements.

- Timeline & Implementation Plan

The CBN has set a timeline of 24 months from 1 of April 2024 and ending on 31 March 2026, and further mandated banks to each submit an Implementation Plan to the Director, Banking Supervision Department, of the CBN for executing compliance with the new minimum capital requirements by 30 April 2024. This Implementation Plan must indicate the bank's desired option(s) and various activities together with timelines for complying with the new minimum capital requirements.

In the forthcoming weeks, it will be imperative for the banks to engage in strategic planning and develop detailed action plans outlining their approach to comply with the newly established capital requirements. This process will involve a thorough assessment of their current capital positions, identification of potential shortfalls, and exploration of viable options which augment their capital base whilst complimenting their long-term strategic objectives. The goal will be to ensure that these financial institutions not only meet the regulatory requirement but also position themselves advantageously for sustainable growth and stability in the evolving banking landscape.

Options Available to Banks

The Recapitalisation Circular recognises three options for banks seeking to comply with the new minimum capital requirements. The options are the (i) injection of fresh capital through private placements, rights issue, and/or offer for subscription; (ii) mergers & acquisitions; and/or (iii) upgrade or downgrade of license authorization.

- Injection of Fresh Capital Through Private Placement,

Rights Issue And / or Offer for Subscription

Subject to the specific means of capital raise adopted by the banks, it appears inevitable that this option will create an avenue for public investors desirous of including bank stocks to their portfolio and more notably, stimulate the Nigerian equity capital markets.

Alternatively, existing shareholders also stand a chance to be issued new shares as a matter of priority where a rights issue is adopted giving them the ability to increase their equity stake.

- Mergers and Acquisitions

The banking industry has witnessed notable mergers and acquisitions over the two decades and whilst in recent times these have been prompted by the expansion drive of a handful of banks, the first wave of bank M&As came about as a result of the 2004 recapitalisation reforms.

Whilst Nigerian banks are largely stronger this time around, we can still expect some M&A activity focused on meeting the new minimum capital requirement rules, likely in the national, regional and merchant bank categories.

In this regard, the CBN has assured the public that in line with extant laws that depositors' accounts and funds will remain secure in the event of an M&A as the acquiring institution will assume responsibility for all liabilities and obligations, including the protection of depositors.

In considering the M&A options, it is worth noting that compliance with the Banks and other Financial Institutions Act 2020 (BOFIA) and rules of the NGX and Securities and Exchange Commission (SEC) for listed banks will come to bear on transaction structuring and timelines. Under the circumstances, it is expected that the CBN will fully cooperate with the banks as necessary to ensure that M&A transactions resulting from the new capital requirements are seamless across the industry.

- Changes to License Authorisation

Banks are also encouraged to explore the option of downgrading their license authorization in order to meet the new minimum capital requirements. Whilst the ability to upgrade has always been available to banks and presents an opportunity for banks within a lower licensing tier to increase their authorisation, the ability to downgrade provides a lifeline for banks that would otherwise struggle to meet the capital requirements but for whom M&A transactions may not be a preferred option. Such banks can now downgrade their authorisation and develop long term strategies for a sustainable capital base under a revised operational platform.

Conclusion

In the next 24 months, it will be interesting to see the various options adopted by the banks to meet the new capital requirements. One notable avenue of exploration will be the resurgence of activities such as public offers, rights issues and private placements within the equity capital markets (ECM) segment of the capital markets which has been largely quiet over the years.

We also expect to see some degree of M&A activity and possibly a couple of downgrades for banks that struggle to attract the required capital timeously.

Footnotes

1. CBN Scope, Conditions & Minimum Standards for Commercial Banks Regulation No. 01 2010 - https://www.cbn.gov.ng/OUT/2010/CIRCULARS/BSD/COMMERCIAL%20BANKING%20LICENSING%20REGULATIONS%20-%20FINAL%20RELEASED.PDF

2. CBN Scope, Conditions & Minimum Standards for Specialized Institutions Regulations No. 3 2010 - https://www.cbn.gov.ng/OUT/2010/CIRCULARS/BSD/REVIEW%20OF%20GUIDELINES%20FOR%20SPECIALISED%20INSTITUTIONS%20- %20FINAL%20RELEASED.PDF

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.