I OVERVIEW OF RESTRUCTURING AND INSOLVENCY ACTIVITY

i Liquidity and State of Financial Markets

As global uncertainties and dynamics impact India, its increasing level of integration with the global economy, continuation of sound domestic policies and structural reforms become important. Being a net commodity importer and making efforts to improve the 'ease of doing business', India stands out among the emerging markets cohort in terms of growth. However, gross fixed capital formation needs to be bolstered, while maintaining robust trends in consumption to sustain higher levels of growth. Retail inflation rose sharply in April 2016 after softening for two months, and this further increased in May 2016. Real fixed investment growth slackened during 2015–2016.

Risks to India's banking sector have increased since last year, mainly on account of a further deterioration in asset quality and low profitability. While the credit and deposit growth of scheduled commercial banks slowed significantly during 2015–2016, their overall capital to risk-weighted assets ratio level increased between September 2015 and March 2016. The risk-weighted assets density declined during this period. The overall credit and deposit growth of banks remained in single digits during the financial year ending March 2016, with a total credit growth of approximately 8.8 per cent, and total deposit growth of 8.1 per cent.

At a time when the banking and financial sector is struggling with growth, the asset quality has further deteriorated. The gross non-performing advances (GNPAs) rose sharply to 7.6 per cent of gross advances in March 2016, from 5.1 per cent in September 2015, largely reflecting reclassification of restructured advances to NPAs following an asset quality review (AQR). Consequently, the overall stressed advances rose only marginally to 11.5 per cent from 11.3 per cent during the period, because of a reduction in restructured standard advances ratio from 6.2 per cent in September 2015 to 3.9 per cent in March 2016. As a result of the prevailing stress, the GNPA ratio may rise from 7.6 per cent in March 2016 to 8.5 per cent by March 2017. The growth of bad loans of Indian banks has further deepened with approximately 80 per cent growth in NPAs during the financial year ending March 2016. If the macro situation deteriorates in the future, the GNPA ratio may increase further to 9.3 per cent by March 2017.

Less-than-expected credit and deposit growth, alongside underperforming industry output and persistently higher inflation rates has led to a tight liquidity situation. This has resulted in a spike in interest rates for short-term papers towards the close of the financial year. The 91-day T-bill auctioned by the Reserve Bank of India (RBI) in December 2015 was sold at 7.2274 per cent, the returns on which increased to 7.3–7.35 per cent by March 2016. Three-month MIBOR during March 2016 prevailed at around 8.2–8.35 per cent, which was much higher than the average return-on-debt funds. Such liquidity pressures and their causes have stretched the asset liability management of certain banks, as has the reluctance of some of the cash-surplus banks to lend money to the needy ones (source: RBI Financial Stability Report – June 2016).

ii Impact of Specific Regional and Global Events

The volatility of the global markets, including fluctuation in commodities such as oil, metals and agricultural produce, has affected the prospects of growth and profitability of domestic Indian entities. Other than these, geo-political situations like sovereign debt crisis in Europe, Chinese slowdown and, more recently, 'Brexit' have had substantial impact on the Indian markets as well.

Domestic factors, such as legal hurdles in implementation of infrastructure projects, lack of majority with ruling Government to pass necessary legislations in Parliament and non-transparent fuel-pricing structures have also been some of the imperative factors affecting the growth prospects of the domestic sector.

The referendum in the UK in June 2016 that decided upon the exit of the UK from the European Union has come as more of a surprise to the markets than a setback for growth prospects. This has further fueled speculation of other member States potentially following the path of the UK. The foreign exchange markets have already skewed towards a stronger euro on the back of the pronounced exit of the UK from the EU. The pound sterling has fallen by as much as 10 per cent against the rupee since the day the referendum result was announced.

The manufacturing set-ups of the UK are already worried about possible sanctions that may be imposed against free movement of goods and services from and to the UK from the EU. Indian companies that have invested very heavily in the UK have already started to feel the pinch of a weaker UK economy and the possibility of a further recession. The Bank of England has already indicated a potential reduction in the rate of interest, from the present 0.5 per cent to around 0.25 per cent.

As far as impact on India is concerned, data from the Ministry of Commerce and Industry reflects that India's bilateral trade with the UK was worth US$14.02 billion in the financial year 2015–2016, out of which, US$8.83 billion was exports and US$5.19 billion was imports. The trade balance was thus a positive of around US$3.64 billion. The event of the UK leaving the EU may actually strengthen India's position, as a truncated EU will have to rework its negotiation strategy to gain market access. Further, it has to be kept in mind that it is highly unlikely that the UK financial markets and its financial expertise will evaporate overnight.

iii Market Trends in Restructuring Procedures and Techniques

As a result of increased deterioration in asset quality, the restructuring of corporate loans is on the rise in India, and the rising level of debt restructuring is a cause of concern for the banking sector and the economy as a whole.

The broad regulatory approach of the RBI over the past few years has been on supporting and strengthening the banking sector through measures aimed at enhancing credit discipline, addressing asset quality issues, encouraging market access, enabling earlier recognition of stress, offering appropriate solutions, improving corporate governance and create strategies to augment capital. In July 2014, the RBI introduced a flexible financing scheme allowing banks to extend long-term loans of 20–25 years to match the cash flows of projects while refinancing them every five or seven years (popularly known as the '5–25 scheme').

The corporate debt restructuring (CDR) mechanism set up with the objective to 'amicably and collectively evolve policies and guidelines for working out debt restructuring plans in the interests of all concerned' has not yielded the desired level of success, which is evident from the increasing number of failed cases, as the CDR largely rested on deferment of liability. The rising number of failures does not augur well for the banking as well as the corporate sector.

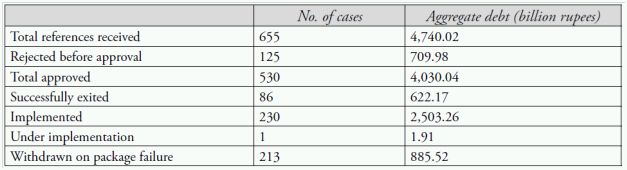

Recognising the moral hazard in perpetuating regulatory forbearance, the RBI removed the distinction between restructured and non-performing assets, effective as of 1st April 2015. Recent trends in the number of cases and aggregate amount of debt referred and approved under the CDR cell shows the effect of withdrawal of regulatory forbearance on restructuring, especially with respect to large credit accounts.

March 2016, there has been no new reference in the year 2015–2016 as the lenders have resorted to alternative mechanisms of restructuring rather than CDR.

Source: CDR Cell – Progress Report as on 31st March 2016, www.cdrindia.org.

The revised framework of the Joint Lenders Forum (JLF), along with the Central Repository of Information on Large Credits, aims to address these issues by incentivising early identification of problems, timely restructuring of loans that are viable and taking prompt steps for recovery or sale if they are found to be unviable. Alongside this, the asset reconstruction companies (ARCs) have been permitted to consider an extended resolution period of eight years, subject to certain conditions, with respect to stressed assets that are under a restructuring proposal approved by the Board for Industrial and Financial Reconstruction (BIFR), CDR or JLF.

In June 2015, the RBI promulgated the Strategic Debt Restructuring mechanism (SDR) permitting the lenders to have a controlling stake in the borrower company by converting their debt into equity with a view to enabling a change of management in the borrower companies, when operational or managerial inefficiencies are observed to be one of the reasons behind the continuation or aggravation in the stress being felt at the borrower company. As per the Religare report, until March 2016, the total number of cases under the Strategic Debt Restructuring Mechanism was 17, with an aggregate debt of around 1 trillion rupees, and the number is expected to increase to around 1.5 trillion rupees, or even more, by the end of March 2017.

Further, in June 2016, RBI came up with a new concept of sustainable restructuring by slightly tweaking the existing concept of SDR. The new guidelines laid out the broad parameters of reduction of the already existing debt size to a sustainable level, and called it the 'S4A Restructuring scheme'. To date, one company with an aggregate exposure of 4.9 billion rupees has been successfully restructured under the S4A mechanism, with many more expected to follow.

Because of the continued domestic economic weakness and the liquidity crunch, there has been a surge in matters being referred for restructuring before the BIFR. Compared with the total of 91 cases registered with the BIFR during 2014, the number increased stupendously to 186 in 2015, and 91 cases have already been registered in the first half of 2016 (source: www.bifr.nic.in). The steep increase in numbers is a clear reflection of stress in the corporate sector and the dire need for an effective financial and corporate restructuring.

II GENERAL INTRODUCTION TO THE FORMAL INSOLVENCY AND RESTRUCTURING PROCEDURES

The legal framework in India to deal with the insolvency and restructuring procedures of corporates, partnership firms and individuals is under transition. Post-enactment of the Insolvency and Bankruptcy Code (IBC) in May 2016 paves the way for the complete overhaul of the insolvency and bankruptcy mechanism in India. However, this is pending notification by the Central Government and shall come into force from the date of its notification.

Presently, there is no single comprehensive and integrated law to deal with corporate insolvency and restructuring in India. In fact, it is dealt with fragmented laws operating in various spheres. The insolvency and restructuring framework in India is majorly guided by the Companies Act 1956/2013 and the Sick Industrial Companies (Special Provisions) Act 1985 (SICA)1.

The formal procedure for restructuring encompasses within its ambit: scheme of reconstruction, takeover, mergers, demergers, transfer of undertakings and restructuring of debts as provided in Sections 391–392 of the 1956 Act (Sections 230–231 of the 2013 Act). In addition, a scheme for revival and restructuring of a sick industrial company can also be duly sanctioned by the board2 under the provisions of SICA. The winding-up procedures are governed in accordance with the provisions of the Companies Act 1956/20133, which contain the law relating to winding up through the High Courts.

Companies Act 1956

Chapter V of the Companies Act 1956 lays down the law relating to 'arbitration, compromises, arrangements and reconstructions' of companies in India. It contains the provisions for the compromises, arrangements and reconstructions between the company and its creditors and shareholders. Salient provisions of the Chapter relating to compromises and arrangements are summarised below:

Where a compromise or arrangement is proposed between a company and its creditors, or between a company and its members, the company court having jurisdiction4 may, on application of the company or of any creditor or member of the company (or in the case of a company that is being wound up, of the liquidator) order a meeting of the creditors, or of the members (as the case may be) to be called, held and conducted in such manner as the court directs. If a majority in number representing three-quarters in value of the creditors or members agree to any compromise or arrangement, it will be binding if sanctioned by the court.

The court will not sanction any compromise or arrangement unless it is satisfied that the company, or any other person by whom an application for winding up has been made, has disclosed all material facts relating to the company to the court, such as the latest financial position of the company and the latest auditor's report on its accounts. From the application until the completion of proceedings, the court is empowered to stay the commencement or continuation of any suit or proceeding against the company on such terms as it thinks fit. The court also has the power to supervise and monitor the implementation of any sanctioned compromise or arrangement, and may also modify it if necessary. If the court is of the opinion that a compromise or an arrangement sanctioned earlier cannot be worked satisfactorily with or without modifications, it may pass an order for winding up a company.

Under this Chapter, the court also has the power to issue directions for the transfer of the whole or any part of the undertaking, property or liabilities of any company to a transferee company, where the compromise or arrangement is for the amalgamation of any two or more companies.

Winding up

As per the Companies Act 1956, the company court can order winding up of a registered company if:

- the company has, by a special resolution, resolved that the company be wound up by the court;

- the company commits a default in delivering the statutory report to the Registrar or in holding the statutory meeting;

- the company fails to commence its business within one year of its incorporation, or suspends its business for a whole year and the court is satisfied that there is no intention to carry on the business;

- the number of members falls below the statutory minimum (seven in the case of a public company and two in the case of a private company);

- the company is unable to pay its debts; or

- the court is of the opinion that it is just and equitable that the company be wound up.

The petition for winding up by the court may be made by the company itself, a creditor of the company, a contributory or contributories, the Registrar of Companies, or the Central or any State Government. A creditor of a company can file an application for the winding up of the debtor company for latter's inability to pay its debts.

In the event that a company is wound up by members or creditors without the intervention of the court, it is called a voluntary winding up. It may take place on the passing of an ordinary resolution in the general meeting of its shareholders under certain circumstances and on the passing of a special resolution of the shareholders to wind up voluntarily for any reason whatsoever. Voluntary winding up is possible for solvent companies that are capable of paying their liabilities in full.

A creditor's voluntary winding up is possible for insolvent companies. It requires the holding of meetings of creditors besides that of the members, from the very beginning of the process of the voluntary winding up. It is the creditors who get the right to appoint the liquidator and, hence, the winding-up proceedings are dominated by them.

Chapter XV of the Companies Act 20135

Although much of the procedure is broadly similar to that already existing, some new provisions have been incorporated under the Companies Act 2013, which lay down the procedure for the merger of two or more small companies, between a holding company and its wholly-owned subsidiary, or a prescribed class of companies by giving notice of the proposed arrangement to the Registrar of Companies, the official liquidator or the persons affected by the scheme, and inviting objections thereupon. There is no requirement to convene any creditors' meetings. The scheme must be approved by members of both the transferor and transferee companies (holding 90 per cent of the total number of shares) at a general meeting, and also by 90 per cent in value of the creditors of the respective companies. A copy of the approved scheme has to be filed with the Central Government. On registration, the transferor company is deemed dissolved.

The Act also contains provisions relating to mergers of domestic companies registered under this Act with foreign companies and vice versa. It further states that, subject to the approval of the RBI, the terms and conditions of the merger scheme may provide for payment of consideration to the shareholders of the merging company in cash, partly in cash or partly in Indian depository receipts.

The Sick Industrial Companies (Special Provisions) Act 1985

The Sick Industrial Companies (Special Provisions) Act 1985 (SICA) was enforced in the public interest with a view to securing the timely detection of 'sick' and potentially sick companies owning industrial undertakings. The focus of insolvency legislation in India is currently on reorganisation of the financial and business structure of potentially viable entities facing financial distress so as to allow them to revive and continue their businesses, and on the liquidation of unviable insolvent entities.

Under the provisions of SICA, only medium-sized and large industrial companies in distress can approach the BIFR for formulation of a rescue or revival plan for them. A company entitled to refer its matter for revival to BIFR is termed a 'sick industrial company' (SIC), and the test of its being under distress is balance-sheet based and not default-based6. Small and ancillary industrial undertakings have been specifically excluded from the jurisdiction of SICA and only medium and large scale industrial undertakings fall within its ambit so that focus remains on rescuing the industries in which large resources in terms of capital; human resources, etc. have been deployed.

Proceedings under SICA

A company that becomes a SIC at the end of the financial year is required to file a mandatory referral to the BIFR within 60 days of the finalisation of its accounts for that said financial year at the AGM of its shareholders.

The Act provides that no referral should be made to the BIFR in the event that the financial assets belonging to a company have been acquired by a SC or RC. The Hon'ble Appellate Authority for Industrial and Financial Reconstruction (AAIFR) and the Hon'ble Delhi High Court have, in the matter of M/s Shamken Spinners Ltd, held that 75 per cent or more of the financial assets of a company qualifying as an SIC need to be acquired by an SC or RC before it is referred to the BIFR.

It further provides that where a referral is pending before the BIFR, it will abate if the secured creditors, representing at least 75 per cent in value of the amount outstanding against financial assistance disbursed to the borrower of such secured creditors, have taken any measures to enforce their security under Section 13(4) of the SARFAESI Act 2002.

After receipt of a referral of a company, the BIFR is empowered to make an inquiry into its working to determine whether it has become an SIC, and will declare it such once satisfied. During the period of the inquiry, the BIFR may appoint one or more persons as special directors on the board of the company in order to safeguard the financial and other interests of the company, or the public interest.

Once a company is declared an SIC, the BIFR decides whether it is practicable for it to make its net worth exceed its accumulated losses on its own, within a reasonable period of time, and, if it deems it possible, the BIFR may allow this.

If the BIFR decides that it is not practicable for this to happen, and that it is necessary or expedient in the public interest to revive the company by adoption of various measures for its revival, the BIFR will appoint any secured lender or independent bank as the operating agency to formulate a scheme for the revival of the company.

Said scheme may provide for the financial reconstruction of the SIC, proper management of the SIC by means of a change in or takeover of its management, its amalgamation with any other company, the sale or lease of a part or whole of any of its industrial undertakings, the rationalisation of managerial personnel and employees in accordance with the law, and such other preventive, ameliorative and remedial measures as may be appropriate. These measures may also include a reduction in the interest or rights of the shareholders of the company and the lease of industrial undertakings of the SIC to any person, including cooperative societies formed by the employees.

The scheme prepared by the operating agency is examined by the BIFR and, thereafter, a draft rehabilitation scheme (DRS) is formulated and published by the BIFR seeking suggestions and objections from all concerned. The DRS must also be circulated to the Central Government, State Government, any scheduled or other bank, any public financial institution, state-level institution or any other institution or authority from which any financial assistance has been sought under the DRS, for their consent. For the purpose of the consent of the said parties, 60 days is allowed, which may be extended to further 60 days by the BIFR. The BIFR may, after considering the objections and suggestions of the various parties sanction the scheme for the revival of the company. The implementation of the sanctioned scheme is monitored by the BIFR and a monitoring agency is appointed by the BIFR for the said purpose. In the event that the need so arises, the sanctioned scheme may be modified by the BIFR.

Should the BIFR be of the opinion that the SIC is unlikely to make its net worth exceed its accumulated losses within a reasonable period of time, that it is not likely to become viable in future, or that it is just and equitable that the company be wound up from the BIFR records and forward its opinion to the competent High Court for winding up. Based on this opinion, the court may pass the order and proceed to winding up in accordance with the provisions of the Companies Act 1956.

Throughout proceedings under this Act, no recovery proceedings (including winding-up proceedings) against the company or its guarantors may be initiated or continued, and the BIFR can also issue directions to the SIC that it may not dispose of any of its assets without the permission of the BIFR.

Under Section 22(3) of SICA, the BIFR can also order that any contracts, agreements or other instruments to which the SIC is a party remain suspended, or be carried out as specified by the BIFR. Such an order can initially last up to two years, but may be extended one year at a time up to a maximum of seven years.

The BIFR can also initiate misfeasance proceedings against any managerial persons of the SIC if it appears that they have retained or misappropriated any company assets. It may direct them to repay or restore the money or assets with or without interest to the SIC and report the matter to the Central Government for action against them as it deems fit. The BIFR may also direct public financial institutions, scheduled banks and state‑level institutions not to provide financial assistance to such persons or any companies or other corporate bodies to which they are associated for up to 10 years.

The provisions of SICA override the provisions of all other laws except the provisions of Foreign Exchange Regulation Act 1973 and the Urban (Land) Ceiling and Regulation Act 1976.

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act 2002 (SARFAESI)

Apart from the above two legislations, the provisions regarding resolution of debt through an ARC are contained under the SARFAESI Act, which also deals with foreclosure and aims to enable secured lenders to realise long-term assets, manage problems of liquidity, asset liability mismatches and improve recoveries by exercising powers to take possession of securities, sell them without the intervention of the court, and reduce NPAs by adopting measures for their recovery or reconstruction.

Under the SARFAESI Act, security interests created in favour of any secured creditor may be enforced without the intervention of a court or tribunal. Where any borrower under a liability to a secured creditor under a security agreement defaults in repayment of a secured debt, and its account is classified by the secured creditor as an NPA, the secured creditor may require the borrower by notice in writing to discharge its liabilities in full within 60 days, failing which the creditor is entitled to exercise all or any rights under Section 13(4)7. Upon receiving a notice, no borrower can sell, transfer, or lease the secured assets mentioned in the notice without the consent of the lenders. The secured creditors are empowered to act even in cases pending before the BIFR or with the official liquidator provided 60 per cent or more of the secured lenders are in agreement.

Recovery of Debts Due to Banks and Financial Institutions Act 1993 (RDDB)

The provisions of RDDB are solely directed to enable the banks and financial institutions to recover their debt quickly and efficiently through the debt recovery tribunals (DRTs) under the aegis of the RDDB Act. Under Section 19 of the RDDB Act, banks and financial institutions can file suits for recovery of their dues, known as original applications. After recording of evidence, final arguments are heard and if in order, a decree is passed in favour of the banks or financial institutions.

The DRTs are also the appellate authority for appeals filed against proceedings initiated by secured creditors under the SARFAESI Act.

i Informal Procedures

In addition to the formal insolvency and restructuring procedures available in India, there are also informal procedures for the restructuring of companies facing distress that are driven by the various circulars and guidelines issued by the RBI. The distressed entity may enter into bilateral restructuring with its lenders or it may resort to the CDR mechanism, a voluntary, non-statutory system that allows a financially distressed company with two or more lenders and debts of more than 100 million rupees to restructure its debts with the super-majority consent of its lenders8. Such restructuring is binding on the remaining lenders, provided they are members of the CDR system. The CDR mechanism is based on debtor-creditor agreements (DCAs) and inter-creditor agreements (ICAs), which provide the legal basis for the whole mechanism. Debtors are required to execute a DCA and abide by the terms therein. Similarly, all the lenders participating in the CDR mechanism are required to execute a legally binding agreement among them to agree to abide by the policies and systems of the CDR mechanism. One of the most important clauses of the DCA is the standstill clause, as a result of which, all parties agree not to initiate any legal action against each other, normally for a period of 90 to 180 days. Further, the borrower also undertakes that during the standstill period the loan documents executed in favour of its lenders will be automatically extended without limitation and the borrower will not approach any other forum for similar relief. There will also not be any change in the directorship of the company in as much as this relates to resignation from the board of directors.

Further, in February 2014, the RBI issued guidelines for formation of the JLF in stressed advances before the accounts become NPAs. The RBI also issued guidelines for reporting and classification of stressed accounts, in the same circular, much before the accounts become NPA. As per the circular, accounts (typically those of more than 1 billion rupees) in which delay or irregularity is seen are to be reported and classified as SMA0, SMA1 or SMA2 in different categories of delay.

In case of stressed accounts, the JLF shall take up the formulation of a corrective action plan with the consent of the majority of JLF members. The RBI has also promulgated the Flexi-Restructuring Plan, which enables the banks to lend and restructure debts to infrastructure companies for a longer period of 20–25 years, with an option of refinancing them every five years. Further, with the objective that the shareholders should bear the first loss as compared to lenders, the RBI issued guidelines for effecting 'change of management' by the lenders under the aegis of 'strategic debt restructuring', which enables the lenders to effect a change of management by conversion of their entire or portion of debt into equity of the borrower and thereafter transfer the same in favour of a 'new promoter' within a specified window, and also consider refinancing of debt to the 'new promoter'.

Recently, the RBI came with a 'Scheme for Sustainable Structuring of Stressed Assets' (the S4A scheme) to enable the banks to combat fresh slippages into NPAs, particularly the large borrowers. The scheme is applicable to projects that have commenced commercial production and have an exposure in excess of Rs. 500 crore. The scheme envisages bifurcation of debt into a sustainable level of debt (not below 50 per cent of the aggregate debt facilities) and an unsustainable portion (to be converted into equity or quasi-equity instruments to enable the lenders to enjoy the upside when the borrower turns around). The sustainable portion of the debt is to be ascertained on the basis of its serviceability out of the cash flows of the entity (of the present and the next six months' cash flows) without altering the prevailing payment or repayment stipulations for each existing debt facility. The scheme is intended to provide a fresh lease of life to stressed borrower accounts that have a viable business model.

ii Duties of Directors of Companies in Financial Difficulties

SICA requires that in the event a company is potentially a SIC, its board of directors should bring the fact, along with reasons why, to the notice of the shareholders by convening a meeting, and to the notice of the BIFR by filing a report.

SICA further requires that in the event that a company becomes an SIC, it should make a mandatory referral to the BIFR within 60 days of the date of finalisation of the accounts for the relevant period, seeking adoption of remedial measures necessary for its revival. In a case of non-compliance, the directors of the company are liable for strict penalties.

The directors are further required to give a notice of the appointment of a liquidator of the company at its general meeting to the Registrar of Companies. The directors of the company cease to exercise all powers of the board and, similarly, the managing directors and the other full-time directors also cease to exercise their powers on the appointment of a liquidator for winding up of the company. In the case of a creditors' voluntary winding up, the directors must convene the meeting of the creditors of the company, and at such meeting the directors must present a statement of the position of the company's affairs together with a list of creditors of the company and the estimated amount of the creditors' claims. The directors must file the notice of any resolution passed at the creditors' meeting with the Registrar of Companies.

In the case of winding up by the court, the directors have the duty to defend the company in the winding-up petition filed by the creditor. Each director must file a statement of the state of affairs of the company upon appointment of an official liquidator by courts. The directors also have the duty to assist the official liquidator from time to time by providing relevant information, records and assistance during the process of winding up by the court.

In addition to the above, directors must act honestly, without negligence and in good faith in the bona fide best interests of the company. Directors are further expected to make proper use of their powers, not to fetter their discretion for any reason whatsoever, and must not place themselves in a position in which their personal interest or duties to other persons may conflict with their duties to the companies, except with the informed consent of the company.

Directors are the trustees for the assets of the company handled by them as well as the exercise of the powers vested in them. If they dishonestly or in a mala fide manner exercise their powers and perform their duties, they will be liable for a breach of trust and shall also be required to compensate the company for any loss or damage suffered by it, by reason of such acts committed by them.

As per Section 542 of the Companies Act if, in the course of the winding up of a company, it appears that the business of the company has been carried on with intent to defraud creditors or any other persons, or for any other fraudulent purpose, the court may direct that the person responsible shall be personally liable without any limitation for all or any of the debts or other liabilities of the company as the court may direct.

iii Clawback Actions

As per Section 531 of the Companies Act 1956, the court has the power to declare any act made, taken or done by or against a company in the six months before its winding up, as fraudulent preference of its creditors.. Further, as per Section 531A, any transfer of property or delivery of goods made by a company for an excessive consideration, if made within the year before a petition is made for winding up or passing of a resolution for voluntary winding up of the company, will also be void. The law further provides that in the event of a fraudulent preference, the preferred person will be subject to the same liability and will have the same rights had it undertaken to be personally liable as surety for the debt to the extent of the mortgage or charge on the property or the value of its interest whichever is less.

In the case of a company being wound up, any floating charge on the property of the company created within the 12 months immediately preceding the commencement of the winding up, unless it can be proved that the company was solvent immediately after the creation of the charge, will be invalid9.

The law further provides that in the case of a voluntary winding up, any transfer of shares in the company not being a transfer made to or with the sanction of a liquidator, and any alteration of status of a member of the company made after the commencement of the winding up, shall be void. Similarly, in the case of a winding up by the court, any disposition of property or actionable claims of the company and any transfer of shares in the company or alternation in the status of its members made after the commencement of its winding up shall, unless the court orders otherwise, be void.

III Recent Legal Developments

Parliament has recently passed the crucial Insolvency and Bankruptcy Code 2016 (IBC), which became an Act after the presidential ascent on 28 May 2016. This enactment paves the way for the complete overhaul of the Insolvency and Bankruptcy mechanism in India, which at present is governed primarily through the provisions of SICA and the Companies Act 1956/2013.

Under the IBC, any creditor (whether financial or operational) of the corporate debtor10 may initiate the corporate insolvency resolution process (CIRP) by filing an application with the adjudicating authority (NCLT) for commencing the process of resolution (restructuring or revival) of the corporate debtor. The application for CIRP shall be filed by the financial creditors (u/s 7); by the operational creditor (u/s 9); or by the corporate debtor (u/s 10).

After the filing of the application for the CIRP, the NCLT shall, within a period of 14 days, decide whether to admit or reject the application. The CIRP shall be deemed to have commenced from the date of admission of this application, and the entire process must be completed with 180 days (extendable by 90 days).

Upon commencement of the CIRP, the NCLT11 shall, by an order, declare a moratorium until the completion of the process, prohibiting: the initiation or continuation of any suit or proceeding; the execution of any judgment or decree against the corporate debtor; the disposal or alienation, in any manner, by the corporate debtor of its assets or legal rights or beneficial interest in them; any action by the secured lenders (see u/s 13(4) SARFAESI); and the recovery of any property that is in possession of the corporate debtor, whether or not it is owned by the corporate debtor. However, the declaration of moratorium shall not result in suspension or termination of essential goods or services to the corporate debtor.

Within 14 days of commencement of the CIRP, the NCLT shall appoint an interim resolution professional, as proposed in the application for initiation of the CIRP, and also make a public announcement of the initiation of the CIRP. The NCLT shall also call for submission of claims by the corporate debtor's creditors. From the date of appointment of the interim resolution professional, he or she shall take on the management of affairs of the corporate debtor. The powers of the board of directors and partners of the corporate debtor shall stand suspended.

The interim resolution professional shall collate all the claims received against the corporate debtor and constitute a committee of creditors comprising all the financial creditors of the corporate debtor (irrespective of them being differently secured). As such, there is no concept of class of creditors (first charge/second charge/unsecured) among the financial creditors. The committee of creditors shall, within seven days of its constitution, and with a super-majority vote, resolve to appoint the interim resolution professional as the resolution professional or replace him or her with another resolution professional.

The resolution professional shall manage the affairs of the corporate debtor and also prepare an information memorandum about the corporate debtor in the prescribed manner for the formulation of resolution plans. Any person (called a resolution applicant) can file a resolution plan in response to the information memorandum prepared and circulated by the resolution professional. The resolution plans for the corporate debtor filed by various resolution applicants shall be examined by the resolution professional and placed before the committee of creditors.

A resolution plan, if approved by the committee of creditors (by 75 per cent or more voting share) shall thereafter be approved by the NCLT only if it is found compliant with the requisites of Section 30(4) of the Act (i.e., the provision for payment of dues to the operational creditor is not lower than the amount that the operational creditor would be eligible to receive in the event of liquidation).

If the resolution plan is rejected by the NCLT for non-compliance with the requisites of section 30(4) or no plan is received within the stipulated time frame of 180 days or 270 days, the NCLT may pass orders for the liquidation of the corporate debtor and issue a public announcement to that effect.

The NCLT may also call for the liquidation of the corporate debtor in the event the resolution professional communicates to the tribunal that even during the pendency of the CIRP, the committee of creditors has decided to liquidate the company, or on determination by the tribunal (on an application filed by any person) that the provisions of the resolution plan have been contravened by the corporate debtor. Upon the passing of the order of liquidation of the corporate debtor by the tribunal, the resolution professional shall act as liquidator and receive and collect claims of creditors, verify and accept or reject them accordingly, and run the liquidation process in accordance with the provisions of the IBC.

The IBC also encompasses specific provisions to deal with avoidance of preferential transactions. The transactions eligible for avoidance proceedings are the transfer of property or an interest thereof (two years for preferential transactions entered into with a related party and one year for transactions entered into with a person other than a related party) of the corporate debtor for the benefit of a creditor, guarantor or surety, on account of an antecedent financial debt or operational debt, or other liabilities owed by the corporate debtor that would have the effect of putting such creditor, guarantor or surety in a more beneficial position than it would have been in the event of distribution of assets in the case of the liquidation of such corporate debtor. Under the IBC, upon an application from the creditor, the NCLT may declare any undervalued transaction entered into that is intended to defraud the creditors as void and also reverse its effect. The NCLT may also reverse any transaction entered (within two years from the insolvency commencement date) that may be an extortionate credit in the form of a financial or operational debt.

With effect from 1st June 2016, the Government has notified the relevant sections for establishing the NCLT under the Companies Act 2013, and has accordingly constituted 11 benches of the NCLT, including a principal bench having distinct territorial jurisdiction. After the establishment of NCLTs, the Company Law Board stands dissolved and all matters relating to it shall now be dealt with by the NCLT, along with the adjudication on class action suits, investigation into the company's accounts and freezing of accounts. All appeals against the directions of the NCLT lie with the NCLT instead of the High Court. Those provisions relating to amalgamation, mergers, compromise, settlement, winding up and similar shall continue to remain under the purview of the High Court, which shall be gradually transferred to the NCLT as and when the relevant provisions are notified by the Central Government.

IV Significant Transactions, Key Developments and most Active Industries

In the past, many companies have made referrals to the CDR mechanism, seeking restructuring of their debts. Of the cases approved by CDR before 31 March 2016, the iron and steel sector tops the list with an aggregate debt of approximately 536 billion rupees in 50 cases (accounting for around 21.24 per cent of the total debts restructured under the CDR), followed by the infrastructure sector, with an aggregate debt of approximately 428 billion rupees across 19 cases, and the engineering sector with an aggregate debt of approximately 253 billion rupees across 41 cases. The recession in the economy, coupled with delays in regulatory approvals, resulted in delayed execution of infrastructure projects. Further, an acute shortage of coal and natural gas in conjunction with the increased cost of equipment pursuant to the depreciation in value of the rupee has dealt a huge blow to many power projects. The iron and steel sector has also been hit as a result of the overcapacities created during the boom period, shortage of iron ore (being the main raw material) pursuant to restrictions on mining imposed by the Government of India, cheap imports of Chinese steel and an overall slowdown in the economy leading to depressed demands.

However, post-cessation of regulatory forbearance available to the lenders on restructuring (whereby standard accounts were allowed to retain their asset classification and already-declared NPAs were allowed not to deteriorate to further lower category pursuant to any restructuring), since April 2015 there has been no reference to any new cases reported to the CDR during the year 2015–2016, as the banks have resorted to carrying out other informal modes of restructuring, such as the JLF mechanism, SDR and the S4A schemes.

With the economy not showing signs of a speedy recovery and already stressed financials of most of the banks, withdrawal of this regulatory forbearance will lead to restructured advances getting downgraded requiring banks to set aside more provisions for any anticipated losses in the future.

V International

India has not adopted the UNCITRAL Model Law, and nor do EC Regulations apply to it. As per the provisions of the Companies Act 1956, Indian courts exercise jurisdiction over the winding-up proceedings of all Indian-registered companies, even over their activities outside Indian boundaries. Foreign entities having dues recoverable from said companies may, however, approach the Indian court conducting the winding up, to lodge claims over the estate of the company being wound up.

The law for the recognition of foreign judgments and proceedings is contained in Sections 13 and 44A of the Code of Civil Procedure, which consider foreign judgments in reciprocating territories12 as conclusive, barring certain exceptions, such as fraud or the judgment not being based on the merits of the case. However, a judgment-debtor can only resist the decree-holder by raising any of the grounds under Section 13 of the CPC.

If the decree is of a court in a non-reciprocating foreign territory, a party has to file a fresh civil action (suit) on that foreign decree, or on the original underlying cause of action, or both in a domestic Indian court of competent jurisdiction and at the same time ensure that the parameters of Section 13 of CPC are met. If a foreign decree fall under the limitations subscribed by Section 13 of the CPC, it is not regarded as conclusive as to the matter thereby adjudicated upon. A decree, whether from reciprocating or non-reciprocating territory, that follows a judgment that is not on merits cannot be enforced in India13.

A company incorporated in a foreign country may be wound up as an unregistered company as per the provisions of Sections 583 and 584 of the 1956 Act (Sections 375-376 of the 2013 Act) if it has office and assets in India, and the pendency of a foreign liquidation does not affect the jurisdiction to make winding up orders. The winding up procedure as laid down in Sections 426–483 and 528–559 of the Companies Act (Chapters XX and XXI of the 2013 Act) has to be followed in respect of the assets of the company.

Under the provisions of the IBC, the Central Government may enter into an agreement with the Government of any country outside India for enforcing the provisions of the insolvency code, however, the application of these provisions in relation to assets or property of the corporate debtor or debtors, including a personal guarantor of the corporate debtor, as the case may be, situated at any place in a country outside India with which reciprocal arrangements have been made, shall be subject to such conditions as may be specified.

Despite the existing provisions of the Companies Act and the Code of Civil Procedure, and the induction of certain provisions under the IBC, the Indian laws on cross-border insolvency are inadequate and need to be reviewed to provide a regime conducive to transnational activity in terms of investment and security.

VI Future Developments

On notification of the IBC, cases relating to restructuring and revival, pending before the BIFR or AAIFR shall abate, and new CIRP applications will have to be filed before the NCLT, which is likely to bring about a radical change in the restructuring and rescue process of sick companies in India – a paradigm shift from the prevailing 'debtor-in-possession' era to the 'creditor-in-possession' regime. The code places higher reliance on the commercial wisdom of the creditors and less on judicial intervention. Further, the code brings a significant change in priorities for distribution of liquidation proceeds, with the highest priority being accorded to secured debt, together with the workmen's dues for the immediately preceding 24 months, after meeting the insolvency resolution cost. The sovereign dues rank lower in priority than meeting the claims of workmen, employees and unsecured financial creditors.

It is a comprehensive attempt to try to restructure or revive a company in a time-bound manner of 180–270 days, and if no such corporate restructuring plan is approved or implemented within the stipulated time, then the company will go into liquidation. In the case of liquidation of a corporate debtor, the personal guarantor can also file for and be declared insolvent before the NCLT itself.

Overall, the legal framework in India, with respect to insolvency and reorganization of financially distressed companies, will get a fresh impetus and shall be aligned with best international practices.

NILESH SHARMA

Dhir & Dhir Associates

Nilesh Sharma is a Senior Partner in Dhir & Dhir Associates, Advocates & Solicitors. He is a law graduate and a chartered accountant. He looks after the restructuring and insolvency practice of the firm. His association with the firm and his experience in this practice area is more than two decades. His experience includes providing advisory on restructuring and insolvency issues, negotiated settlements, cross-border insolvency issues, representation before the bankruptcy courts, etc. He is a member of INSOL India and AAIFR BIFR Association of India.

SANDEEP KUMAR GUPTA

Dhir & Dhir Associates

Sandeep Kumar Gupta is a Partner at Dhir & Dhir Associates, Advocates & Solicitors. He is a qualified chartered accountant with an extensive experience of more than two decades in banking, project finance and debt restructuring of entities in distress, both through the CDR mechanism and on bilateral basis. He is a part of the corporate consultancy team of the firm, advising client on matters related to settlements/restructuring with lenders, business and corporate restructuring, including the Strategic Debt Restructuring and S4A mechanisms and other insolvency-related issues.

Footnotes

1 The SICA (Repeal Act) 2002 has already been passed, but it has still not been notified. Along with the notification of the IBC the SICA Repeal Act will also be notified and thereafter the Revival and Rehabilitation of Sick Companies will be governed in terms of the provisions of IBC.

2 Board for Industrial and Financial Reconstruction (BIFR) established in terms of the provisions of Sick Industrial Companies (Special Provisions) Act 1985 (SICA).

3 The Act of 1956 is soon to be scrapped because the Companies Act 2013 has been enacted and 283 Sections of the same have already been notified in the Official Gazette of the Government of India, and are applicable from 1 April 2014. The remaining sections of this Act (including the provisions related to arrangement and compromise and winding up) are yet to be notified. The same shall become effective from the date the same are notified in the Official Gazette of the Government of India.

4 The High Court of the state in which the registered office of the company is situated.

5 Corresponding to Chapter V of the Companies Act 1956.

6 An industrial company that, in addition to fulfilling other prescribed requisites, has at the end of any financial year accumulated losses equal to or exceeding its entire net worth, becomes an SIC.

7 The lender may take possession of the secured assets or the management of the borrower's business and also have the right to transfer same by way of lease, assignment or sale.

8 With the consent of lenders representing 75 per cent or more of its debt in value terms and by 60 per cent of the lenders by numbers.

9 Except to the amount of any cash paid to the company at the time of or subsequent to the creation of, and in consideration for, the charge, together with interest on that amount at the applicable rate.

10 Corporate incorporated under the Companies Act 2013 or earlier Acts and Limited Liability Partnerships incorporated under the LLP act 2000.

12 The adjudicating authority under the IBC.

12 'Reciprocating territory' means any country or territory outside India which the central government may, by notification in the Official Gazette, declare to be a reciprocating territory for the purposes of this section. As notified by the government of India, the following are the reciprocating territories for the purposes of section 44A of the CPC: the United Kingdom, Aden, Republic of Singapore, Federation of Malaya, Trinidad and Tobago, New Zealand and Cook Islands, Hong Kong, Papua and New Guinea, Bangladesh and the United Arab Emirates.

13 Supreme Court of India, in the matter of International Woolen Mills v. Standard Wool (UK) Ltd.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.