Key changes at a glance

Expanding the scope of resolution

- Broader PIA including more institutions within the scope of resolution to reflect local systemic impact;

- To activate insolvency proceedings, NRAs will need to demonstrate that resolution is not the least detrimental option

Clarifying the early intervention framework and MREL calibration

- Removal of the overlaps between early intervention (BRRD) and supervisory measures (CRD);

- Increased cooperation between NCAs and NRAs.

- Clarification of MREL calibration for transfer strategies

Improving the level playing field

- Mandatory use of the least cost test for all types of DGS interventions outside payout of covered deposits in insolvency.

- Resolution must always be preferred if insolvency would be more costly for the DGS.

Strengthening the funding in resolution

- Possibility to use the DGS to bridge the access to the resolution funds under certain conditions;

- DGS can also be used in resolution, for preventive measures or for alternative measures in insolvency.

Amending the hierarchy of claims in insolvency and ensuring depositor preference

- New general depositor preference to replace DGS "super preference";

- Improvement of transparency on financial robustness of DGSs.

Depositor protection

- Extension of the deposit protection to public entities;

- Increased protection for amounts in excess of EUR 100 000 for temporary high balances;

- New equivalent protection for client funds held by non-bank financial institutions.

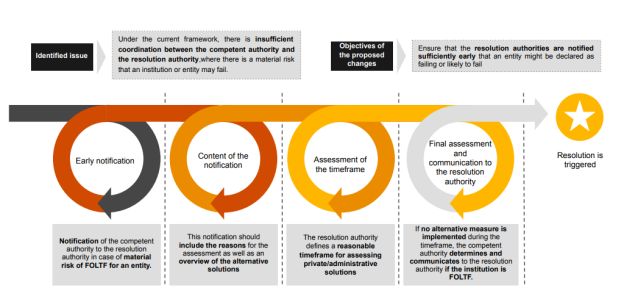

Focus topic: New early warning of failing or likely to fail procedure

Focus topic: Public interest Assessment (PIA)

|

Current functioning of the Public Interest Assessment (PIA) The public interest assessment (PIA) determines whether resolution would have a less severe impact on overall financial stability than 'classic' insolvency proceedings, in particular assessing how each scenario achieves the resolution objectives:

|

Proposed refinements to the resolution objectives

- The criticality of a bank's functions on financial stability will be assessed at regional level (and not only at national level), resulting in a larger number of banks being included within the scope of resolution;

- Resolution authority are required to consider and compare all extraordinary public financial support that can reasonably be expected to be provided in either case. If liquidation aid is expected, this should lead to a positive PIA outcome and trigger resolution;

- Mandatory application of the 'least cost test': resolution must always be preferred if insolvency would be more costly for the DGS.

Proposed procedural changes to the comparison between resolution and national insolvency proceedings

- National insolvency proceedings should be selected as the preferred strategy only when they achieve the framework's objectives better than resolution (and not to the same extent)

| If solvency is elected, NRAs must demonstrate that resolution was not in the public interest. |

Click here to continue reading. . .

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]