The Cayman Islands is one of the leading international centres for the creation and administration of trust structures, and its continued development and growth is due to a number of important factors. The Cayman Islands has a comprehensive Trusts Law, is well known for its innovative Special Trusts Alternative Regime ('STAR'), provides for the registration and licensing of Private Trust Companies ("PTCs"), and offers a range of innovative wealth structuring vehicles. The jurisdiction is also home to some of the most talented and forward thinking trust professionals and advisors.

TRUSTS LAW

In the Cayman Islands, as in England, the law of trusts is not statute-based but primarily grounded in rules of common law and equity.

These are supplemented by local statutes including the Trusts Law (2017 Revision), which incorporates the previously separate statutes the Trusts (Foreign Element) Law, STAR Law and the Trusts (Amendment) (Immediate Effect and Reserved Powers) Law. Other local statutes such as the Fraudulent Dispositions Law and the Perpetuities Law also have a role to play in the administration of trusts.

Cayman Islands' trust law continues to evolve through robust judicial decisions relating to issues that are at the forefront of legal development in this field. The jurisdiction's long-established trust legislation is supported by a strong and independent local judiciary. Private and public sectors are continuously working collaboratively to review and update legislation so it remains current and viable.

TAX NEUTRALITY

The Cayman Islands is a tax neutral jurisdiction. There has never been any direct taxation in the Cayman Islands, the only fiscal impositions being stamp duty and import duty. A trust can be registered as an "Exempted Trust" and obtain an undertaking from the Governor in Cabinet which exempts the trust from risk to future taxation for 50 years.

CATEGORIES OF TRUSTS

The discretionary trust is the most common trust vehicle used in the Cayman Islands, but strict settlements and charitable trusts are also widely used. In addition to traditional wealth planning, where exempted trusts, reserved powers trusts, and forced heirship planning trusts are often used, Cayman Islands' trusts are used extensively in capital markets transactions and structured finance deals.

STAR TRUSTS

A STAR Trust can be established for any purpose, provided it is lawful and not against public policy. It can create innovative trust planning opportunities, and advocates of STAR continue to find new uses for this regime in their planning. There are a number of features that distinguish the STAR provisions from the purpose trust legislation of other jurisdictions.

FEATURES

The objects of a STAR trust may be persons or purposes, the persons may be of any number and the purposes may be of any number or kind, charitable or non-charitable, provided they are lawful and not contrary to public policy.

The rule against perpetuities, which limits other types of trusts in the Cayman Islands to the statutory perpetuity period of 150 years, does not apply to a STAR trust and therefore a STAR trust can have perpetual existence.

The STAR provisions stipulate that a STAR trust is not rendered void by uncertainty as to its objects or mode of execution. It allows the trust deed to give the trustee or any other person power to resolve an uncertainty as to its objects or mode of execution.

The STAR provisions deal comprehensively with the issue of enforcers. They provide that the only persons who have standing to enforce a STAR trust are such persons, whether or not beneficiaries, as are appointed to be enforcers by the terms of the trust deed, or in certain circumstances by order of the court. Therefore beneficiaries who are not enforcers have no right to enforce the trust or to obtain information regarding the trust.

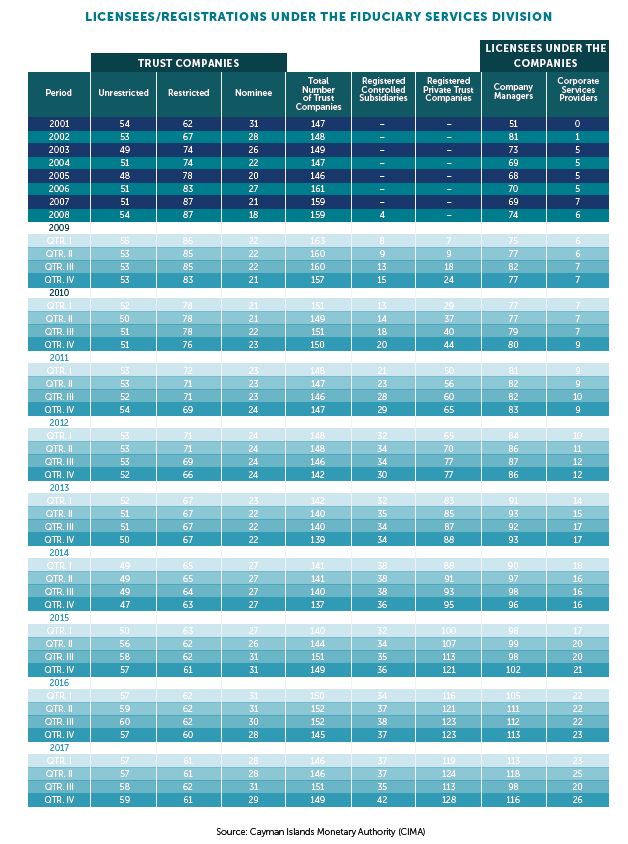

REGULATION

Trust Companies in the Cayman Islands are regulated by the Cayman Islands Monetary Authority ("CIMA") through the various licenses granted and registrations required. Generally, there are two types of licenses granted to trustees carrying on a trust business in Cayman:

- A full trust license entitles the holder to provide trustee services to the public generally.

- A restricted trust license is issued subject to the condition that the trust business is limited to certain named clients. All directors and senior officers of a trustee holding such a licence (including any changes after licensing) must be approved by CIMA.

Trustees and protectors of Cayman Islands trusts must also adhere to the registration requirements of beneficial ownership legislation now in force, and with the reporting requirements provided for in local legislation as part of the international tax information exchange framework established by virtue of FATCA and CRS.

The Cayman Islands has a record of enacting innovative and far-sighted legislation in the wealth management sector, and a wide offering of expert service providers in the Cayman Islands who can assist stakeholders with an efficient and effective strategy to establish or move structures to the jurisdiction.

Contributing to the ongoing evolution of the jurisdiction, new laws providing for the creation of foundation companies were passed in early 2017 and new legislation guiding and regulating non-profit organisations is now in place.

The government continues to demonstrate responsiveness to the needs of the financial services industry, and there is a broad on-going commitment to enact further legislation as needed in the trust arena including in consultation with local professionals.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.