On August 4, 2023, the Department of Finance released an updated version of the draft legislation that will incorporate the excessive interest and financing expense limitation rules ("EIFEL Rules") into the Income Tax Act (Canada) ("Tax Act"). Although they have not yet been passed into law, once implemented, the EIFEL Rules will have retrospective effect – applying to taxation years beginning on or after October 1, 2023.1 Because the EIFEL Rules have not yet been enacted, it is possible that there could be further amendments to them – although our expectation is that they are now in their near final form.

Background

For context, the EIFEL Rules are the Department of Finance's legislative response to the recommendations of the Organization for Economic Co-operation and Development ("OECD") included in its 2015 Action 4 Report ("Report") that was released in connection with its Base Erosion and Profits Shifting Project ("BEPS Project"). In the Report, the OECD expressed concern about the ability of multinational enterprises to use interest and financing expenses to reduce taxable income in high-tax jurisdictions and/or to shift taxable income to low-tax jurisdictions. To address this concern, the Report recommended that countries implement comprehensive earnings stripping rules that would limit a taxpayer's deductible interest and financing expenses to a fixed percentage of its earnings.

The Department of Finance announced its intention to implement this recommendation as part of their 2021 Federal Budget, with draft legislation first being released on February 4, 2022. A revised draft of the EIFEL Rules was released on November 3, 2022, and as noted above, the most recent version of these rules was released in August 2023.

General Rule: Interest and Financing Expenses Limited to 30% of Tax EBITDA

Conceptually, the EIFEL Rules are intended to restrict a taxpayer's ability to deduct interest and certain other financing related expenses to a fixed percentage of the taxpayer's earnings before interest, tax, depreciation and amortization ("EBITDA") with such EBITDA being computed in accordance with Canadian income tax principles. The fixed percentage specified by the EIFEL Rules is 30% (which was at the high-end of the range recommended in the Report) although there is also a limited transitional rule which sets this percentage at 40% for taxation years that begin on or after October 1, 2023, but before January 1, 2024.

The EIFEL Rules do not contain carte blanche exclusions for arrangements that are in place when the rules come into force. As such, existing financing arrangements will need to be carefully reviewed in light of the EIFEL Rules, and all financing arrangements will similarly need to be monitored going-forward.

Interestingly, the EIFEL Rules operate as an accessory regime in that they only apply to interest and financing expenses that are otherwise deductible in accordance with the existing rules in the Tax Act (for example, the general interest deductibility rule and the thin-capitalization provisions). Accordingly, the EIFEL Rules will need to be considered alongside the existing rules in the Tax Act, adding another layer of complexity to an already complex array of rules.

Who Will the EIFEL Rules Apply To?

The EIFEL Rules generally apply to Canadian resident corporations and trusts, as well as to Canadian branches for non-residents, but not to individuals and partnerships. The EIFEL Rules contain special rules that apply to financial institutions, taxpayers that hold interests in partnerships and/or controlled foreign affiliates of Canadian resident taxpayers. Additional provisions operate to exclude from the application of the EIFEL Rules, interest and financing expenses incurred in connection with certain private-public infrastructure projects and inter-affiliate transactions.

The EIFEL Rules do not apply to taxpayers that are excluded entities. An "excluded entity" is comprehensively defined in the EIFEL Rules but, in general terms, includes:

- smaller Canadian-controlled private corporations;

- members of a group having aggregate net interest and financing expenses for the year that are not more than $1,000,000, and

- members of a group that carry on substantially all of their activities in Canada, do not have significant connections to foreign jurisdictions and pay substantially all of their interest and financing expenses to persons that are not tax-indifferent (i.e., tax-exempt entities and non-residents).

As was consistent with the Report, the Department of Finance made it clear in the explanatory notes accompanying the EIFEL Rules that it did not consider excluded entities to pose a significant base erosion and profit shifting threat and therefore were outside the scope of the legislation.

The EIFEL Rules in Detail

The EIFEL Rules are largely mechanical in nature. Its provisions rely on multiple formulae, comprehensively defined terms and, in some instances, accounting concepts. These provisions are supplemented by many detailed anti-avoidance and transitional rules. As a result, when first considered in their entirety, the EIFEL Rules can be quite daunting and difficult to absorb.

The heart of the EIFEL Rules is, not surprisingly, its charging provision which contains a complex formula ("Main Formula") which determines the proportion of a taxpayer's otherwise deductible "interest and financing expenses" that will be denied. In other words, the purpose of the Main Formula is to produce a fraction or percentage that is then used to determine the amount of any resulting expense reductions of the taxpayer. For example, if the Main Formula generates an output of 50% in respect of a taxpayer, then one-half of each of the taxpayer's specified interest and financing expenses will be reduced for the purposes of computing its income for a particular taxation year.

In simplified terms, the Main Formula sets out a fraction, the numerator of which is the aggregate amount of a taxpayer's interest and financing expenses for the taxation year, as reduced by certain amounts, while the denominator is essentially the same aggregate amount of interest and financing expenses but without the reductions. In other words, the adjustments to the numerator determine how much of the taxpayer's interest and financing expenses will be denied (the less significant the adjustments, the more significant the denial). The key variables that reduce the numerator (and thus reduce the fraction or percentage of the expense reduction) of the Main Formula for a particular taxation year are as follows:2

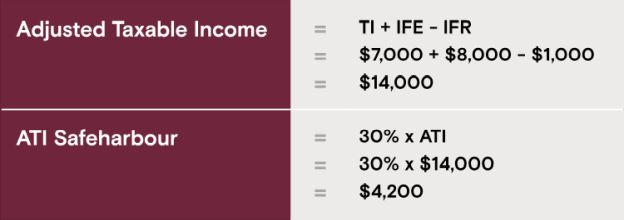

- an amount equal to 30% of the taxpayer's "adjusted taxable income" for the taxation year ("ATI Safeharbour");3

- the taxpayer's "interest and financing revenues" for the taxation year;

- excess capacity carryforwards, if any, from the three prior taxation years of the taxpayer, and

- excess capacity carryforwards, if any, transferred to the taxpayer from eligible affiliates.

A taxpayer's "interest and financing expenses" for a particular taxation year are defined in the EIFEL Rules in great detail. In general terms, they include the taxpayer's interest and financing expenses, capitalized interest, the financing component of certain leases as well as costs and expenses of certain financing related derivatives (such as currency hedges and interest rate swaps). The definition of "interest and financing revenues" is similarly comprehensively defined in the EIFEL Rules but conceptually includes the reciprocal items to those included in the interest and financing expenses definition (such as interest income, income from certain financial leases etc.). Finally, the definition of "adjusted taxable income" has been drafted to capture a taxpayer's "tax EBITDA" for the taxation year calculated in accordance with Canadian income tax rules and concepts. For example, in most cases, the definition of adjusted taxable income starts with a taxpayer's taxable income (determined in accordance with the other rules in the Tax Act) and then adds back certain amounts in respect of capital cost allowance, terminal losses and resource expenditures. The definition then subtracts from the adjusted taxable income computation certain income or revenue amounts such as recaptured capital cost allowance and certain sources of income that are effectively exempt from Canadian income tax (including via the application of foreign tax credits).

To the extent that the application of the EIFEL Rules in a particular taxation year results in the denial of a portion of a taxpayer's interest and financing expenses that would otherwise be tax-deductible for that taxation year, the aggregate of all such denied amounts generally becomes a "restricted interest and financing expense" of the taxpayer. Such restricted interest and financing expenses can generally be carried forward indefinitely by the taxpayer and deducted in the computation of its taxable income in subsequent taxation years where the taxpayer has excess deduction capacity (see below).

In cases where a taxpayer's actual interest and financing expenses for a particular taxation year are less than the maximum of what it could have incurred without triggering the application of the Main Formula, the taxpayer has "excess deduction capacity" (i.e., it could have incurred additional tax-deductible expenses without restriction).4 In such circumstances, the EIFEL Rules contain provisions which enable the taxpayer to either: (i) use this excess deduction capacity in one or more of its three following taxation years so as to eliminate the application of the Main Formula in those other years,5 or (ii) transfer such excess deduction capacity to an affiliate so that it is able to eliminate the application of the Main Formula to it for that taxation year. Note that the EIFEL Rules effectively contain ordering provisions which require (or at least motivate) a taxpayer that has excess deduction capacity in a particular taxation year to use such capacity to absorb its existing restricted interest and financing expenses before it is able to: (i) carry forward such capacity for use in its future taxation years, or (ii) transfer such excess capacity to an affiliate.6

Finally, the EIFEL Rules also include provisions under which certain taxpayers can elect to use an amount determined by a group ratio rule to replace the ATI Safeharbour amount in the Main Formula. In general terms, this election is available to taxpayers that are members of consolidated groups for financial reporting purposes in cases where the ratio of the consolidated group's net third-party interest and financing expenses to the group's book EBITDA implies that a higher deduction limit (relative to that provided by the ATI Safeharbour) would be appropriate. The consolidated group for these purposes would generally encompass all of the entities that are fully consolidated into a parent entity's audited consolidated financial statements.

Simplified Example

The basic operation of the EIFEL Rules is perhaps best illustrated with example. Consider the following simplified fact pattern. A Canadian resident corporation ("Canco") carries on an active business in Canada and, in a particular taxation year, Canco has: (i) taxable income ("TI") of $7,000; (ii) interest and financing expenses ("IFE") of $8,000, and (iii) interest and financing revenues ("IFR") of $1,000. Canco does not have any affiliates nor does it have any unused excess capacity carryforwards.

Using the above facts, Canco's adjusted taxable income ("ATI") and ATI Safeharbour can be calculated as follows:

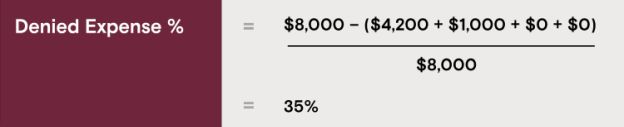

Using the above noted facts, the Main Formula produces the following result:

Accordingly, Canco's $8,000 of otherwise tax-deductible financing expenses will be reduced by 35% (i.e., $2,800) to $5,200 as a result of the application of the EIFEL Rules. The $2,800 of denied interest and financing expenses can generally be carried forward by Canco and applied in any future taxation year. Note, if Canco (and/or an affiliate) did have unused excess capacity carryforwards of not less than $2,800, it may have been possible for Canco to reduce the numerator of the Main Formula (and by extension the denied expense percentage) to nil.

Conclusion

In sum, the EIFEL Rules are a complicated set of legislative measures that will provide both substantive and compliance challenges to taxpayers, particularly in the first few taxation years while the inevitable teething pains are sorted out. Taxpayers to whom the EIFEL Rules will apply should proceed with caution.

Footnotes

1. In other words, for a trust or corporation with a calendar tax year-end, the EIFEL Rules will apply as of January 1, 2024.

2. Put another way, the numerator (after the specified reductions have been taken into account) represents what are considered, under the EIFEL Rules, to be "excessive" interest and financing expenses.

3. As noted above, for taxation years that begin on or after October 1, 2023, but before January 1, 2024, the fixed percentage will be 40%. Also, as mentioned below, this fixed ratio can be replaced by a group ratio concept in certain circumstances.

4. For example, if a taxpayer were to incur interest and financing expenses in a particular year in an aggregate amount equal to the sum of its: (i) ATI Safeharbour, and (ii) interest and financing revenue for that taxation year, the application of the Main Formula would not generate an expense reduction percentage. Accordingly, to the extent that its aggregate interest and financing expenses are less than this amount, it will generally cause the taxpayer to have excess deduction capacity.

5. This carryforward mechanism produces a similar conceptual result as a system in which a taxpayer's restricted interest and financing expenses for a particular taxation year could be carried back to any of its three prior taxation years.

6. Similarly, the variable in the Main Formula which deals with excess capacity received from affiliates effectively requires a taxpayer to first apply such transferred capacity to reduce is restricted interest and financing expenses before being able to use such transferred capacity to reduce the numerator in the Main Formula in the taxation year in which the transferred capacity was received.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.