- in United States

- with readers working within the Utilities industries

- within Law Practice Management, Wealth Management and Coronavirus (COVID-19) topic(s)

President Biden signed the Inflation Reduction Act of 2022 (IRA)1 into law on Tuesday, August 16, 2022. Among other things, the IRA expands the federal tax credits available to promote renewable energy and revises the requirements and qualification criteria for the Section 45Q carbon capture credit. This Legal Update focuses on the IRA's carbon capture use and sequestration provisions.

The key carbon capture components of the IRA are listed below, and a more detailed analysis of each component follows in this Legal Update.

The IRA:

- Extends eligibility for the tax credit to projects that begin construction before January 1, 2033, from January 1, 2026.

- Revises the "base" amount of the tax credit and increases the credit amount if certain prevailing wage and apprenticeship requirements are satisfied. Also includes an additional increase in amount for direct air capture facilities.

- Lowers the capture requirements for both direct air capture and industrial capture projects to be eligible for the credit.

- Introduces an option to allow "direct pay" for both taxable and non-taxable entities.

- Introduces an option for taxable entities to transfer the tax credits to third parties for cash.

- Replaces the 1-year carryback and 20-year carryforward periods with a 3-year carryback and 22- year carryforward period.

- Imposes a 15% minimum tax on corporate taxpayers with adjusted financial statement income in excess of $1 billion, effective for tax years beginning after December 31, 2022, with the ability to apply the carbon capture tax credit to reduce up to 75% of the minimum tax in excess of $25,000.

Extension of the 45Q Eligibility Period

Under prior law, projects would need to have begun construction prior to January 1, 2026, in order to be eligible for the tax credit. The IRA extends the deadline for any qualified facility that begins August 19, 2022 2 Mayer Brown | US Inflation Reduction Act of 2022: Carbon Capture Use and Sequestration Provisions construction prior to January 1, 2033, if either (i) the carbon capture equipment begins construction before such date or (ii) the original planning and design for such facility involved installation of carbon capture equipment. There is no change to how beginning of construction is defined, and such construction requirement can be satisfied if either construction of the carbon capture equipment begins before such date or the original planning and design for such facility includes installation of carbon capture equipment. Similar to start-of-construction guidance issued with respect to the PTC and the ITC, IRS Notice 2020-12 provides two methods for establishing the beginning of construction: (i) starting physical work of a significant nature either directly or by contract or (ii) paying or incurring (depending on the taxpayer's method of accounting) 5% of the ultimate tax basis of the project. Both methods require that a taxpayer make continuous progress toward completion once construction has begun.2

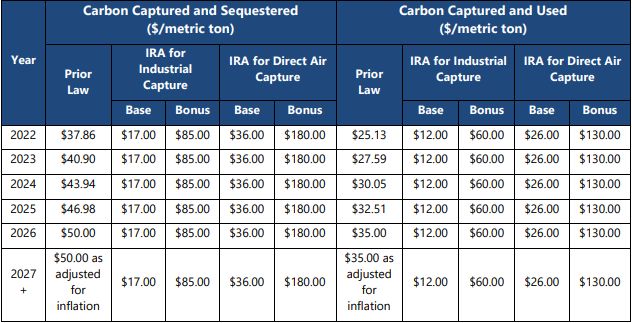

Available 45Q Credit Amounts

The IRA implements a two-tiered credit amount structure—a "base" credit amount and a "bonus" amount if certain prevailing wage and apprenticeship requirements are met. The base amount of the credit available for each metric ton of qualified carbon oxide captured is reflected in Table 1 below. The IRA introduces a higher base credit amount for direct air capture facilities.

The IRA provides that the base amount of the 45Q tax credit may be multiplied by 5 if the qualified facility causes any laborer or mechanic employed by contractors or subcontractors in the construction or repair of the facility to be paid wages not less than the prevailing rates for construction or repair of similar character in the locality of the facility. The facility will also have to satisfy apprenticeship requirements. The requirements become effective 60 days after the Internal Revenue Service issues additional guidance with respect to such requirements, and any carbon capture equipment that begins construction prior to such date and is installed at a qualified facility that also began construction prior to such date is eligible for the increased credit amounts automatically.

Table 1. 45Q Tax Credit Amounts

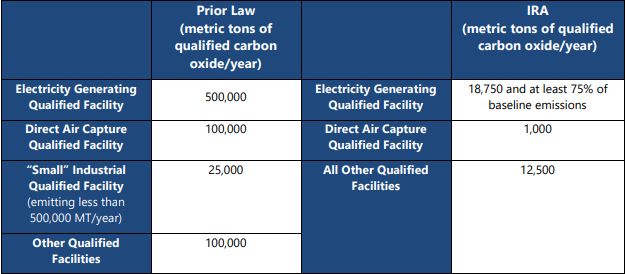

"Qualified Facility" Emissions Thresholds

The IRA significantly lowers the threshold of carbon oxides that a facility must capture in order to be eligible for the tax credit. Under prior law, there was a fourth category of qualified facilities that no longer exists. This category was for facilities that do not emit more than 500,000 metric tons of carbon oxide in any year and that capture at least 25,000 metric tons of qualified carbon oxide per year for use in which a commercial market exists other than as a tertiary injectant for enhanced oil recovery. Under the IRA, there are only three categories—electricity generating qualified facilities, direct air capture facilities, and other qualified facilities—each with a decreased threshold as compared to that under prior law.

Table 2. Carbon Oxide Thresholds

Direct Pay Option

The IRA includes a "direct pay" option that consists of a cash payment in lieu of receiving a tax credit. For most of the renewable energy tax credits addressed in the IRA, this option is limited to taxexempt entities, which would not otherwise be able to take advantage of the tax credit. However, the IRA includes an exception for carbon capture tax credits. Both taxable and tax-exempt entities may elect the direct pay option, but any taxable entity may only so elect for the first 5 years of the tax credit period that is otherwise available.

Credit Transferability

The IRA includes a new option that allows taxable project owners to transfer all or part of their tax credits arising in tax years after December 31, 2022, to third parties in exchange for cash on an annual basis. While this option provides additional flexibility to taxable project owners, it does not allow the transferee of the credits to take a tax deduction for its purchase price, whicCarryback and Carryforward Periods h may put the transferee in a worse position than a traditional tax equity investor.3

Carryback and Carryforward Periods

The IRA replaced the prior 1-year carryback and the 20-year carryforward periods with a 3-year carryback and 22-year carryforward period for carbon capture tax credits. This applies for all taxable years beginning after December 31, 2022.

Minimum Tax

The IRA imposes a 15% corporate alternative minimum tax on any corporation that has an average annual adjusted financial statement income for any consecutive 3-year period in excess of $1 billion. The annual adjusted financial statement income disregards any amounts received under the "direct pay" option and is also reduced by depreciation deductions. The carbon capture credit may be applied to reduce up to 75% of the minimum tax in excess of $25,000. This minimum tax would apply for taxable years beginning after December 31, 2022.

Footnotes

1. Text of the IRA is available at https://www.taxequitytimes.com/wpcontent/uploads/sites/15/2022/08/inflation_reduction_act_of_2022.pdf

2. For further information on start of construction, see our prior Legal Update at https://www.mayerbrown.com/en/perspectivesevents/publications/2020/02/irs-issues-first-batch-of-long-awaited-carbon-capture-tax-credit-guidance

3. See further discussion regarding transferability at https://www.taxequitytimes.com/2022/08/the-green-energy-tax-incentives-of-theinflation-reduction-act-of-2022/

Visit us at mayerbrown.com

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2020. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.