Introduction

The ability to generate sustainable revenue remains a huge challenge for the Nigerian government, especially due to the decline and instability in oil prices which has affected revenue generation from the Nigerian oil and gas industry. As part of efforts to address its revenue challenges, the Federal Government earlier in the year launched the Strategic Revenue Growth Initiative (SRGI) to boost revenue generation by government agencies and enable it to meet its ever growing financial obligations. The objectives of the SRGI include an increase of the Value Added Tax (VAT) rate from the current rate of 5%, identification of new revenue sources and enhancing revenue collection from existing revenue sources.

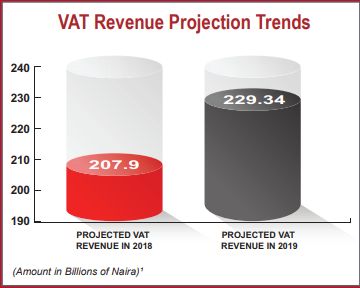

As the Federal Government's foremost revenue generation agency, the Federal Inland Revenue Service (FIRS) has expressed its commitment towards achieving the SRGI goals and it appears that the FIRS has positioned VAT as one of the major planks upon which it can increase government tax revenue. A review of recent VAT collection trends and revenue projections will show an increasing reliance on VAT. For example, in 2017, total VAT collection was ₦972.34 billion, while in 2018 it moved up to ₦1.1 trillion. This trend has continued with an increase in the Federal Government's projected revenue from VAT for the year 2019 to ₦229.34 billion as announced in the President's budget speech.

In addition, the Federal Government in its Medium Term Expenditure Framework 2020 – 2022 has projected an increase in VAT revenue collection efficiency from the present average of 21% to at least 35% by 2022.2 This highlights the Federal Government's increased focus on VAT and the potential that VAT presents in increasing the revenue profile of the government.

In view of the above, this newsletter will examine recent developments in the administration of VAT in Nigeria and the overall importance of VAT to the Nigerian economy

Administration of VAT in NigeriaMatters Arising

Regulatory Developments

VAT was first introduced in Nigeria by the VAT Decree of 1993, which has undergone subsequent amendments and explanatory notes issued in 1996, 1998 and 2007 respectively to reflect modifications and provide clarifications on the operation of VAT in Nigeria. VAT is currently charged at the rate of 5% on the supply of VATable goods and services in Nigeria and this rate is regarded as one of the lowest amongst peer countries, such as Ghana and South Africa, where VAT is charged at 12.5% and 15%, respectively.

Notwithstanding the relatively low rate of VAT in Nigeria, there has been significant revenue from VAT in Nigeria. As stated above, in 2017, the FIRS recorded a VAT revenue of ₦972.34 billion which subsequently increased to ₦1.1 trillion in 2018.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.