We expect a battle between Spain's two superclubs for top spot in the Money League for the next few years at least

Welcome to the 14th edition of the Deloitte Football Money League, in which we profile the highest earning clubs in the world'smost popular sport. TheMoney League is published nine months after the end of the 2009/10 season, and is therefore the most contemporary and reliable analysis of clubs' relative financial performance.

There are a number of methods that can be used to determine clubs' relative size – including measures of fanbase, attendance, broadcast audience, or on-pitch success. Indeed the relative wealth of certain clubs' owners has filled many column inches in recent times. However, the Money League focuses on the clubs themselves, comparing revenue from day to day football operations which we believe is the best publicly available financial comparison.

Whilst last year's Money League, covering the 2008/09 season, showed football's top clubs' relative resistance during the early stages of the economic downturn, it wasn't until the 2009/10 season, which is the focus of this edition, that we expected to see the full impact on clubs.

We continued to assert that the game's top clubs would be well placed to meet these challenges given their large and loyal supporter bases, ability to drive broadcast audiences, and continuing attraction to corporate partners.

This was more than borne out by clubs' revenue performance in 2009/10. The combined revenues of the top 20 Money League clubs surpassed €4 billion for the first time, with a total of €4.3 billion being an 8% increase on the previous year. All bar three of the top 20 clubs achieved revenue growth in 2009/10.

The established large and loyal supporter bases and historic on-pitch success underpin the brand strength of football's top clubs. These characteristics mean that a handful of clubs continue to drive the highest revenues and populate the top positions within the Money League.

The same ten clubs populate the top ten places in the Money League for the second successive year, with the top six ranking identical to last year. Six of those top ten have been in our Money League top ten in each of the last ten years. Each of this year's top ten clubs has been in for at least eight of the last ten years and none has ever dropped below 13th in that period. This shows both the enduring strength of these clubs and the scale of the challenges to those aspiring to break into that elite group. Nonetheless, we expect to see one or two clubs make that step in the next year or two.

Spanish one-two

Congratulations to Real Madrid who head the Money League for the sixth successive year. Los Blancos will doubtless be confident that they can match Manchester United's eight year hegemony enjoyed from 1996/97, the first edition of the Money League, through to 2003/04.

FC Barcelona is placed second in the Money League completing a Spanish one-two for the second successive year. Whilst the Catalan club could not quite match its domestic double and UEFA Champions League winning season of 2008/09 in 2009/10, it retained the La Liga title and added the FIFA World Club Cup and UEFA Super Cup.

It is Barca's on-pitch success that has underpinned its revenue growth in recent years. Conversely, Real's recent revenue growth has been achieved despite relatively modest on-pitch performance by the club's own high standards, particularly in the Champions League.

The combined revenues of the top 20Money League clubs surpassed €4 billion for the first time in 2009/10

Whilst Real held a €40m revenue advantage over Barca in 2009/10, Barca's revenues should exceed €400m in the next edition of the Money League, particularly given the club's new shirt sponsorship deal with the Qatar Sports Investment Agency which will deliver revenue from 2010/11. Hence, we expect a battle between Spain's two Superclubs for top spot in the Money League for the next few years at least, with on-pitch performance likely to be a key driver.

Promotion and relegation

Whilst Spanish clubs claim the top two spots in the Money League, England retains the largest representation from any single country, again with seven clubs. This strength in depth is driven by the scale and relatively even distribution of the Premier League's centrally negotiated broadcast monies and the success of English clubs in generating higher matchday revenues than their continental competitors.

Fourteen of the top 20 clubs participated in the Champions League in 2009/10 with six clubs participating in the Europa League from the Group phase onwards

As in last year's edition, all of this year's 20 clubs are from the 'big five' European leagues with Germany and Italy contributing four clubs each, Spain three clubs, and France two clubs.

VfB Stuttgart and Aston Villa return to the top 20 after a one year and five year absence respectively. Atlético de Madrid's success in winning the reformatted and renamed UEFA Europa League, Europe's second tier clubs competition, allow it to claim 17th position, its highest position since the 12th place secured in our first edition of the Money League back in 1996/97.

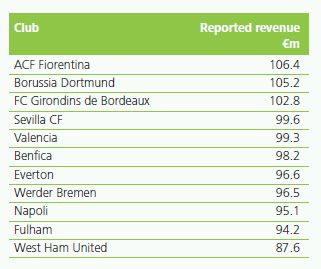

Two German clubs, Werder Bremen and Borussia Dortmund, drop out of this year's top 20, continuing a recent trend of two or three clubs being relegated from the top 20 each year, with on-pitch performance and particularly participation, or a lack of it, in the Champions League being a key driver of a club's promotion or relegation from the top 20.Fourteen of the top 20 clubs participated in the Champions League in 2009/10 with six clubs participating in the Europa League from the Group phase onwards, four of whom parachuted in from the top-tier competition. Four clubs – Manchester City, Tottenham Hotspur, Schalke 04, and Aston Villa – didn't participate in any European competition from the group phase onwards.

Inter's treble winning season – lifting the Scudetto, Coppa Italia, and Champions League – did not allow it to move up theMoney League with the club retaining ninth position despite a €28m (14%) uplift in revenue,

Movers and shakers

So who are the biggest movers in this year's list? Manchester City has climbed the most places, up nine to eleventh position, even though the club did not participate in European competition. Whilst its revenue growth in 2009/10 has been due to commercial revenue increases, the club's owners will be hoping the heavy investment in the playing squad will translate into on pitch success, particularly in qualifying for the Champions League. Should this be achieved, Manchester may join Milan and London in having two clubs in the Money League top ten in future editions.

Perhaps a more immediate challenger to the top ten is Tottenham Hotspur, who climb three places to 12th in this edition. The club's continued on-pitch improvement allowed it to finish fourth in the Premier League in 2009/10 and qualify for this season's Champions League. Whilst there is a gap of over €50m between them and tenth place Juventus, the revenue that Spurs will receive from participating in Europe's top clubs' competition in 2010/11 will provide a substantial boost. Juve's failure to qualify for the Champions League in 2010/11 will likely mean that it drops out of the top ten next year.

Perhaps surprisingly, Inter's treble winning season – lifting the Scudetto, Coppa Italia, and Champions League – did not allow it to move up the Money League with the club retaining ninth position despite a €28m (14%) uplift in revenue. The club is close behind Liverpool and its Milan neighbours, but its non mover status emphasises the challenges it, along with most Italian clubs, has in addressing matchday and commercial revenues.

Clubs from the 'big five' European leagues also occupy the vast majority of positions immediately below the top 20 as the table below shows

Moving forward

What can we expect in future years? New, bigger central overseas broadcast deals, from 2010/11 should allow English clubs to retain the highest representation in the Money League in forthcoming years.

Whilst Inter, AC Milan and Juventus retained top ten positions in this edition, and Serie A's return to collective selling from 2010/11 is an encouraging sign that Italian football is in the early stages of much needed reform, more action is necessary at an accelerated pace particularly in relation to stadia, if Italian clubs are not to lose further ground against their European peers. It is only five years since two Italian clubs, Juventus and AC Milan, claimed top five positions in the Money League.

The much discussed implementation of UEFA's Financial Fair Play Regulations from 2013/14 will not impact on clubs' revenue generation, with the key principle underlying the regulations being that clubs do not spend more than they earn. Indeed the regulations should help encourage clubs to identify and realise sustainable increased revenues

In any event, in principle, it is logical to expect those clubs earning the most to be able to invest the most in their playing squads and this to translate into on-pitch success and hence a continued stasis amongst clubs in terms of the Money League rankings, particularly towards the top of the list.

In our previous publications, we have demonstrated that there is a strong correlation between a club's wage bill and on-pitch success, particularly within domestic competition. Indeed this year's Money League clubs have won 43 of the 50 domestic league titles available in the 'big five' countries over the past ten years. The link is less strong at European competition level although only one club from outside the Money League top ten – Porto in 2003/04 – has won the Champions League in the past ten years.

In the positions immediately below first place in domestic leagues, the all important European qualification places, there is more variability in clubs' finishing position although in general those clubs further up the Money League have been the most consistent qualifiers for the Champions League.

In future, we expect a continuation of the pattern of the top positions in the list being relatively resistant to movement of clubs, and two or three clubs dropping in and out of the top 20 rankings each year, largely due to on-pitch performance

This year'sMoney League clubs have won 43 of the 50 domestic league titles available in the 'big five' countries over the past ten years

Our focus this year

In addition to our usual profiles of the top 20 clubs we include two feature articles in this year's publication. The first assesses each of the three key revenue streams, listing the top 20 clubs for each, whilst comparing and contrasting these lists with the overall top 20. With the return of Serie A to collective selling from 2010/11, Spain stands alone as the only 'big five' league to retain an individual selling regime, although discussions are currently taking place regarding the future distribution of broadcast revenues with the rights selling method potentially open for future discussion. Our second feature article therefore looks at the collective and individual sale of broadcast rights, the relative impact of each regime on clubs' revenue generating ability, and the impact on both domestic competition and the Money League.

The Deloitte Football Money League was compiled by Dan Jones, Austin Houlihan, Richard Battle, Adam Bull, Martyn Hawkins, Simon Hearne, Rich Parkes and Alexander Thorpe. Our thanks go to all those who have assisted us, inside and outside the Deloitte international network. We hope you enjoy this edition.

How we did it

We have used the figure for total revenue extracted from the annual financial statements of the company or group in respect of each club, or other direct sources, for the 2009/10 season. In some cases, the annual financial statements do not cover a whole season, but are for the calendar year, in which case we have used the figures for the most recent calendar year available.

Revenue excludes player transfer fees, VAT and other sales related taxes. In a few cases we have made adjustments to total revenue figures to enable, in our view, a more meaningful comparison of the football business on a club by club basis. For instance, where information was available to us, significant non-football activities or capital transactions have been excluded from revenue.

Each club's financial information has been prepared on the basis of national accounting practice or International Financial Reporting Standards ("IFRS"). The financial results of some clubs have changed, or may in future change, due to the change in the basis of accounting practice. In some cases these changes may be significant.

Based on the information made available to us in respect of each club, to the extent possible, we have split revenue into three categories – being revenue derived from matchday, broadcast and commercial sources. Clubs are not wholly consistent with each other in the way they classify revenue. In some cases we have made reclassification adjustments to the disclosed figures to enable, in our view, a more meaningful comparison of the financial results.

Matchday revenue is largely derived from gate receipts (including season tickets and memberships). Broadcast revenue includes revenue from both domestic and international competitions. Commercial revenue includes sponsorships and merchandising revenues. For a more detailed analysis of the comparability of revenue generation between clubs, it would be necessary to obtain information not otherwise publicly available.

Some differences between clubs, or over time, will arise due to different commercial arrangements and how the transactions are recorded in the financial statements. Some differences between clubs, or over time, will arise due to different ways in which accounting practice is applied such that the same type of transaction might be recorded in different ways.

This publication contains a variety of information derived from publicly available or other direct sources, other than financial statements.

We have not performed any verification work or audited any of the information contained in the financial statements or other sources in respect of each club for the purpose of this publication.

For the purpose of the international comparisons, all figures for the 2009/10 season have been translated at 30 June 2010 exchange rates (£1 = €1.2214). Comparative figures have been extracted from previous editions of the Deloitte Football Money League.

There are many ways of examining the relative wealth or value of football clubs – and at Deloitte we have developed methodologies to help potential investors or sellers do just that. However, for an exercise such as this, there is insufficient public information to do that. Here – in the Deloitte Football Money League – we use revenue as the most easily available and comparable measure of financial wealth.

Based on the information made available to us, we have split revenue into three categories – matchday, broadcast and commercial sources.

Ups and downs

1. Real Madrid

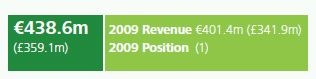

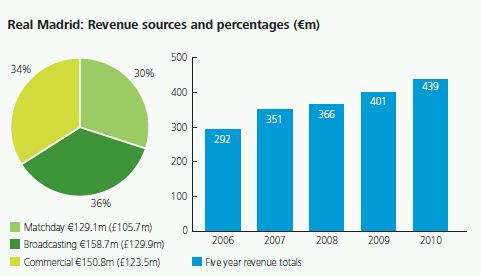

Revenues of €438.6m (£359.1m) cement Los Blancos' position at the top of the Money League for the sixth consecutive year. Real remains the only club to surpass €400m in revenue, doing so for the second successive season. Whilst the 2009/10 season saw Real Madrid again outperformed on the pitch by Barcelona, who beat them to the league title for a second successive year, in revenue terms Real Madrid were over €40m (£33m) ahead of their Spanish rivals.

Broadcasting revenue of €158.7m (£129.9m) was consistent with the previous season (falling by only 1%), underpinned by the club's broadcast rights contract with Mediapro. This contract, combined with certain others guarantees the club more than €1.1 billion up to 2013/14. Exiting the UEFA Champions League at the Round of 16 meant Real Madrid earned €26.8m (£21.9m), €22m (£18m) less than the tournament winners, Inter Milan. La Liga clubs are currently discussing proposals for a more equal revenue distribution mechanism from domestic competition broadcast rights, although Real and Barca will seek to at least protect current revenue levels which provide a key advantage over their European peers. To put this into context, Real's broadcasting revenue is higher than the total revenue of half of the Money League clubs.

LosMerengues will need their star player signings of 2009 to justify their transfer value on the pitch both domestically and in the Champions League in order to maximise its revenues

Real reported an €11.6m (8%) increase in commercial revenue to €150.8m (£123.5m). As a result Real and Bayern Munich are the only two clubs that generated over €150m from this source. Real's shirt front deal with Bwin runs until 2012/13 and reportedly generates between €15m (£12.3m) and €20m (£16.4m) per season. Adidas will continue as kit sponsor until 2011/12. Other partnerships, including with Audi, Coca-Cola and Spanish beer brand Mahou also contributed to commercial income in 2009/10, with Saudi Arabian telecoms company STC signing a three year deal starting from 2010/11.

Matchday revenues grew by a remarkable €27.7m (27%) to €129.1m (£105.7m). One driver of this growth was the hosting of the Champions League final in 2010 at the Santiago Bernabéu in front of a crowd of 75,000. Real Madrid also achieved matchday revenue increases at other matches owing to increased attendances, memberships and prices. Real has reconfigured certain areas within the Bernabéu in recent years in order to grow corporate hospitality revenues.

In the coming years, particularly as UEFA's Financial Fair Play rules take effect, Real Madrid's revenue prowess should, in theory, translate into a competitive advantage on the pitch. In the short term, Los Merengues will need their star player signings of 2009 to justify their transfer value on the pitch both domestically and in the Champions League in order to maximise its revenues and keep ahead of great rivals Barcelona in the Money League.

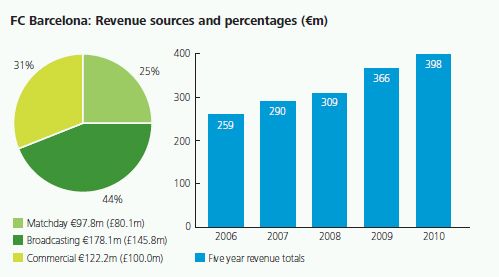

2. FC Barcelona

Barcelona's unprecedented on-pitch success in 2008/09 was continued into 2009/10, a season in which the club won La Liga and the Spanish Supercopa. This was complemented by reaching the semi-final of the UEFA Champions League and being crowned FIFA Club World Cup champions in December 2009.

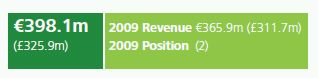

Despite the strengthening of Sterling against the Euro between 2008/09 and 2009/10, Barcelona have consolidated their 2nd placed position in the Football Money League, increasing their lead over Manchester United from €38.9m in 2008/09 to €48.3m (£39.5m). In 2009/10, revenue grew across all three categories with total revenue increasing by 9% to €398.1m.

Less successful Copa del Rey and Champions League campaigns saw the number of home matches at the Nou Camp reduce from 30 in 2008/09 to 27 in 2009/10. Even so, matchday revenue increased slightly by €2.3m (2%) to €97.8m, with Barcelona generating the 4th highest matchday revenues amongst Money League clubs. A small increase in matchday revenue in 2010/11 will likely enable Barcelona to join Real Madrid in generating over €100m across each of the three revenue streams. Manchester United will also potentially achieve this in 2010/11.

Broadcast revenues increased by €19.7m (12%) to €178.1m with a rise in Champions League central distributions of €8.1m, particularly driven by higher market pool payments to Spanish clubs, contributing to this increase. The club also signed a new individual broadcast contract with Mediapro in 2010, with improved financial terms, which runs until 2014.

2009/10 saw a healthy increase in commercial revenue of €10.2m (9%) to €122.2m. Following the arrival of new President Sandro Rosell in June 2010, the club entered into a multi-year main shirtfront sponsorship deal for the first time in its history. The new administration has attributed this decision to the need to to tackle the club's debt. The five and a half season deal with Qatar Sports Investment worth a guaranteed minimum of €165m (£135m) is the highest of any reported shirt sponsorship deal and will see the Qatar.

Foundation logo on the Blaugrana's shirt from the start of the 2011/12 season through to the end of the 2015/16 season. Part of the new administration's strategy will look to build on Barca's on-pitch success and the strength of its brand in order to increase commercial revenue.

If Barcelona can sustain their remarkable on-pitch success of recent seasons and continue to translate this into revenue growth then they will challenge their great rivals for top position in the Money League in future editions.

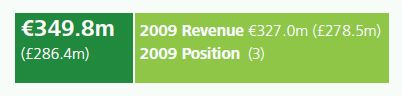

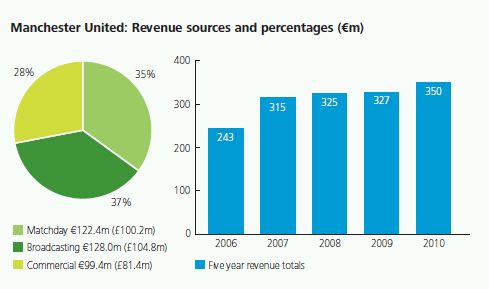

3. ManchesterUnited

Manchester United retains third place in the Money League after a season in which the club experienced mixed fortunes on the pitch. Victory in the League Cup for a second successive season and a second placed Premier League finish were tempered by comparatively disappointing FA Cup and UEFA Champions League campaigns.

Overall revenue grew by £7.9m (3%) to £286.4m (€349.8m) with the club's fortunes on the pitch mirrored by mixed performance across the three revenue categories. A decrease in matchday revenue was more than offset by growth in both broadcasting and most significantly, commercial revenues. Despite favourable fluctuations in the Sterling exchange rate, Barcelona increased the gap between second and third spot in the Money League by €9.4m to €48.3m.

Elimination in the Champion's League at the quarter-final stage and an early exit from the FA Cup resulted in fewer home games (28 versus 30 in 2008/09) and a decrease of £8.6m (8%) in matchday revenue to £100.2m. However, the Red Devils still generate revenues per home match of £3.6m (€4.4m). Despite a c.5% decrease in season ticket renewal ahead of the 2010/11 season, average league match attendances have to date remained broadly consistent with previous years.

The new cycle of Champions League broadcast and commercial contracts, with improved values, meant that despite a less successful run in the competition, the club's distribution actually rose by €7.5m (20%) to €45.8m. This was the principal driver of overall broadcasting revenue growth, which increased by £5.1m (5%) in 2009/10.

The club's commercial activities saw the most significant revenue growth over the year, increasing by £11.4m (16%) to £81.4m. United have built on the commercial success of previous years with the addition of several new commercial partners which boosted revenues in 2009/10 including deals with Turkish Airlines, Betfair and several telecommunications companies. The increased value of the club's new shirt sponsorship deal with Aon Corporation which came into effect for the 2010/11 season will boost United's commercial revenue further, as will additional commercial deals including those with Singha, Thomas Cook, Epson and Vina Concha y Toro.

As predicted in last year's Money League, despite a favourable move in the Sterling exchange rate, the gap between United and its Spanish rivals has increased. Manchester United's revenue performance this year emphasises that only the most successful on-pitch performance, particularly in the Champions League, along with continued growth in commercial revenues and a stronger Sterling will enable the club to catch the two Spanish clubs.

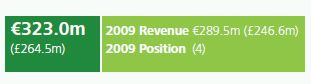

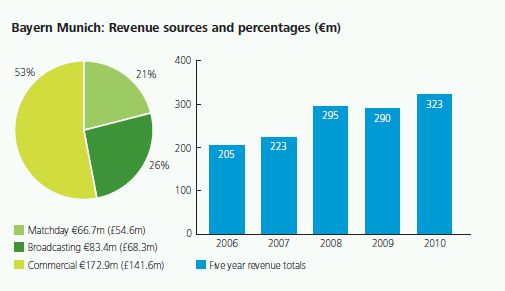

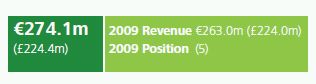

4.Bayern Munich

A domestic league and cup double and their first UEFA Champions League final since 2001 helped Bayern Munich to generate total revenue of €323m (£264.5m), up by €33.5m (12%) on 2008/09, and secure fourth place in the Money League for the third consecutive year. The Bavarians have closed the gap on Manchester United in third spot to €26.8m, a reduction of €10.7m since 2008/09. However, given that Bayern's almost perfect season coincided with United's worst run in the Champions League for four years and that the Red Devils will grow broadcast and commercial revenues again in 2010/11 it remains a significant challenge for Bayern to break into the top three for the first time since the 2001/02 season.

Bayern's revenue exceeded €300m for the first time in 2009/10 with growth across all three revenue streams. The largest rise was in broadcast revenue which increased by €13.8m (20%) on the 2008/09 figure to reach €83.4m (£68.3m) in 2009/10. Finishing runner-up in the Champions League to Internazionale earned Bayern central UEFA distributions of €44.9m, an increase of €10.3m on 2008/09, the third highest of all the Money League clubs after Internazionale and Manchester United. However, the value of these deals remains significantly lower than its European rivals due to the limited development of the German Pay-TV market compared to the other 'big five' European countries.

As in previous years, commercial revenue is the club's real strength, accounting for over half of total revenue. The €172.9m (£141.6m) generated from commercial activities in 2009/10, an increase of €13.6m (9%) on the previous year, is the highest of any of the Money League clubs and remains more than €20m higher than the next best, €150.8m (£123.5m), achieved by Real Madrid.

The club's on-pitch success during 2009/10 is likely to have contributed to this growth by triggering performance bonuses attached to their sponsorship deals.

The progress of Louis van Gaal's men to domestic and European cup finals led to the club playing 25 home matches during 2009/10 as compared with 23 in 2008/09. This, combined with a season of largely selling out the 69,000 capacity Allianz Arena, has seen Bayern's matchday revenue increase by €6.1m (10%) in 2009/10 to €66.7m (£54.6m). These increased revenues have facilitated the club's ability to pay off a large portion of the stadium debt; within six years of the stadium opening the club will reportedly have paid off €176m.

Despite an indifferent first half of the 2010/11 domestic season Bayern have successfully qualified for the knockout stages of the Champions League, which is vital if they are to keep clear distance between themselves and the chasing pack and make up further ground on the Money League's top three

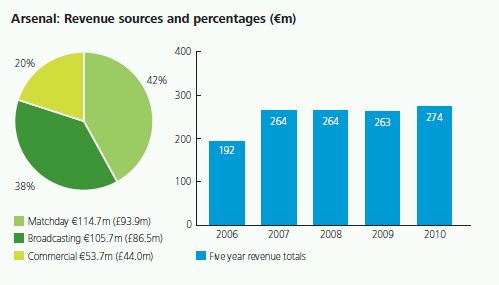

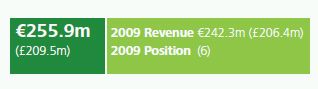

5. Arsenal

Arsenal retain fifth place in the Money League, posting core football revenues of £224.4m (€274.1m) to maintain their position as the second highest ranking English club in the Money League. Whilst football revenues remained flat overall, the club also earned a further £157m (€192m) from property development.

The financial benefits derived from the Emirates stadium are regularly acclaimed. In 2009/10 the club consistently achieved its now customary capacity attendances, averaging 59,765 for home league games, though five fewer home matches (27) were played than in 2008/09, contributing to the 6% fall in matchday revenue from £100.1m (€117.5m) to £93.9m (€114.7m). Four fewer home games were played in domestic cup ties. But on a positive note, matchday revenue per match rose from £3.1m (€3.7m) to £3.5m (€4.2m) implying that if the club performs well in future cup competitions substantial matchday revenue increases will follow.

Broadcast revenues increased by 14% in 2009/10, to £86.5m (€105.7m), up from £75.8m (€89.0m) in the previous season. This uplift is partly attributed to higher distributions from the Premier League, which contributed £51.7m (€63.1m), as the team finished third in the league rather than fourth, as in 2008/09. And whilst in 2009/10 Arsenal fell one round short of reaching the semi-final of the Champions League (as in the previous season), distributions from UEFA rose from €26.8m (£22.8m) to €33.4m (£27.3m), driven by the overall increase in value of UEFA's new broadcasting and commercial contracts for the competition.

In previous years we have noted how, in terms of commercial revenues, Arsenal lagged behind other elite European clubs. This remained the case in 2009/10, when commercial revenues reduced by £4.1m (9%) to £44.0m (€53.7m). The decrease can be attributed to a mixture of the economic climate, the lower number of home games which resulted in lower merchandising and catering revenues, and less successful Champions League and FA Cup campaigns meant lower revenues were generated from some sponsorship contracts.

Emirates hold stadium naming rights under a long term deal worth a reported £90m (€110m) extending to 2020/21, which also includes shirt front sponsorship rights until 2013/14. The club's kit deal with Nike has also been extended, and improved, to run for a further three years to 2013/14. Bound by such long-running partnerships, it may be that substantial increases in commercial revenues are not achievable in the short term, although the club renewed its secondary sponsorship deal with Lucozade Sport and secured Thomson Sport as its new travel agency partner in 2010.

Arsenal is committed to its mission of financial self sufficiency and has a strong and stable business model. Its investment in its stadium has provided the business with a solid foundation. In the longer term, if its strategy of pursuing international commercial development is successful, it could provide The Gunners with a financial strength matched by few clubs.

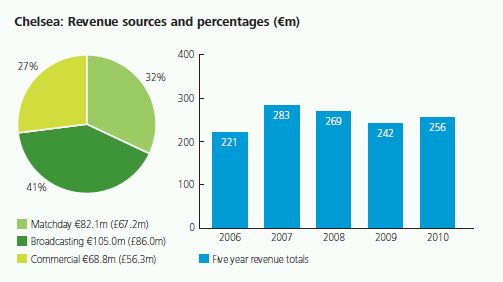

6. Chelsea

The arrival of Carlo Ancelotti as manager in the summer of 2009 after a period of managerial turbulence was immediately followed by significant on-pitch success. The club won the Premier League to end Manchester United's three year reign as champions, with the league title complemented by retaining the FA Cup and in doing so, securing for the club its first League and Cup double. However, domestic achievement contrasted with a disappointing UEFA Champions League campaign that saw Chelsea eliminated in the first knockout round by their former manager José Mourinho's Internazionale.

The club achieved less success in terms of revenue growth, with total revenue growing by only £3.1m (2%) to £209.5m, preventing the club from regaining their place in the top five (which was lost to Arsenal last year). As with Manchester United, a decline in matchday revenue was offset by increases in broadcast and commercial revenue.

Over the year, commercial revenue grew by £3.5m (7%) to £56.3m (€68.8m). The long term, high value shirt front (Samsung) and kit (adidas) deals were complemented by new partnerships, such as that with 188Bet. The security of the club's main partner deals as well as the continued growth of its sponsorship portfolio through recent deals such as those with Singha and Lucozade, provides a platform for the club to achieve further growth in future years

For the first time since Roman Abramovich's acquisition of the club Chelsea's matchday revenue fell, by £7.3m (10%), in part due to the club's disappointing Champions League campaign resulting in two fewer home fixtures in the competition. Although average home league attendances remained very strong at 99% of capacity (41,422), limited stadium capacity restricted Chelsea to the lower half of the top 20 in terms of average attendance amongst the Money League clubs. Despite this the club still generated the fifth highest matchday revenue with £67.2m (€82.1m) at an average of £2.4m per game.

Despite a less successful European campaign, the increased Premier League and UEFA Champions League distributions, up £5.1m to £52.8m (€64.5m) and €1.3m (£1.1m) to €32.2m (£26.5m) respectively, contributed to an increase in total broadcasting revenues of £6.9m (9%) to £86m (€105m).

Consistent on-pitch success, both domestically and in Europe, coupled with further commercial revenue gains are likely to be key to revenue growth in the short term. However, the limited capacity of Stamford Bridge, and the limitation this places on matchday revenues will make it challenging for Chelsea to return to the top five in the Money League in the near future

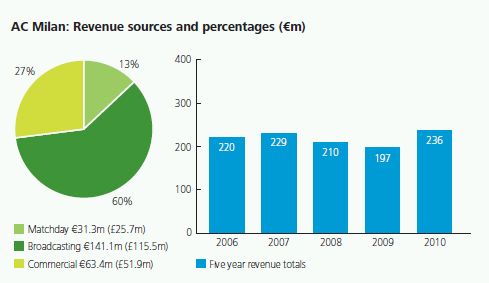

7. AC Milan

The return to UEFA Champions League football in 2009/10 helped AC Milan climb three places to seventh in the Money League with record revenues of €235.8m (£193.1m), up €39.3m (20%) on 2008/09. This climb in the rankings included overtaking city rivals Inter, despite the Nerazzurri's on-pitch dominance in 2009/10.

Reaching the Champions League's Round of 16 earned the club €23.8m in UEFA central distributions, dwarfing the €0.4m they received during their 2008/09 UEFA Cup run. This, combined with revenue from archive rights and option payments, drove a €42.1m (43%) increase in broadcast revenue in 2009/10. Milan boast the third highest broadcast revenue in this year's Money League with €141.1m (£115.5m). However, the club faces a struggle to maintain or increase this in the next edition of the Money League, given the introduction of collective selling of Serie A broadcast rights from 2010/11 and a more equal distribution of revenues amongst Italian clubs.

Despite finishing third in Serie A and competing in the Champions League, Milan's matchday revenue fell by €2.1m (6%) to €31.3m (£25.7m) in 2009/10 and accounted for only 13% of total revenue. A 16,900 decrease on 2008/09's average league attendance of 59,700 has left Milan's matchday revenue, with the exception of Juventus, as the lowest of the top ten clubs in the Money League and lower than that achieved by some clubs who did not make it into the Money League's Top 20. Plans to renovate the San Siro as part of Italy's bid for UEFA Euro 2016 may have provided the platform to boost matchday revenue, but since France were chosen to host the tournament these plans are less certain, although redevelopment is much needed.

The Rossoneri's commercial revenue decreased by €0.7m (1%) to €63.4m (£51.9m) in 2009/10. The club's shirt sponsorship deal with Bwin, reportedly worth an average of €12m per season, expired at the end of the 2009/10 season and has been replaced by a five year deal with Emirates worth a similar €60m (£49m). This contract, combined with a kit deal with adidas until 2016/17 and Champions League qualification, will help Milan to generate strong commercial revenues in 2010/11.

As noted, the club faces long term structural challenges in matchday and broadcast revenue. In the short-term, the club's performance both domestically and in the Champions League under new manager Massimiliano Allegri will be the key determinant of how high they finish in next year's Money League.

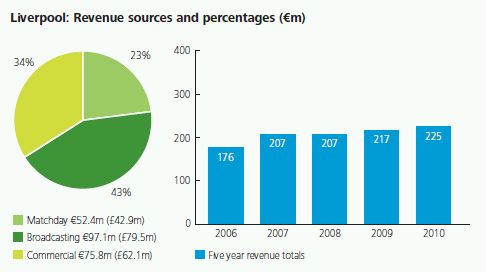

8. Liverpool

Liverpool slip one place to eighth position with revenues of £184.5m (€225.3m) in 2009/10. As is the case on the pitch, they are likely to face strong competition from Manchester City, who are the highest climbers up this year's Money League under their Middle Eastern owners, and Tottenham Hotspur who have qualified for the UEFA Champions League for the first time, for a top four position among English clubs in the Money League next year. The strategy of the Merseyside club's new North American owners, New England Sports Ventures (NESV), will be central to re-establishing and sustaining the club's on and off pitch success.

Matchday revenue of £42.9m (€52.4m) in 2009/10 was slightly up (by £0.4m) on the previous year despite a 2% drop in average home league attendance to 42,863 following a less successful Premier League campaign. 27 home games were played in both seasons, with matchday revenue per match of £1.6m consistent with the previous season (although this followed a 23% rise from £1.3m between 2007/08 and 2008/09).

Broadcasting revenue increased by £4.9m (7%) to £79.5m (€97.2m) from £74.6m (€87.6m) in 2008/09, driven by an uplift in UEFA distributions, as a seventh place finish in the Premier League provided £48.0m (€58.6m), £2.3m lower than in 2008/09 when the club finished second. Although Liverpool exited the Champions League at the Group stage, they received €5.7m (£4.7m) more in central distributions than in the previous season, when they reached the quarter-final, and a further €3m (£2.5m) as a result of parachuting into the Europa League and reaching the semi-final. However, not qualifying for the Champions League in 2010/11 means the club will receive significantly lower distributions from UEFA.

The increase in broadcast revenue was offset by a £5.6m decrease in commercial revenues, from £67.7m (€79.5m) to £62.0m (€75.9m). This reduction is attributed to reduced royalties and merchandising income. However Liverpool's 2010/11 commercial revenues will be boosted by the new four year deal with Standard Chartered Bank, providing a reported £20m per season – £12.5m more per annum than under the previous agreement withCarlsberg. Whilst adidas will continue as the club's kit provider until the end of the 2011/12 season, NESV will be hoping to bring their experience from baseball to help Liverpool generate further commercial revenues from global sources

Carlsberg. Whilst adidas will continue as the club's kit provider until the end of the 2011/12 season, NESV will be hoping to bring their experience from baseball to help Liverpool generate further commercial revenues from global sources.

Since they acquired the club in October 2010, the new owners have spent time 'taking stock' and have yet to appoint a new CEO, although they were active in the January 2011 transfer window. Plans for a new stadium are also being considered, which, if the business case for construction is proven, will be the most sustainable way for Liverpool to achieve further significant revenue increases in the coming years. In the meantime, an improvement in on-pitch performance is essential for the club to remain securely in the top half of the Money League.

To read this article in full please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.