Issues affecting all schemes

Lifetime allowance abolition – legislation and guidance

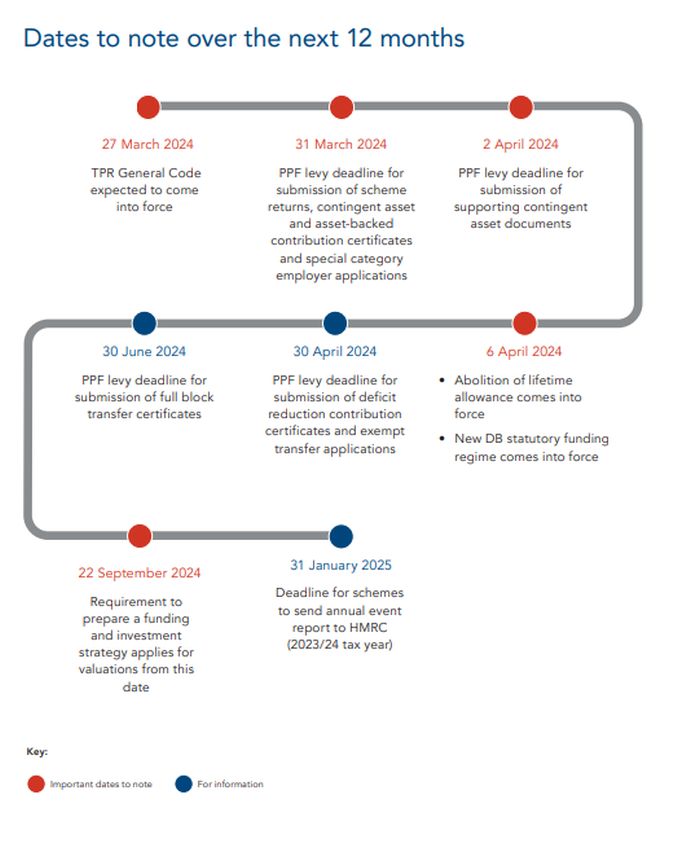

The Finance Act 2024, which provides for the abolition of the lifetime allowance (LTA) and introduction of the new tax regime for lump sums and lump sum death benefits from 6 April 2024, has received Royal Assent. HMRC has confirmed that a number of changes will need to be made to the Act to ensure that its provisions correctly reflect the intended policy. These changes will be made by regulations which have yet to be published.

HMRC has also published two further LTA guidance newsletters (February and March). These include FAQs and further guidance on a range of topics including:

- Pension commencement excess lump sums (PCELS) – in particular, the cap on the amount of a PCELS will be removed.

- Transitional tax-free amount certificates.

- Reporting obligations.

- LTA protections and enhancement factors.

Action

Trustees, employers and administrators should continue their preparations for abolition of the LTA and introduction of the new lump sum regime. They should also monitor publication of the HMRC regulations (and announcement of any further changes to the legislation), as well as publication of further HMRC guidance.

Cyber security – Pensions Regulator report

The Pensions Regulator (TPR) has published a report on the actions it took following the cyber breach experienced by Capita in early 2023. The report also sets out the steps that TPR expects trustees to take in the event of a cyber incident and emphasises the importance of schemes having robust cyber security and business continuity plans in place. For more information, please see our legal update.

Action

Trustees and administrators should review the report and consider whether any changes are required to their scheme's cyber security arrangements.

Automatic enrolment – earnings figures and alternative quality requirements

The government has announced that the 2023/24 automatic enrolment earnings figures will be retained for 2024/25, meaning they will be:

- Earnings trigger: £10,000.

- Qualifying earnings band: £6,240 – £50,270.

The government has also published the findings of its 2023 review of the automatic enrolment alternative quality requirements. This includes a response to its May 2023 call for evidence on the operation of the alternative quality requirements for DB and hybrid schemes. Following the review, the government has concluded that no changes are needed to the requirements.

Action

Employers should ensure that their payroll processes continue to reflect the correct earnings figures.

Pensions dashboards – "view" data

The Pensions Dashboards Programme has published FAQs on "view" data. The FAQs cover:

- What view data is.

- What the view data journey is.

- Whose responsibility it is to ensure data accuracy.

Action

No action required, but trustees and administrators may find the FAQs helpful.

Provision of incorrect information – liability

The Pensions Ombudsman (TPO) has upheld a complaint about the provision of incorrect information by a scheme regarding the entitlement of a member's cohabiting partner to a survivor's pension. The member contacted the scheme when he received a terminal diagnosis to ask what benefits his partner would be entitled to following his death. He was told that she would be eligible for a survivor's pension. Following the member's death, the scheme refused to pay a survivor's pension to the partner because, although the scheme rules provided for payment of a survivor's pension to cohabiting partners, this only applied to members in service on or after 1 April 2008, and the member had left service in 1991.

TPO decided that, although the scheme rules did not entitle the partner to a survivor's pension, a defence of estoppel by representation applied because:

- The scheme had made a clear and unequivocal representation that marriage was not a requirement for payment of a survivor's pension to a cohabiting partner. As a result, the member had a reasonable expectation that the scheme would provide his partner with a pension on his death and that there was no need for him to marry her to safeguard her financial future.

- It was reasonably foreseeable that the member would rely on the information given to him in the telephone call without requesting confirmation in writing. He was not given any other information that might have caused him to question the accuracy of the representation, nor was he signposted to the scheme rules or asked to read the scheme booklet. In view of that context and the prognosis of his illness, it was reasonable for him to rely on the telephone call alone, rather than continue to make more detailed enquiries.

- The member had acted on the incorrect information to his partner's eventual detriment.

TPO ordered the scheme to pay a survivor's pension to the member's partner (including arrears to the date of the member's death) and to pay her £2,000 for the severe distress and inconvenience caused.

Action

No action required.

Originally Published 11 March 2024

To view the full article click here

Visit us at mayerbrown.com

Mayer Brown is a global services provider comprising associated legal practices that are separate entities, including Mayer Brown LLP (Illinois, USA), Mayer Brown International LLP (England & Wales), Mayer Brown (a Hong Kong partnership) and Tauil & Chequer Advogados (a Brazilian law partnership) and non-legal service providers, which provide consultancy services (collectively, the "Mayer Brown Practices"). The Mayer Brown Practices are established in various jurisdictions and may be a legal person or a partnership. PK Wong & Nair LLC ("PKWN") is the constituent Singapore law practice of our licensed joint law venture in Singapore, Mayer Brown PK Wong & Nair Pte. Ltd. Details of the individual Mayer Brown Practices and PKWN can be found in the Legal Notices section of our website. "Mayer Brown" and the Mayer Brown logo are the trademarks of Mayer Brown.

© Copyright 2024. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.