In view of assisting financial market participants to comply with Sustainable Finance Disclosure Regulation requirements ahead of 1 January 2023, the date the regulatory technical standards enter into force, Luxembourg's Financial Sector Supervisory Authority has confirmed 31 October 2022 as the deadline for submission of the updated pre-contractual documentation for those who intend to benefit from the accelerated examination procedure.

In anticipation of the long-awaited regulatory technical standards (RTS), Level 2 regulation of Sustainable Finance Disclosure Regulation (SFDR) and Taxonomy regulation (TR), both EU and Luxembourg supervisory authorities have been continuously providing guidance to market participants in order to bring additional clarity into the evolving domain of sustainability disclosures.

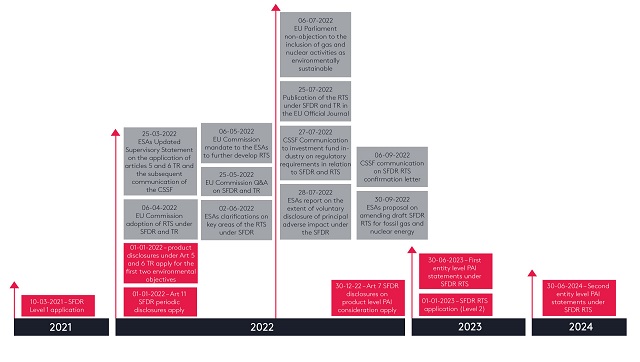

The European Securities and Markets Authority (ESMA) highlighted the sustainable finance roadmap as one of the key priorities in its 2023 work programme1. In order to remind you of the key dates and for easier navigation through regulatory events in the previous six months, we have summarised key dates and developments:

1 ESAs Updated Supervisory Statement on the application of SFDR, articles 5 and 6 of TR and the subsequent communication of the CSSF

By way of background, on 25 March 2022, the European Supervisory Authorities (the ESAs) published an Updated Supervisory Statement2, the key objective of which was to achieve an effective and consistent application and national supervision of SFDR.

The ESAs reminded that most of the provisions on sustainability-related disclosures laid down in the SFDR were applicable from 10 March 2021. While the application of the RTS has been delayed, now confirmed for 1 January 2023, as initially foreseen in the EU Commission letter dated 25 November 20213.

This delay does not impact the application of the amendments introduced by TR to SFDR. Indeed, the taxonomy-alignment4 related product disclosures are in force in respect of the first two environmental objectives from 1 January 20225.

The ESAs recommended using the interim period from 10 March 2021 until 1 January 2023 (the Interim Period) to prepare for the application of the forthcoming RTS, while also applying the relevant measures of SFDR and TR according to the relevant application dates.

It was also clarified that, under Articles 5 and 6 of TR, supervisory expectations for disclosures during the Interim Period are for financial market participants to provide an explicit percentage quantification to the extent of which investments underlying the financial product are taxonomy-aligned6.

In addition, the Updated Supervisory Statement includes an annex in which the ESAs detailed the application timeline of specific provisions of SFDR, TR and the related RTS. Transitional arrangements foreseen by the ESAs for entity-level principal adverse impact (the PAI) disclosures would no longer be relevant due to the delay of application of RTS. The first PAI disclosures in accordance with RTS should therefore be made in a statement published by 30 June 2023 in respect of a reference period corresponding to the calendar year 2022.

In Luxembourg, the Financial Sector Supervisory Authority (the CSSF) issued a communiqué on 1 April 2022 in order to bring the Updated Supervisory Statement to the attention of market participants.

In line with the Updated Supervisory Statement, the CSSF encouraged the use of the draft RTS7 as a reference during the Interim Period for the purposes of applying the provisions of articles 2a, 4, 8, 9, 10 and 11 of the SFDR and articles 5 and 6 of the TR.

2 EU Commission adoption of RTS under SFDR and TR

On 6 April 2022, the EU Commission took a further step in its action plan on financing sustainable growth by adopting the RTS8 supplementing SFDR and TR.

In the explanatory memorandum, the Commission reiterated9 bundling all 13 RTS into a single act, as well as deferring their application to 1 January 202310.

RTS brings additional precisions regarding:

- the details of the content and presentation of the information in relation to the principle of 'do no significant harm' (the DNSH);

- the exact content, methodologies and presentation of the information in relation to sustainability indicators and adverse sustainability impacts; and

- the content and presentation of the information in relation to the promotion of environmental or social characteristics and sustainable investment objectives in pre-contractual documents, on websites and in periodic reports.

Under these rules, financial market participants will have to provide detailed information about tackling and reducing any possible negative impacts that their investments may have on the environment and society. These new requirements will help to assess the sustainability performances of financial products and enhance the comparability of financial products from different sectors.

Key precisions brought by the RTS concern the following areas:

2.1 PAI reporting on the entity-level11

The RTS specify the content, methodology and presentation of the mandatory information required by articles 4(1) to (5) of SFDR:

- a reporting template describing how PAIs on sustainability factors are taken into consideration in investment decisions (reporting must be carried out in the format of the template in Annex I of the RTS by 30 June each year with the previous calendar year as a reference period).

- a summary section containing information on policies for the identification of PAIs, actions taken and planned to mitigate them (for instance, reduction of carbon emissions by means of engagement or other policies), and historical comparisons.

- mandatory indicators that will always lead to PAIs and additional opt-in indicators identifying, assessing and prioritising the consideration of additional adverse impacts.

- for financial market participants that do not consider PAIs of investment decisions on sustainability factors, a statement and explanation.

2.2 Pre-contractual product disclosures

The RTSs also detail the content and presentation of the information to be disclosed at pre-contractual level in the sectoral documentation referred to in Article 6(3)12 of the SFDR.

Financial products referred to in Articles 8(1) to (2a) and 9(1) to (4a) of the SFDR, being those which, under Article 8, promote, among other characteristics, environmental or social characteristics (the Light Green Product) and under Article 9 have sustainable investment as an objective (the Dark Green Products), must perform disclosures in that regard, using the format of templates laid down in Annexes II and III of RTS. These templates contain minimum disclosure requirements in relation to:

- how the environmental or social characteristics, or the sustainable investment objectives, (as applicable) are taken into account (including detailed descriptions and alignment with TR);

- if and how PAIs are considered;

- which investment strategy is followed and how assets are allocated;

- information on indexes designated as reference benchmarks (if applicable).

New requirements are developed in relation with the DNSH principle referred to in Article 2, point (17), of the SFDR. with a view of aligning SFDR's DNSH disclosures with TR minimum safeguards13.

2.3 Website disclosures on financial products

Information that is mandatory for product website disclosures include, inter alia, descriptions of environmental or social characteristics or sustainable investment objective (as applicable) or a corresponding negative disclosure, details on investment strategies and asset allocation, monitoring data and measuring methodologies, as well as information on the attainment of the objectives.

2.4 Product-level periodic disclosures

Periodic disclosures in the sectoral documentation referred to in Article 11(2) of SFDR14, must also be carried out in the format of the templates in Annexes IV and V of the RTS.

These templates require filling out elaborate information on, inter alia, how environmental or social characteristics or sustainable investment objectives (as applicable) were attained, historical comparisons covering up to five reference periods, and disclosures of the top 15 investments made during a particular reference period.

3 Mandate to the ESAs to further develop

One month after the RTS' adoption, ESMA published two EU Commission letters inviting ESAs to propose a set of amendments to the RTS, in line with legislative evolutions related to environmentally sustainable activities and the necessity to improve the granularity of existing disclosures.

3.1 Disclosures of product exposures to gas and nuclear activities[15]

In anticipation of the final adoption of the draft Complementary Climate Delegated Regulation16 (see paragraph 7 belowID1 ), the Commission requested for additional disclosures related to fossil gas and nuclear activities to be included in the RTS to ensure that market participants disclose information reflecting the provisions set out in the above Delegated Regulation shortly after the RTS application date.

The ESAs have submitted these draft RTS amendments to the Commission on 30 September 2022 (see paragraph 12 belowID2).

3.2 Amendments on PAI product disclosures and transparency by financial products[17]

Aside the necessity to expand disclosures in relation to the evolutions of the notion of environmentally sustainable activities, the Commission has also requested amendments to the PAI regime[18], with a view of, inter alia, potentially extending the lists of universal PAI indicators and refining all the indicators for adverse impacts and their respective definitions, applicable methodologies, metrics and presentation.

The guiding principle is reducing the risk of "false certainty" and potential "safeguards washing" by requiring well-substantiated evidence that investments align with the safeguards. It also aims at calibrating the RTS so that disclosures are proportionate and feasible for financial market participants.'

As for financial product disclosures, ESAs were requested to enhance transparency on decarbonisation targets – these should cover intermediary targets and, if applicable, actions already pursued.

Finally, a reassessment was requested on whether existing provisions of RTS regarding products referred to in Articles 5 and 6 TR sufficiently address disclosure and information on environmentally sustainable economic activities.

These amendments are expected within a period of 12 months following the receipt of the letter (by May 2023 at the latest).

4 EU Commission Q and A on SFDR and TR

On 25 May 2022, the EU Commission provided additional clarifications on the application of the SFDR and Taxonomy, following a set of queries raised by the ESAs.

Key takeaways from the Commission's Q&A document:

- Product level PAI vs entity level PAI – it is possible to not consider PAIs at entity level (whether voluntarily, or due to being below the 500 employees threshold), yet do so at financial product level

- Pre-existing and closed products – as the SFDR provided no transitional regime, products made available to investors pre- and post-10 March 2021 are in scope of the SFDR. Products that closed before that date do not have to carry out precontractual disclosures, but still have to perform website disclosures. Their periodic reports have to be SFDR-aligned if drawn up after that date. 19

- Good governance – in order to be considered as such, all Article 8 and 9 SFDR products need to ensure their underlying investments are in companies that follow good governance practices20

- Taxonomy disclosures

- Data use – for the purposes of Article 5 and 6 TR disclosures, financial market participants may only disclose information for which they have reliable data on environmental objectives and of the extent of underlying investments which are environmentally sustainable activities, otherwise the TR alignment should indicate zero. If narrative explanations are chosen for the purposes of Articles 5 and 6, these should leave no ambiguity about the alignment, or include negative justifications. For economic activities carried out by undertakings not themselves subject to the TR, in exceptional cases where reliable information cannot be obtained, financial market participants may make complimentary assessments using information from other sources.

- Article 6 TR / Article 8 SFDR - Article 6 TR applies to Article 8 SFDR products that promote environmental characteristics, whether or not they contribute to an environmental objective.

- Article 5 TR / Article 9 SFDR – Article 5 TR applies to Article 9 SFDR products that invest in an economic activity that contributes to an environmental objective. Furthermore, financial products with social objectives that invest in economic activities contributing to an environmental objective will also trigger the application of Article 5.

5 ESMA supervisory briefing on the integration of sustainability risk and disclosures

At the end of May 2022, ESMA published a supervisory briefing21 to ensure convergence of practices of EU national competent authorities in the supervision of investment funds with sustainability features.

This briefing covers the following areas:

(a) Guidance for the supervision of fund documentation and marketing material:

(i) Creation of checklists for pre-contractual documentation assessments to ensure verification of completeness and adherence to minimum disclosure standards;

(ii) Verification of the consistency of information across the fund documentation and marketing material;

(iii) Verification of disclosure clarity and volume, absence of boilerplate language and labelling;

(iv) Principles for fund names (eg use of terms green / impact / sustainable etc);

(v) Clarifications for investment policies, which need to clearly reflect claims made in the fund documentation, as well as key disclosure elements for investment strategies.

(b) Guidance for website and periodic disclosures, respectively – alignment with the SFDR RTS and model disclosures set in its annexes.

(c) Admissibility of additional supervisory actions, which do not rely only on the financial market participants' disclosures, but on findings resulting from portfolio analyses, internal control functions, external auditors, on-site visits etc.

(d) Guidance on the integration of sustainability risks by AIFMs22 and UCITS23 management companies (ManCos) through risk-based, desk-based and on-site surveillance of effective implementation of relevant policies, as well as sample checks.

(e) Examples of breaches for which ESMA considers administrative measures and enforcement to be appropriate.

6 ESAs clarifications on key areas of the draft RTS under SFDR

On 2 June 2022, ESAs undertook to collate various clarifications in relation to draft RTS under SFDR which were submitted to the EU Commission on 2 February24 and 22 October25 2021 respectively. Even though the EU Commission has, at the time of publication, adopted the draft Delegated Regulation on the basis of the two draft RTS, the ESAs have undertaken to share their views on the draft documents, in their versions submitted to the Commission in 2021.

Key clarifications provided by the ESAs relate to the following points:

- Sustainability indicators vs PAI indicators – even though these represent different disclosures under the SFDR, it is possible to use PAI indicators to measure the environmental or social characteristics or the overall sustainable impact of the financial product;

- PAI calculation in periodic disclosures – for periodic

disclosures being governed by sectoral legislation, the methodology

for calculating PAIs of investment decisions on sustainability

factors is set in the provisions of the draft RTS detailing

articles 4 and 7 of the SFDR

- For quantitative changes throughout the reference period, assessments should be based on quarterly average calculations;

- Calculations should cover all instruments, whether direct (securities issued directly by the investee company) or indirect (eg investments in funds and funds of funds), and take into account the results of a look-through approach in relation to underlying investments of holding companies, collective investment undertakings and SPVs.

- Disclosures of investment proportions - where a financial product falls under the scope of article 8 or 9 of SFDR, it should outline the share of investments held directly and indirectly, and the proportion of investments used to attain the environmental and social characteristics or the sustainable investment objective. For the remainder of the assets, disclosures need to be made in relation to the amount, purpose and environmental and social safeguards;

- Changes to be reflected in pre-contractual disclosures – where underlying investments and commitments vary over time, updates should be considered in accordance to the relevant sectoral legislation governing pre-contractual disclosure documents in the context of the life cycle of the product;

- Timing for periodic disclosures – 2022 periodic reports should be drawn up according to the sectoral legislation listed under Article 11(2) in compliance with SFDR, irrespective of reference periods (additional details are to be contained in periodic reports from 1 January 2023, once the RTS start to apply);

- Taxonomy-related product disclosures:

- Taxonomy alignment – for article 3 TR compliant activities only

- Taxonomy-aligned investments are intended to be binding commitments to ensure transparency to end investors (and are subject to penalties for failure to respect);

- Turnover as preferred measurement for the taxonomy contributions of non-financial investee undertakings – if a more representative calculation may be given by capital or operating expenditure, those could be used instead;

- Products should be able to demonstrate contribution to both climate change mitigation and adaptation; and to other four environmental objectives in Article 9 TR once applicable;

- Taxonomy alignment for investments in other products (incl funds of funds) should be based on the aggregate market value of the proportion of taxonomy-aligned underlying investments.

- DNSH:

- Although considerations of PAIs on investments and DNSH disclosures are intended to use the same list of indicators (contained in Annex I RTS), PAI statements under articles 4 and 7 of SFDR should by no means be mistaken with DNSH requirements for sustainable investments and have to be applied independently;

- As ESA's final reports did not specify additional criteria on how PAI indicators should be used for DNSH disclosures, it is proposed as best practice to disclose DNSH for sustainable investments by extracting the indicators from Annex I, and show the impact of sustainable investments against those indicators;

- DNSH under TR and DNSH under SFDR do not apply in the same way - TR sets out detailed DNSH activity level criteria under Article 17 and in technical screening criteria in relevant delegated acts, while SFDR sets out this principle for the purpose of assessing at the level of the investment which may qualify as sustainable. In that respect, it means that to qualify as a sustainable investment in accordance with SFDR, an investment in a taxonomy-aligned economic activity must also respect the 'do no significant harm' principle as set out in Article 2(17) of SFDR;

- The scope of DNSH under SFDR has been enlarged by the RTS in order to include alignment with human and labour rights, thus aligning it to the minimum safeguards under article 18 TR.

7 European Parliament non-objection to the inclusion of gas and nuclear activities in the TR

In July 2022, the European Parliament did not oppose the inclusion of gas and nuclear activities26, under certain conditions, in the classification of transitional activities contributing to climate change mitigation. These are now covered in the Complementary Climate Delegated Act under the TR, published in the EU Official Journal on 15 July 202227 and set to apply from 1 January 2023.

8 Publication of the RTS under SFDR and TR in the EU Official Journal

Following the end of the scrutiny period and the non-objection of the EU Parliament and the Council, the Delegated Regulation of 6 April was published in the EU Official Journal on 25 July 202228. The date of application of technical standards contained therein has been confirmed for 1 January 2023.

9 CSSF Communication to investment fund industry on regulatory requirements in relation to SFDR and RTS

On 27 July 2022, the CSSF published a communiqué to the investment fund industry on regulatory requirements in relation to SFDR and RTS.

The CSSF reminded market participants on several key regulatory deadlines:

- 1 January 2023 – deadline for specific updates of UCITS' and AIFs' (subject to articles 8 and 9 of SFDR) pre-contractual and periodic documents, as well as websites, using the templates provided for in the SFDR RTS

- 31 October 2022 – each UCITS and CSSF authorised AIF are expected to file updated pre-contractual documents in order for the CSSF to endeavour releasing the visa stamp prior to 31 December 2022

- 1 January 2023 – annual reports of UCITS and regulated AIFs issued as of this date must comply with product disclosure requirements laid down in the SDFR RTS and its annexes

The CSSF also highlighted that dedicated precontractual and periodic disclosures should be submitted for each fund compartment.

It is to note that the precontractual and periodic disclosure templates must not be amended except as foreseen under Article 2 of the SFDR RTS, ie the size, font type and colour of characters.

10 ESAs report on the extent of voluntary disclosure of principal adverse impact under the SFDR

At the end of July 2022, the ESAs published the first annual report29 to the European Commission on the extent of voluntary disclosure of PAIs under the SFDR.

This report provides an overview of examples of best practice on disclosures, as well as including a set of recommendations for national competent authorities.

In the report, the ESAs provide a preliminary, indicative and non-exhaustive overview of examples of voluntary disclosures under Article 4(1)(a) of the SFDR. The ESAs conclude that disclosures vary significantly across jurisdictions and categories of financial market participants in scope of SFDR, and it is difficult to identify definite trends.

11 CSSF communication on the SFDR RTS confirmation letter

After announcing its regulatory expectations in July, the CSSF, on 6 September 2022, made available templates for RTS confirmation letters, which are to accompany filings of updated documents. These can be downloaded from the CSSF website, by UCITS ManCos and AIFMs, for UCITS and AIFs respectively.

In order for market participants to benefit from an accelerated document examination in view of visa stamping, the CSSF reminded of several conditions which have to be met:

- Changes to pre-contractual documentation to be limited to Article 8 and 9 of RTS templates, for each fund compartment

- Accompanying confirmation letter and table need to be filled in and signed

- Changes other that those stated in the first point must be minor, of editorial nature and not materially affect investors (otherwise an ordinary amendments' procedure will be carried out)

From a procedural perspective, the following steps will have to be followed

- Submission of draft documentation to the CSSF for examination (if track changes where applicable)

- Implementations of the comments received from the CSSF, until completion

- Upon receiving information that the examination phase has ended and an invitation of the CSSF, electronic transmission of the clean version of the pre-contractual document for visa-stamping

This accelerated procedure will only be available for documentation submitted for examination by 31 October 2022, after which the CSSF will undertake examinations on a best effort basis.

12 ESAs proposal on amending draft SFDR RTS for fossil gas and nuclear energy

Following the EU Commission mandate issued in May and the adoption of the Complementary climate Delegated Act, the ESAs have delivered their suggestions on specific disclosures to be provided in relation to investments in taxonomy-aligned gas and nuclear economic activities.

Going forward, it is proposed for financial product disclosures' templates to contain an additional yes/no question to identify the intent to invest in the above activities and if the answer is yes, a graphical representation of the proportion of investments in such activities.

How can Ogier help?

Ogier offers a powerful platform by pairing legal and regulatory services with technical and practical advice on the implementation and delivery of SI and ESG mandates. We are able to provide tailored legal advice within the context of sustainable investing and we have a team of lawyers across service-lines and jurisdictions who are equipped to advise on related legal and regulatory matters.

Ogier Global's Sustainable Investment Consulting team is experienced in advising on ESG, sustainable investing, impact and climate change including strategy and policy development, ESG risk analysis, metrics identification, reporting in compliance with relevant regulations and industry standards, as well as impact verification.

Should you have any further questions, please contact Ogier in Luxembourg.

Footnotes

1 ESMA 2023 Annual Work Programme, ESMA 22-430-1055

2 Replacing the initial Joint ESA Supervisory Statement on the application of the Sustainable Finance Disclosure of 25 February 2021, JC 2021 05

3 European Commission Letter of 08 July 2021 on information regarding regulatory technical standards under the Sustainable Finance Disclosure Regulation 2019/2088, Ares(2021)4439157

4 Taxonomy-alignment relates to those environmentally sustainable activities which comply with and use the classification laid down by TR

5 Article 27(2)(a) of the TR

6 It is to note that financial products not in scope of articles 8 and 9 of the SFDR, disclosures must cover a negative statement indicating that underlying investments do not take into account the EU criteria for environmentally sustainable activities

7 Joint ESA, Final Report on draft Regulatory Technical Standards with regard to the content of presentation of disclosures pursuant to Article (4), 9(6) and 11(5) of Regulation (EU) 2019/2088 of 22 October 2021, JC 2021 50

8 Delegated Regulation C(2022)1931 final of the European Commission of 6 April 2022 supplementing Regulation (EU) 2019/2088 of the European Parliament and of the Council with regard to regulatory technical standards specifying the details of the content and presentation of the information in relation to the principle of 'do no significant harm', specifying the content, methodologies and presentation of information in relation to sustainability indicators and adverse sustainability impacts, and the content and presentation of the information in relation to the promotion of environmental or social characteristics and sustainable investment objectives in pre-contractual documents, on websites and in periodic reports

9 As per its letter to the Parliament and the Council of 8 July 2021 (Ares(2021)4439157)

10 As per its letter to the Parliament and the Council of 25 November 2021 (Ares(2021)7263490)

11 The so-called "comply or explain mechanism"

12 Article 6(3) of SFDR provides: (a) for AIFMs, in the disclosures to investors referred to in Article 23(1) of Directive 2011/61/EU

(g) for UCITS management companies, in the prospectus referred to in Article 69 of Directive 2009/65/EC

(h)for investment firms which provide portfolio management or provide investment advice, in accordance with Article 24(4) of Directive 2014/65/EU

13 As described in Article 18 of the TR

14 Article 11(2) of SFDR provides: (a) for AIFMs, in the annual report referred to in Article 22 of Directives 2011/61/EU

(g) for UCITS management companies, in the annual report referred to in Article 69 of Directive 2009/65/EC;

(h) for investment firms which provide portfolio management, in a periodic report as referred to in Article 25(6) of Directive 2014/65/EU

15 European Commission Letter of 8 April 2022 on mandate to the ESAs to develop SFDR RTS on product exposures to gas and nuclear activities, Ares(2022)2798608

16 Draft Commission Delegated Regulation amending Delegated Regulation (EU) 2021/2139 as regards economic activities in certain energy sectors and Delegated Regulation (EU) 2021/2178 as regards specific public disclosures for those economic activities

17 European Commission Letter of 11 April 2022 on mandate to the ESAs on PAI product, Ares(2022)2937873

18 Articles 4(6) and 7 SFDR

19 This means that products which are no longer offered to investors but continue to exist, must nevertheless be classified according to SFDR and TR

20 This does not apply to government bonds

21 ESMA, supervisory briefing, Sustainability risks and disclosures in the area of investment management, ESMA34-45-1427

22 Alternative investment fund managers, as defined in Directive 2011/61/EU

23 Undertakings for collective investment in transferrable securities, as defined in Directive 2009/65/EC

24 Final Report on draft Regulatory Technical Standards with regard to the content, methodologies and presentation of disclosures pursuant to Article 2a(3), Article 4(6) and (7), Article 8(3), Article 9(5), Article 10(2) and Article 11(4) of Regulation (EU) 2019/2088

25 Final Report on draft Regulatory Technical Standards with regard to the content and presentation of disclosures pursuant to Article 8(4), 9(6) and 11(5) of Regulation (EU) 2019/2088

26 Under stringent conditions including, inter alia, that both gas and nuclear contribute to the transition to climate neutrality; for nuclear to fulfils nuclear and environmental safety requirements; and for gas to contribute to the transition from coal to renewables

27 Commission Delegated Regulation (EU) 2022/1214 of 9 March 2022 amending Delegated Regulation (EU) 2021/2139 as regards economic activities in certain energy sectors and Delegated Regulation (EU) 2021/2178 as regards specific public disclosures for those economic activities, OJ L 188 of 15 July 2022

28 Commission Delegated Regulation (EU) 2022/1288 of 6 April 2022 supplementing Regulation (EU) 2019/2088 of the European Parliament and of the Council with regard to regulatory technical standards specifying the details of the content and presentation of the information in relation to the principle of 'do no significant harm', specifying the content, methodologies and presentation of information in relation to sustainability indicators and adverse sustainability impacts, and the content and presentation of the information in relation to the promotion of environmental or social characteristics and sustainable investment objectives in pre-contractual documents, on websites and in periodic reports, OJ L 196 of 25 July 2022

29 Joint ESAs' Report on the extent of voluntary disclosure of principal adverse impact under the SFDR of 28 July 2022, JC 2022 35

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.