A reputational risk refers to the threat in terms of profitability or sustainability of a financial institution that is triggered by the public's unfavourable perception of the organization. For instance, if a financial institution has a high-net-worth customer who is a pedophile, the public could cast doubt on the positive image, integrity and goodwill of the financial institution. Another example could be if a financial institution were to engage in activities that could harm the environment, this could change the perception of its clients as well as its employees. In this line, Volkswagen had to spend up to USD 14.7 Billion to settle allegations of cheating emission tests and deceiving customers on 2.0 litres Diesel vehicles with respect to the US Federal Trade Commission. Consequently, this cheating scandal took a significant toll on the reputation of Volkswagen, causing a major drop in its sales as well as causing employees to lose trust over the group.

The consequences of such stigma by the public could be devastating for a financial institution. With the advent of social media, reputational damage can go viral at a click, and the eects can be everlasting. Online discourse can be brutal, with consumers not hesitating to condemn companies. Furthermore, investors can become more skeptical and fearful of facing the public's rage. As for employees, since they are client-facing, they may even find themselves in a state of anguish amidst vehement polemics about their employer. Reputational risk may even lead to increasing criminal or regulatory risks and eventually cause further damage to a financial institution.

At a macro level, the devastating eects faced by a financial institution may bring blame and shame to the reputation of a whole country. This could potentially lead to skepticism as to the eectiveness of the regulator's supervision and could even have an impact on the sound repute of the country, thereby resulting in collateral damage as potential or existing investors may seek to invest their funds in other jurisdictions. If this were to happen to an international financial center, then this could be a major cause of concern with devastating consequences to the economic pillar of a country at large since this would mean substantially less Gross Domestic Product.

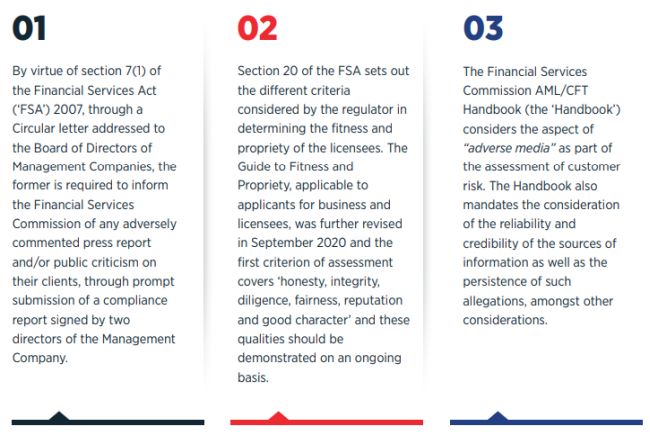

Insofar as operators of the Non-Banking Financial Services sector are concerned in Mauritius, the legal and regulatory framework already takes into account reputational damage through the following:

Given that reputational risk can originate from both internal and external sources for a financial institution, it is noteworthy to point out that like a well-equipped fisherman, the regulatory framework has been designed as a fishing net, with a long and wide outreach, to capture as many negative events and as broadly as possible. Amongst the regulator's equipment, terms like "reputation" and "character" have been used in guidelines signaling that no stone should be left unturned when assessing the fitness and propriety of a person. This depicts the utmost importance that the regulator attributes to preserving the good repute of Mauritius.

In light of the above paragraphs, it has been observed that reputational risk poses massive threats to financial institutions and hence there is a need to strike the right balance between managing "worth it" and 'worthy' client relationships. As rightly stated by Abraham Lincoln, "Character is like a tree and reputation like its shadow. The shadow is what we think of it; the tree is the real thing." Assessing reputational risk therefore signifies going beyond an assessment of money laundering and terrorist financing ("ML/TF") risks. Therefore, non-ML/TF elements should also form part of assessment of adverse information. Through the current legal and regulatory framework in place, it appears to be no easy task to evade the regulator's fishing net. Thus, reputational risk must be a substantive component that should be considered by all financial institutions since this could have terrible consequences in terms of the public's perception of the financial institution and the country of operation, thereby aecting the sustainability and profitability of the financial institution as well as the good repute of the country. The need for continuous vigilance through an eective KYC program is therefore of prime importance as well as staying compliant with reporting obligations vis-à-vis the regulator.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.